Battery Separator Films Market — Strategic Outlook for 2026 Decision-Making

Executive snapshot

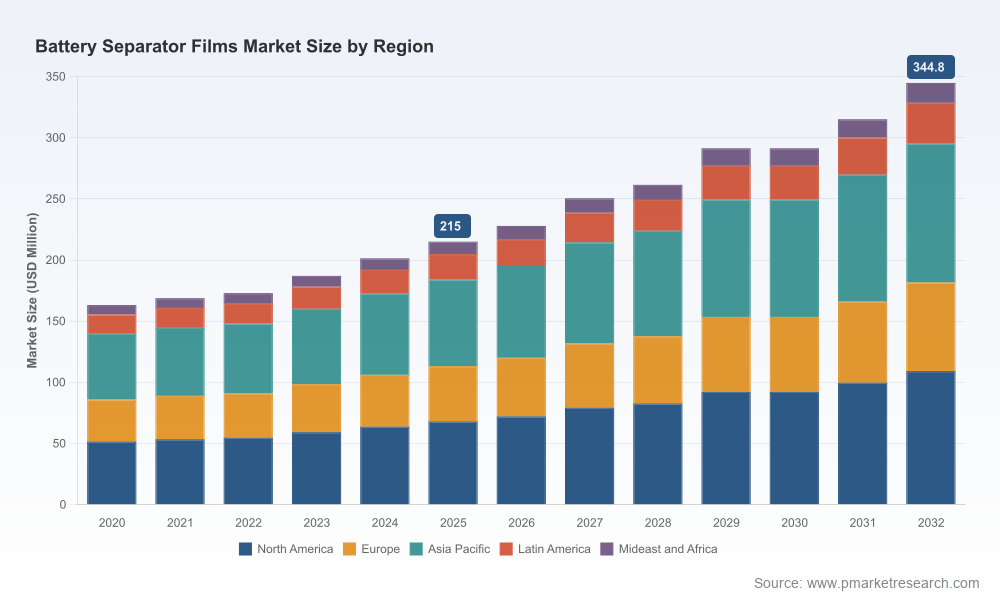

As global electrification accelerates, battery separator films have moved from a component-level consideration to a strategic lever for original equipment manufacturers, cell makers and materials suppliers. Our PW Consulting Battery Separator Films Market study (base year 2025) synthesizes five years of historical behavior and a seven‑year forecast horizon (2026–2032) to translate market signals into operational decisions for 2026. The market grew from roughly USD 163.2 Million in 2020 to USD 215.0 Million in 2025 and is forecast to reach USD 344.8 Million by 2032, representing a compounded annual growth rate of 6.98% over the forecast window. These headline metrics frame a mid‑single‑digit growth market that is large enough to attract strategic capital yet fragmented enough to reward targeted capability plays.

Battery Separator Films Market

Why this research matters for 2026

- Timing: 2026 is a pivot year for downstream demand and domestic manufacturing incentives. Companies making supplier, capacity or vertical integration choices this year will lock in cost and security advantages for the coming decade.

- Risk concentration: The market exhibits relatively low concentration — the largest players do not yet dominate the majority of demand — which creates opportunity for new entrants, regional champions and targeted M&A.

- Policy inflection: Public programs and loan facilities designed to reshore critical battery components have shifted project economics; capturing those benefits requires a clear view of project sequencing and eligibility criteria.

Market trajectory — what the numbers tell us (high level)

The market’s rise from about USD 163 Million in 2020 to USD 215 Million in 2025 demonstrates recovery and structural growth through the EV and energy storage build‑outs. The forecast to USD 344.8 Million by 2032, at a 6.98% CAGR, implies continued expansion driven by mainstreaming of EVs, stationary storage deployments, and incremental technical requirements (safety, thinness, coating technology). For corporate strategists, the takeaway is clear: separator films are not a commoditized sideline — they are a growing materials market with meaningful implications for supply chain resilience, cost-to-performance tradeoffs, and product differentiation.

Battery Separator Films Market

Key market dynamics shaping 2026 choices

- Demand drivers: Continued EV penetration and large‑scale energy storage projects remain the principal demand engines. Cell format diversification (pouch, prismatic, cylindrical) and evolving chemistry mixes require varying separator attributes — thickness, porosity, coatings — leading to product segmentation and new qualification cycles.

- Capacity and policy: North American and regional capacity additions accelerated in 2025–2026, supported by targeted public financing. Notably, a major U.S. Department of Energy support package materially de‑risked a new domestic production facility, demonstrating how public loans can alter location economics and content strategies.

- Raw material volatility: Polyolefin feedstocks faced price dispersion and supply constraints in 2025, increasing manufacturing cost variability. Buyers and producers must embed feedstock sensitivity scenarios into procurement and contract design.

- Technology evolution: Wet‑process polyethylene and dry‑process polypropylene remain core platforms, while ceramic and coated solutions are evolving for enhanced safety. Suppliers are investing in ultra‑thin coatings and ceramic architectures that trade incremental cost for safety and energy density benefits.

- Fragmentation and specialization: The market structure still rewards specialist players who combine process expertise with close OEM qualification support. Market concentration is modest — the top firms collectively account for roughly one quarter of global value — which keeps competitive entry and regional champion strategies viable.

Competitive landscape — what incumbents and challengers are doing

The report profiles leading technology and manufacturing players and evaluates strategic positioning across technology, capacity footprint, customer access and certification speed. Representative firms include major integrated Japanese and Korean chemical manufacturers, specialized polymer film houses, and Western producers scaling domestic capacity. Several trends are visible in company moves:

Battery Separator Films Market

- Strategic partnerships and regional supply agreements to secure OEM relationships and shorten qualification timelines.

- Capacity expansions and greenfield lines in target geographies that benefit from local content incentives.

- R&D and process upgrades aimed at ultra‑thin, coated and ceramic architectures to meet higher safety specifications for next‑generation cells.

Key corporate profiles covered in the study (illustrative) span long‑standing wet‑process polyethylene producers, dry‑process polypropylene incumbents, and fast‑growing regional manufacturers. For each company we map product portfolios, production technologies, recent capacity moves, and typical OEM engagement models to highlight where a counterparty fits on the risk/reward spectrum for suppliers and buyers.

Recent industry developments (select highlights)

- Production consolidations and restructuring by established chemical groups to rationalize output and improve per‑line productivity.

- Strategic supply agreements linking separator producers to major automotive supply networks, aiming to secure long‑term offtake.

- Capacity expansions in North America and Asia, including new production lines for ultra‑thin coated separators and the commissioning of expanded facilities to serve regional EV ecosystems.

- Public funding and loan support that shifted project economics for domestic producers, enabling faster ramp and improved financing terms.

Each of these developments is analyzed in the report with implications for cost curves, qualification timelines and supplier selection strategies.

What the PW Consulting report delivers (practical, action‑oriented contents)

This study is designed to be decision‑ready for commercial, supply chain and corporate development teams. Key deliverables include:

- Market model and scenario set: A transparent baseline model (2020–2025 historical) with three forward scenarios to 2032, capturing demand sensitivity to EV adoption, stationary storage build‑outs and raw material shocks.

- Supplier scorecards: Comparative matrices of technology competence, qualifying timelines, geographic footprint, and risk exposures for the major producers and promising challengers.

- CapEx and time‑to‑market playbooks: Practical guides for sizing greenfield vs. brownfield investments, minimum viable capacity steps, and typical ramp assumptions by process type.

- Procurement and contracting templates: Negotiation levers for fixed vs. variable pricing, indexation approaches for feedstock volatility, and qualification milestone structures to manage supplier onboarding risk.

- Regulatory and incentive matrix: A compiled dossier of key public programs, loan facilities and content rules that materially affect location economics and eligibility for subsidies.

- Technology roadmaps and failure modes: Engineering‑grade descriptions of separator performance attributes tied to cell safety and energy density, and a prioritization of R&D bets by ROI horizon.

How to use this research in 2026 — recommended decision frameworks

Companies should translate the study’s insights into an integrated set of actions across four dimensions:

- Supply security: Map current and prospective suppliers against demand profiles and qualification lead times. Prioritize dual‑sourcing and nearshoring where policy incentives and logistics justify incremental cost.

- Cost management: Build material‑price sensitivity into commercial contracts and internal cost models. Consider hedging strategies or captive feedstock arrangements for large volume commitments.

- Product differentiation: For OEMs and cell makers, define separator requirements as part of cell‑level performance tradeoffs; specify where premium coatings or ceramic features justify higher cell cost through safety or energy benefits.

- Strategic investment and partnerships: Evaluate capacity expansions, minority stakes and joint ventures with suppliers based on modeled payback under different market scenarios. Public financing windows can materially lower hurdle rates for onshore projects if structured correctly.

Where this report withholds and why — the trailer approach

To serve executives who need both actionable direction and motivation to engage the full intelligence product, this overview demonstrates the analytical scaffolding and strategic conclusions without reproducing the granular segmentation tables, regional/application dollar splits or proprietary supplier scoring matrices. Those detailed segmentations, unit‑level pricing curves, and confidential technical scoring frameworks are available in the full report and are the precise building blocks recommended for supplier selection, contract negotiation, and capital allocation in 2026.

Conclusion — a decision lens for 2026

The battery separator films market presents a clear growth runway with nuanced risk layers that make 2026 a consequential year for capital, procurement and partnership decisions. With a base year of 2025 and a forecast to 2032 at a 6.98% CAGR, stakeholders who align supplier strategy, raw material risk management and technology choices now will secure outsized competitive advantage. PW Consulting’s full Battery Separator Films Market study supplies the granular data, supplier scorecards and playbooks that convert market forecasts into executable, low‑regret moves. For teams planning capacity, sourcing or M&A steps this year, the study is engineered to reduce uncertainty and accelerate decision cycles.

Next steps

- Access the full report to review the regional and application breakdowns, unit‑level cost curves, and supplier scorecards required to finalize 2026 plans.

- Engage PW Consulting for a tailored workshop to map your company’s exposure and prioritize actions across sourcing, capex and technology investments.

For detailed analysis of this topic, please visit the official page:Battery Separator Films Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com