Digital Neuritis Drug Market Overview: Key Drivers and Challenges

Other |

2026-04-07 04:21:45

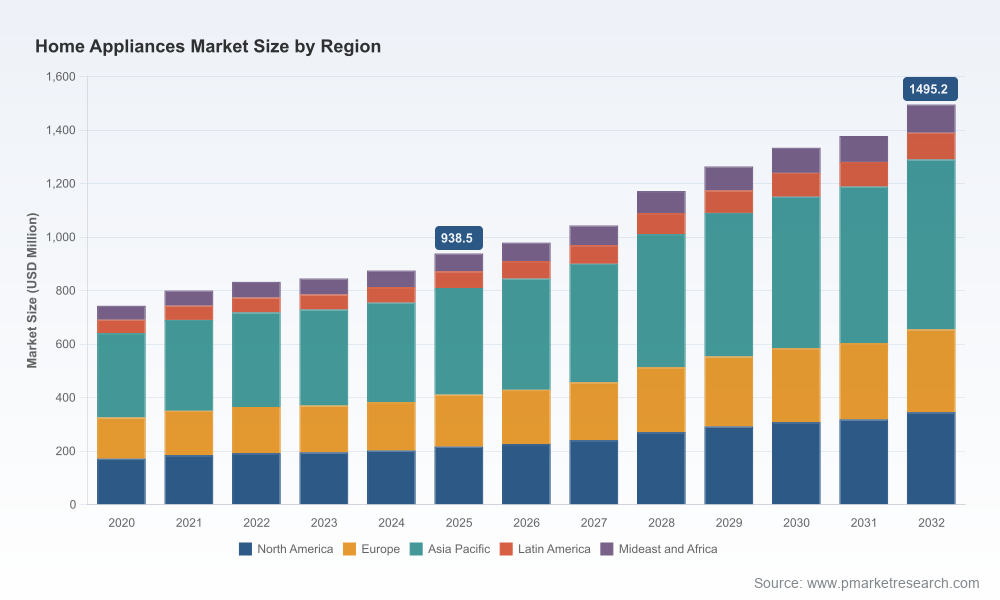

As companies plan bold strategic moves in 2026, clarity on market scale, growth trajectory and the dynamics reshaping competitive advantage is non‑negotiable. Our Home Appliances Market study (base year 2025; historical 2020–2025; forecast 2026–2032) shows a market that has grown from a measured baseline in 2020 to an expanded industry footprint by 2025 and is projected to continue expanding through 2032. At the headline level, the market was approximately 743.2 Million USD in 2020 and reached 938.5 Million USD in 2025. Early forecast indicators show an estimated 979.2 Million USD in 2026 and directional growth to roughly 1,495.2 Million USD by 2032—reflecting a compound annual growth rate (CAGR) of 6.98% across the forecast period.

Home Appliances Market

These topline metrics tell two concurrent stories: robust consumer and commercial demand for appliance replacement and upgrade cycles, and a market undergoing structural change driven by smart connectivity, supply‑chain realignment, and regulatory pressure. For senior leaders, the question is not whether the market will grow, but how to capture disproportionately large value as growth accelerates and disruption intensifies.

Home Appliances Market

Our report is designed as a decision‑quality toolkit for executive teams and corporate development functions. It combines rigorous market sizing and forecasting with executable strategy products—built to be used, not admired. Core deliverables include:

Home Appliances Market

The report purposefully combines quantitative rigor with practical templates: negotiation one‑pagers, Sprint‑style implementation checklists, and board‑ready slide decks—so teams can move from insight to execution in weeks, not months.

The industry remains concentrated—top three players account for a substantial share and the top five capture an even larger portion of market value—creating a landscape where scale, brand equity and channel access matter. That concentration underpins both defensive and offensive strategic choices for incumbents and new entrants alike.

Key incumbents we profile in depth include global OEMs with differentiated strategic postures:

Recent competitive moves illustrate the strategic playbook in action: BSH’s early‑2026 launches that integrate AI‑driven cooking guidance point to premium feature monetization; Electrolux’s partnership with Midea signals selective teaming to accelerate North American scale; GE Appliances’ multi‑billion investment program underscores a renewed emphasis on domestic capacity and product innovation. Each example reinforces the need for firms to match product strategy with sourcing and channel tactics.

Regulatory developments are a central stressor for 2026 strategy. Expanded Section 232 inclusions and strengthened tariffs introduced in 2025–2026 create an elevated landed‑cost baseline for appliances with significant steel and aluminum content and certain derivative articles. USITC analyses indicate these measures can compress import volumes, raise domestic input costs, and feed through to consumer prices over multiple quarters. Concurrently, product safety actions—recent CPSC recalls for heaters and small electrics—amplify reputational, warranty and compliance costs.

Our report supplies tactical responses that leaders can operationalize immediately: local content roadmaps to mitigate duties, tiered sourcing strategies that balance cost and risk, contingency manufacturing plans for critical SKUs, and tightened QA protocols to reduce recall probability and repair cycle costs.

We designed this study to be immediately applied by strategy, commercial and operations teams. Engagements typically begin with a two‑week strategy sprint to calibrate the firm’s exposure across product families and markets, followed by a 12‑week implementation program that includes:

Our approach is explicitly pragmatic: we combine the top‑down market forecast (presented in this primer) with bottom‑up SKU economics and validated supplier cost models so leaders can make capital allocation, pricing, and commercial decisions with confidence.

In this executive primer we intentionally surface strategic trends, competitive implications and operational playbooks while withholding certain granular segmentation tables and proprietary datasets that form the basis of executable targets (including detailed regional, application and product‑type splits). That level of granularity—along with downloadable datasets, interactive models and the full competitor scorecards—is available in the full report and on our client portal. This “preview” strategy lets us demonstrate analytical depth and practical orientation while protecting the proprietary inputs that enable precise, actionable decisions.

If your agenda for 2026 includes pricing resets, supply‑chain reconfiguration, smart‑appliance monetization, or M&A, PW Consulting’s Home Appliances Market report is designed to be the strategic reference point—and the operational engine—for your initiatives. Contact our industry team to schedule a briefing and obtain access to the full dataset and implementation toolkits that will enable accelerated decision‑making in the year ahead.

For detailed analysis of this topic, please visit the official page:Home Appliances Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com