Birthmark Removal in Islamabad: What Makes Modern Procedures More Effective?

Health |

2026-07-02 12:17:27

As firms prepare investment and product roadmaps for 2026, the engine-driven welders market presents a classic industrial-opportunity set: mature core demand, steady growth, concentrated supplier power, and pockets of premiumization driven by jobsite productivity and emissions/engine compliance. PW Consulting’s latest market modeling uses a 2025 base-year and projects the market forward at a 4.91% CAGR — moving from roughly USD 1.38 billion in 2025 toward an approaching USD 1.91 billion by 2032. This primer synthesizes why that trajectory matters for executive decisions, what commercial moves separate winners from also-rans, and which parts of the intelligence we keep proprietary to encourage direct access to the full report.

Engine-Driven Welders Market

Reliable growth envelope: A mid-single-digit CAGR anchored to resilient end-markets (construction, energy/infrastructure maintenance, mining and pipeline work) creates a low-volatility setting for both organic investment and targeted M&A. That predictability supports multi-year product development cycles and platform investments.

Engine-Driven Welders Market

High concentration, high leverage: Market concentration data show a clear advantage to market incumbents — leading manufacturers capture the lion’s share of value — creating scale-driven R&D, distribution, and aftersales advantages that are difficult for new entrants to replicate overnight.

Engine-Driven Welders Market

Product-as-service and jobsite productivity premiumization: Buyers are increasingly willing to pay for features that reduce labor and downtime (integrated generator-welder combinations, improved duty cycles, compact footprints for service trucks). This shifts margins away from pure hardware toward bundled service propositions and aftermarket consumables.

Regulatory and engine compliance pressures: Engine emissions compliance and customer demand for lower operating costs make engine choice and supplier partnerships (e.g., Kohler, Kubota, other OEMs) strategically material for new product programs.

Demand drivers: The market’s baseline growth is driven by steady spending on construction and infrastructure maintenance, periodic mining and pipeline projects, and a continued need for portable welding power where grid or stationary power is impractical. These dynamics favor portable, high-duty-cycle systems that offer dual-functionality (welding + auxiliary power).

Product evolution: Recent product launches demonstrate two concurrent trends — premium high-output units built for continuous heavy-duty use and compact, fuel-efficient models tailored for service vehicles and constrained jobsite footprints. Both directions are visible in new product introductions that emphasize duty cycle, generator capacity, and engine robustness.

Cost structure sensitivity: Raw materials for alternators, control electronics, and engine subsystems introduce volatility; fuel and maintenance economics influence total cost of ownership and therefore purchasing preferences among contractors and rental houses.

Channel and aftermarket importance: Dealers, rental fleets, and service networks are the primary gates to end-users. Aftersales support, spare-part availability, and service SLA performance materially affect lifetime value and brand differentiation.

The competitive field blends global industrial champions with regional specialists. The following high-level strategic profiles capture the posture of market leaders and notable challengers (full company dossiers and benchmarking matrices are available in the full report):

The Lincoln Electric Company — Leverages deep welding technology, established global channels, and strong OEM engine partnerships. Recent launches focus on premium arc performance and robustness for harsh jobsite conditions, reinforcing Lincoln’s positioning in heavy construction and industrial segments.

Miller Electric — Emphasizes product breadth across portable and truck-mounted systems with attention to regulatory compliance and integrated systems. Miller’s product portfolio and brand trust make it a first-choice partner for rental companies and contractors that prioritize reliability and compliance.

ESAB Corporation — Continues to target challenging environments with compact, high-duty-cycle units that combine welding output and significant generator power. ESAB’s recent high-output product introductions point to a strategy of premium-positioned, jobsite-optimized equipment.

Mid-size and specialist players — Suppliers including Hobart, Multiquip, Denyo, MOSA, Shindaiwa, Tomahawk, Cruxweld, and regional manufacturers are playing differentiated roles: some focus on fuel efficiency and compactness, others on rugged field use, and a few on price-competitive offerings for growing regional demand. Their collective presence increases options for OEM partnerships and private-label programs.

Two recent product milestones illustrate competitive dynamics: ESAB’s launch of a fully assembled high-duty 270A engine-driven welder/generator designed for harsh environments (Sept 2025), and Lincoln’s Frontier 500X (Feb 2026) emphasizing advanced arc control and rugged performance. These introductions underline an arms race in performance-per-pound and generator integration — critical attributes that customers reward in field use.

For executives setting 2026 priorities, our analysis yields a focused set of strategic levers that create disproportionate value:

Prioritize integrated platform development — Develop systems that tightly integrate welding controls and auxiliary power electronics to create measurable productivity gains on site. Aim for features that demonstrably reduce labor hours and generator footprint; these are the levers buyers will pay for.

Lock in engine and emissions partnerships — Early agreements with reputable engine OEMs and compliance roadmaps reduce time-to-market risk and protect against regulatory retrofits. Consider co-engineering to optimize packaging, cooling, and maintenance intervals.

Invest selectively in rental and dealer ecosystems — Rental fleets are high-frequency users that accelerate product adoption and feedback loops. Structured partnerships (preferred rental program, uptime guarantees, shared telematics) can shorten sales cycles and build installed-base advantages.

Monetize aftermarket and telematics — Telemetry-enabled maintenance, predictive replacement parts subscriptions, and consumables bundles convert one-time hardware sales into durable revenue streams, improving customer stickiness and margins.

Mitigate supply-chain and commodity risk — Diversify critical-component suppliers, qualify second-source alternators/controllers, and consider hedging strategies for raw-material exposure.

Targeted M&A and JV playbooks — Use the market’s concentration dynamics to locate tuck-in acquisitions that add channel depth, service footprints, or regional manufacturing competency. Prioritize assets that close capability gaps (e.g., emissions-compliant engines, telematics IP, or specialized duty-cycle expertise).

Time-to-market for new product introductions — compress by using modular sub-systems and engine OEM co-development.

Installed-base uptime — target measurable reductions in mean time to repair through parts availability and predictive maintenance programs.

Aftermarket revenue per unit-year — increase via service contracts and consumables conversion.

Channel fill rates and rental penetration — track both to evaluate product-market fit in high-usage segments.

Demand shock sensitivity — While growth is steady, the market is not immune to cyclical downturns in construction and mining investment. Scenario planning should include stress tests for demand contractions up to two years.

Regulatory shifts — Stricter emissions standards or regional bans on specific engine types would force accelerated product redesigns; maintain regulatory surveillance and contingency engineering capacity.

Technology displacement — Electrification of jobsite equipment and advances in battery energy density could erode certain portable-engine segments over the medium term. Track battery cost curves and hybrid architectures as hedges.

Competitive escalation — Incumbents with large balance sheets can accelerate feature migration and price competition; defend through differentiation, service, and channel lock-in.

PW Consulting’s full Engine-Driven Welders Market study is structured to be immediately operational for commercial and product teams. Highlights include:

Top-line market sizing and seven-year forecasting by product architecture and end-use verticals, built from a 2025 base and extended through 2032 using scenario-enabled CAGR paths.

Competitive benchmarking with product feature matrices, manufacturing footprints, and go-to-market positioning for the leading global and regional suppliers.

Detailed commercialization playbooks: channel entry strategies, rental conversion models, and dealer incentive structures geared to accelerate adoption in target verticals.

Aftersales and services playbook: telematics specifications, spare-parts assortment strategies, and subscription pricing templates designed to lift lifetime value.

Supply-chain risk assessment and procurement levers to reduce BOM volatility, including alternate-sourcing maps and parts localization scenarios.

Acquisition target screen and integration checklist for tuck-ins that enhance channel share, aftermarket capability, or regional manufacturing scale.

Regulatory watch-list and compliance roadmap tailored to major markets, including timing impacts on product roadmaps.

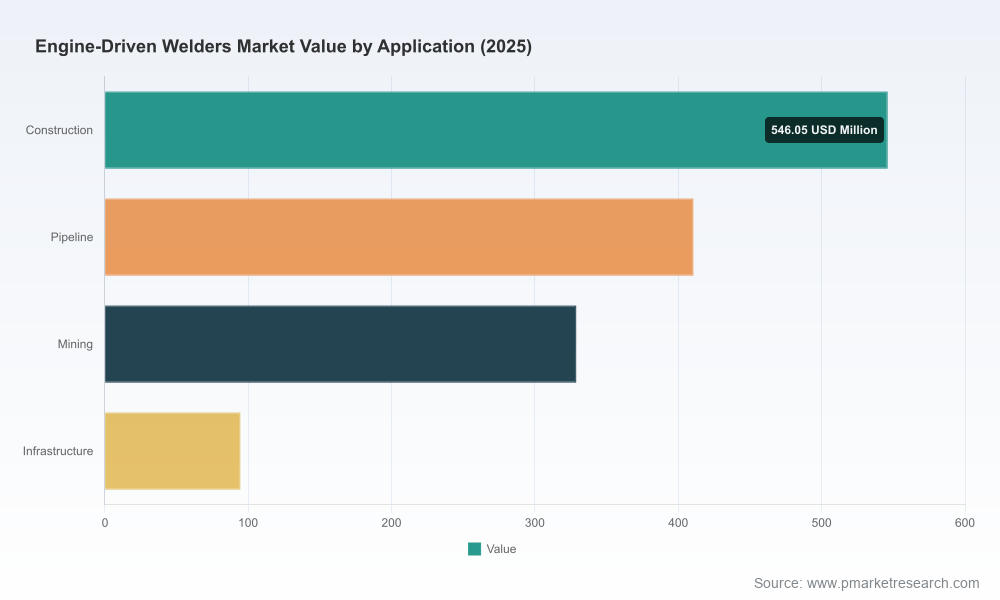

To preserve the strategic “trailer” effect, this primer intentionally omits the report’s full tabulated segmentation and regional share tables. Those detailed breakdowns — including the granular regional, type, and application splits that underpin the forecasting model — are accessible within the full PW Consulting report.

Book a 60-minute strategic briefing with PW Consulting to review how the modeled scenarios map to your product roadmap and channel plans.

Commission a 90-day quick-win program to pilot telematics and a rental-partner roll-out in one prioritized geography to validate TCO and uptime improvements.

Initiate OEM-engine R&D engagements to lock emissions-compliant platforms for the next-generation product suite.

Engine-driven welders remain a practical industrial device, but the competitive frontier is now about services, integration, and regulatory foresight rather than basic hardware alone. With the market growing at an approximate 4.91% CAGR and meaningful opportunities for margin expansion through aftermarket and channel strategies, 2026 is the year to convert incremental product improvements into structural advantage.

Contact PW Consulting to access the complete dataset, proprietary segmentation tables, and the vendor scorecard that power these recommendations.

For detailed analysis of this topic, please visit the official page:Engine-Driven Welders Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com