What Are the Latest Trends Driving Growth in Tablets Market Worldwide?

Networking |

2026-05-19 13:26:24

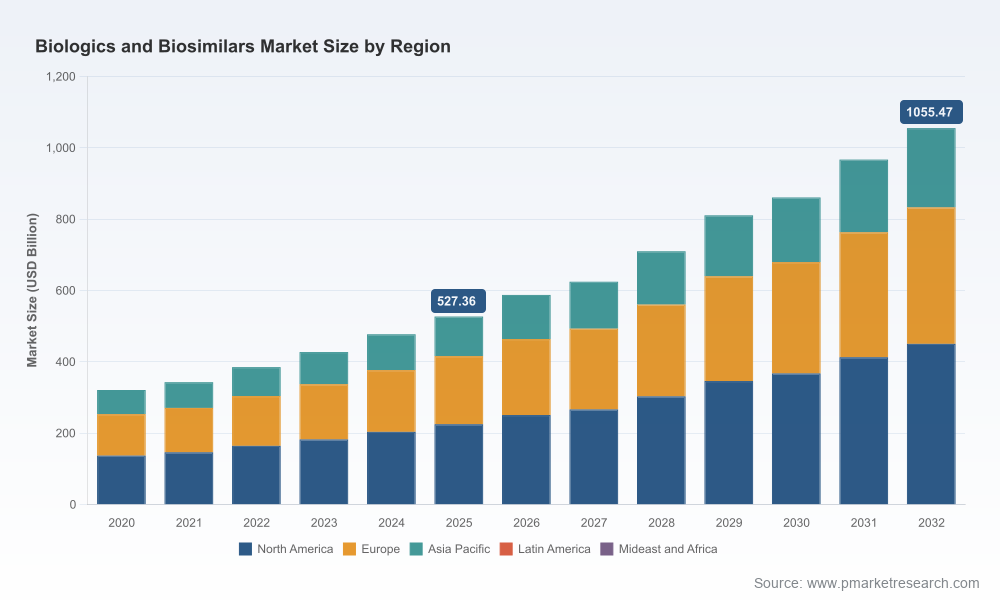

As drug developers, manufacturers and payors plan for the next horizon, the biologics and biosimilars market is entering a decisive growth phase. Using 2025 as our base year, the market eclipses half a trillion USD and is projected to expand at a compounded annual growth rate (CAGR) of approximately 10.42% over the 2026–2032 forecast window. By the end of that period the market more than doubles versus the 2025 baseline, reflecting accelerating adoption, an expanding therapeutic addressable base and intensified commercial competition. Market concentration remains meaningful but not insurmountable — three firms control a modest share of the total, and the top five account for less than half of market value, signaling room for challenger strategies and scale plays.

Biologics and Biosimilars Market

Investment prioritization: With rapid top-line expansion and therapeutic innovation, capital allocation across R&D, capacity expansion and business development must be prioritized against a backdrop of price pressure and reimbursement uncertainty. Our study translates top-line growth into the tactical decisions finance and strategy teams need to make in 2026.

Biologics and Biosimilars Market

Go-to-market timing: Several regulatory and commercial inflection points in 2024–2026 make launch sequencing and commercialization partnerships central to success. We map the windows where first-mover advantage, interchangeability designations and payer contracting materially change commercial trajectories.

Biologics and Biosimilars Market

Manufacturing and supply resilience: The market’s growth is only as real as the supply chain that supports it. Our analysis identifies chokepoints in sterile injectable and API sourcing, quantifies tariff and input-cost pressures, and shows the operational contingencies that preserve margin in 2026.

M&A and partnership targeting: Fragmented concentration combined with accelerating biosimilar launches creates attractive arbitrage for acquisitions, licensing and JV structures. The report provides an evidence-based framework to screen targets and model post-deal synergies under varied reimbursement scenarios.

PW Consulting’s Biologics and Biosimilars Market study is purpose-built for executives who need immediately actionable intelligence. The core deliverables include:

The market is shaped by a mix of incumbent biologics leaders and fast-moving pure-play biosimilars specialists. The competitive environment combines deep scientific capabilities, scaled manufacturing footprints and varying commercial models — direct-to-market, partner-led commercialization and region-specific licensing. Below we summarize the strategic posture of the primary players covered in the study.

Amgen Inc. (Thousand Oaks, CA) — A legacy biologics leader with a broad biosimilars rollout history. Amgen’s portfolio strategy emphasizes generating commercial scale quickly through approved, high-profile biosimilars and leveraging existing commercial infrastructure to defend and extend margin in key markets.

Pfizer Inc. (New York, NY) — Combines substantial manufacturing capability with aggressive commercialization in oncology and specialty categories. Pfizer’s playbook centers on operational scale, strategic partnerships and leveraging global supply chains to drive market share.

Sandoz Group AG (Basel, Switzerland) — A pure-play follow-on biologics specialist that prioritizes regulatory efficiency and cost-competitive manufacturing. Sandoz focuses on rapid approvals and price-sensitive market penetration strategies.

Celltrion Inc. (Incheon, South Korea) — Growth-oriented biosimilars manufacturer with an aggressive product roadmap and expanding US capacity. Celltrion’s model pairs volume-driven manufacturing with an aggressive global launch cadence.

Biocon Biologics Ltd. (Bengaluru, India) — Focuses on cost-competitive biosimilars and partnerships that open Western markets. Biocon’s ability to combine lower-cost manufacturing with regulatory approvals has made it a strategic partner for multinational commercialization.

Alvotech (Reykjavík, Iceland) — A nimble innovator targeting high-value reference biologics through focused biosimilar development and select regulatory submissions, with a playbook that emphasizes targeted launches in specialty categories.

Formycon AG (Munich, Germany) — A specialist in ophthalmology biosimilars, Formycon leverages niche therapeutic focus to win formulary spots and to negotiate favorable hospital and specialty-clinic access.

Samsung Bioepis (Incheon, South Korea) — Strength lies in combining biotech R&D with large-scale manufacturing and US commercialization partnerships; their strategy emphasizes co-development and co-commercialization in major markets.

Fresenius Kabi AG (Bad Homburg, Germany) — Uses an existing hospital and infusion-product footprint to support biosimilar adoption in institutional settings and to bundle supply offerings for hospital systems.

2024–2025 saw a cluster of regulatory approvals and guidance updates that materially affect growth trajectories and go-to-market tactics. Highlights include FDA activity that makes interchangeability easier to achieve, several new approvals across monoclonal antibody biosimilars and oncology agents, and confirmation that the universe of approved biosimilars is growing faster than realized market share.

Three structural dynamics frame risk and opportunity for 2026:

Adoption gap: Although regulatorily approved biosimilars are multiplying, their realized market share lags approval counts. Structural headwinds in contracting, physician switching behavior and payer carve-outs temper volume ramp assumptions.

Reimbursement pressure: Public and private payors are recalibrating reimbursement for biologics. In the U.S., persistent underpayments to hospitals and lagging Medicare adjustments change the economics of hospital-administered biologics versus outpatient or retail channels.

Supply-chain concentration: A sizeable share of APIs and sterile injectable capacity remains concentrated in a small set of geographies. Tariff changes and input-cost volatility have increased the marginal cost of production for monoclonal antibody batches, making supply strategy a board-level risk.

Reassess portfolio prioritization through an adoption-sensitivity lens: prioritize programs with the shortest path to interchangeability or with durable hospital economics.

Secure supply redundancy: immediate actions should focus on dual-sourcing APIs and qualifying sterile-injectable partners outside concentrated geographies to mitigate tariff and capacity shocks.

Align commercialization with payor contracting: develop specialty-channel and hospital-bundle offers that reflect real-world reimbursement constraints and unlock institutional uptake.

Identify M&A and partnership targets where manufacturing scale or regulatory dossiers accelerate market entry — and use our deal-screening models to validate valuation under conservative uptake scenarios.

Invest in evidence generation: payer-facing health economics and outcomes research (HEOR) will be decisive to convert approvals into formulary wins and to compress time-to-volume.

This briefing demonstrates the depth of analysis Pw Consulting applies to biologics and biosimilars strategy while intentionally withholding the granular regional, type and application line-item numbers that drive tactical decisions. The full report contains the complete subsegment breakdowns, downloadable financial models, interactive scenario dashboards and the competitor playbooks referenced above.

If your 2026 planning cycle requires prioritized investment lists, M&A screening, manufacturing capacity blueprints or payer negotiation simulations, the full study and accompanying advisory workshop will translate these insights into a 90‑day execution plan tailored to your organization’s strategic objectives.

For detailed analysis of this topic, please visit the official page:Biologics and Biosimilars Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com