Global Bunker Fuel Oil Market Set to Hit USD 225.4 Billion by 2034 at 4.1% CAGR

Technology |

2026-06-09 08:55:54

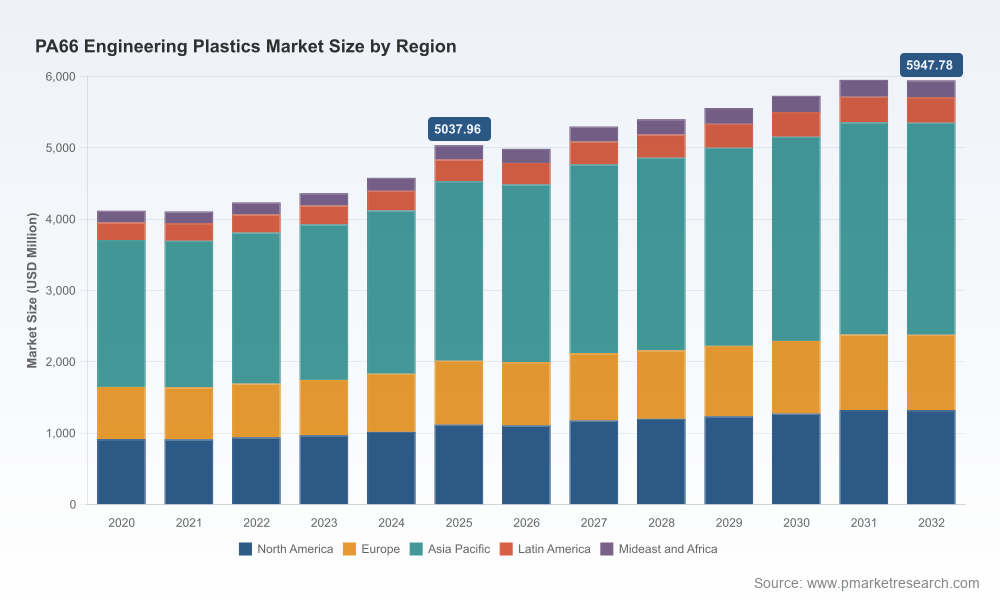

As 2026 begins, the global PA66 engineering plastics market sits at a pivotal inflection—anchored by structural applications in transportation and electrical systems, while being reshaped by raw-material volatility, sustainability imperatives, and selective innovation among a handful of large producers. Our study uses 2025 as its base year, traces 2020–2025 historical performance, and projects forward through a 2026–2032 forecast window. On a headline basis, the market expanded materially from the low‑4000s (USD Million) in 2020 to roughly 5.04 billion USD (USD Million) in 2025, and — under our central scenario — grows at a compound annual growth rate of about 2.4% over the forecast horizon. The model does show near-term normalization in 2026 before a sustained recovery, underscoring how short-cycle shocks can ripple through the value chain despite a structurally supported long‑term demand base.

PA66 Engineering Plastics Market

Investment prioritization: Capital allocation decisions—whether for capacity expansions, debottlenecking, or M&A—must be informed by an understanding of medium-term demand elasticity, price corridors, and competitor concentration. Our study provides scenario-tested volume and revenue pathways (base case, downside, upside) that translate macro growth assumptions into portfolio impact for manufacturers and compounders.

PA66 Engineering Plastics Market

Supply‑chain resilience: PA66's upstream linkage to adipic acid and hexamethylene diamine exposes producers to feedstock and logistic shocks. The report quantifies the sensitivity of producer margins to feedstock cost moves and offers mitigation playbooks (index-linked contracts, hedging, and feedstock diversification) calibrated for 2026 conditions.

PA66 Engineering Plastics Market

Product & portfolio strategy: For OEMs and compounders targeting electrification and high-temperature applications, our analysis ranks PA66 product subfamilies by technical fit, cost-to-performance, and adoption risk—allowing R&D and commercial teams to sequence product launches and pricing strategies.

Sustainability transition: With a rising share of buyers demanding lower‑carbon content and closed‑loop solutions, the research highlights practical levers—bio‑circular feedstocks, chemical recycling, ISCC‑type certifications—and maps their cost, timeline, and reputational tradeoffs for 2026 decision-making.

Methodology & data appendix: Transparent market sizing approach, source weighting, and our reconciliation of company disclosures, trade flows, and primary interviews (base year 2025; historical 2020–2025; forecast 2026–2032).

Top‑line market model: Annual revenue and volume time series (historical and forecast) with scenario toggles and sensitivity tables. Headline market size and growth trajectories are stated in USD (revenue unit: Million).

Supply & demand balance: Capacity maps, utilization estimates, and near‑term reconfiguration risk points (including expected post‑2025 commissioning schedules and likely uptime scenarios).

Price and margin bridge: Cost curve for typical PA66 manufacturing, feedstock pass‑through mechanics, and modeled margin impact under plausible raw‑material moves.

Segment analysis: Demand drivers and commercial dynamics by product grade and end‑use (we deliberately withhold full granular tables in this preview to retain strategic exclusivity; complete split tables are available in the full report).

Regulatory & sustainability matrix: Policy tailwinds and barriers (including certification regimes and recycling standards) with timeline estimates and supplier readiness scoring.

Competitive profiles and benchmarking: Deep‑dive dossiers on the leading global producers, their asset footprints, go‑to‑market positioning, technology differentiators, and strategic intent.

Opportunity map: Near-term commercial plays (premiumization, product bundling, regionalized logistics), M&A screening, and private‑equity return scenarios calibrated to 2026 market dynamics.

Playbooks & annexes: Negotiation levers for feedstock contracts, sample contractual language for bio‑content claims, and a practical checklist for launching recycled or bio‑based PA66 grades.

The PA66 market is meaningfully concentrated: the leading three global groups collectively control a material share of global shipments, with the top five firms commanding an even larger portion of the market. This concentration creates both stability in price leadership and risks of capacity-driven pricing moves. Our competitive audit shows a two‑tier structure: fully integrated producers with upstream monomer control and compounders/compound integrators that add value through formulation and application development.

Ascend Performance Materials (Houston, Texas) — the largest fully integrated PA66 producer globally. Ascend’s strategic pivot toward bio‑circular feedstocks is a potential industry inflection: by end‑2025 it reported production runs using used‑cooking‑oil based feedstocks with a reported ~25% carbon footprint reduction. For buyers and investors, Ascend’s move accelerates the commercialization baseline for bio‑content claims.

Invista (Wilmington, Delaware) — a longstanding leader in PA66 polymers and intermediates with deep OEM relationships. Its breadth across resin and polymer intermediates gives it flexibility in responding to feedstock swings and application-specific formulations.

RadiciGroup (Novara, Italy) and EMS‑GRIVORY (Domat/Ems, Switzerland) — specialist producers with strong compound portfolios and engineering partnerships in Europe; they compete on tailored formulations and high‑performance end‑use certifications.

Lanxess (Cologne, Germany) and BASF (Ludwigshafen, Germany) — both are active in high‑performance PA66 and related polyamide spaces. Recent product launches (e.g., additive packages to enhance thermal/mechanical properties; new polyphthalamide grades aimed at EV thermal envelopes) show a clear focus on electrification and thermal resilience.

Celanese (Irving, Texas) and Envalior (Netherlands) — represent a mix of global scale and focused high‑performance offerings, with Celanese leveraging compounder scale and Envalior targeting premium structural and thermal niches.

Recent industry moves underscore two parallel trends. First, sustainability-led productization and feedstock substitution (Ascend’s bio‑circular runs and ISCC Plus certification) are shifting supplier economics and customer expectations. Second, circularity technologies such as Toray’s chemical recycling process (announced in early 2025) are moving from lab‑scale demonstration toward commercial feasibility, creating an emerging recycling supply chain that could materially alter input cost profiles over the medium term.

Raw-material dependence: PA66’s upstream reliance on adipic acid and hexamethylene diamine concentrates exposure. Procurement teams must plan for episodic shortfalls and price shocks; our stress tests quantify margin erosion under 10–30% feedstock cost swings.

Price volatility: Regional price movements remain asymmetric—our analysis documents recent declines in Asian transactional prices during 2025, and suppliers in 2026 have continued to use price updates to manage margin pressure. Sellers in North America have taken corrective action as well (for example, there were producer price adjustments on upstream inputs in 2026), which will influence regional competitiveness.

Regulatory & compliance noise: Chemical and polymer pricing adjustments by large producers for caprolactam and related inputs can create cross‑polymer competitiveness shifts—an important consideration for firms that compete across PA6/PA66 portfolios.

Technology transition: Adoption timing for bio‑based feedstocks and chemical recycling will determine who captures early‑mover premium vs. who faces stranded investments.

For producers: prioritize selective capacity upgrades and invest in feedstock flexibility. Structure new offtake contracts with indexation and sustainability tranches to de‑risk project economics.

For compounders: double down on application engineering for EV thermal systems and electrical insulation where PA66’s properties are differentiators; create bundled solutions (material + design support) to defend margin.

For OEMs: build dual‑sourcing playbooks that account for both technical equivalence and verified sustainability credentials; run procurement pilots for recycled/bio‑content grades before scaling.

For investors: screen for firms with integration into monomer supply or with credible circularity roadmaps; use scenario returns (base, downside, green premium) included in the report to set bid/ask ranges.

This preview outlines the strategic DNA of the PA66 market and the practical choices companies face in 2026. The full PA66 Engineering Plastics Market report from PW Consulting contains the complete, source‑level datasets: the year‑by‑year revenue and volume matrices, the detailed segment and regional splits, company-level capacity vintages, pricing ladders, and the scenario models with downloadable worksheets. Those who need to convert insight into investment or commercial action will find the granular tables, model inputs, and executable playbooks essential.

Accessing the full report will provide the specific segmentation, transaction tables, and interactive models necessary to quantify the precise P&L and balance-sheet impacts for targeted strategies in 2026. For firms that must make capital, procurement, or product portfolio decisions this year, that level of detail is the difference between informed agility and reactive oversight.

For detailed analysis of this topic, please visit the official page:PA66 Engineering Plastics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com