The Cost of Manual Tracking in Bulk Liquid Terminals

Other |

2026-03-05 08:20:00

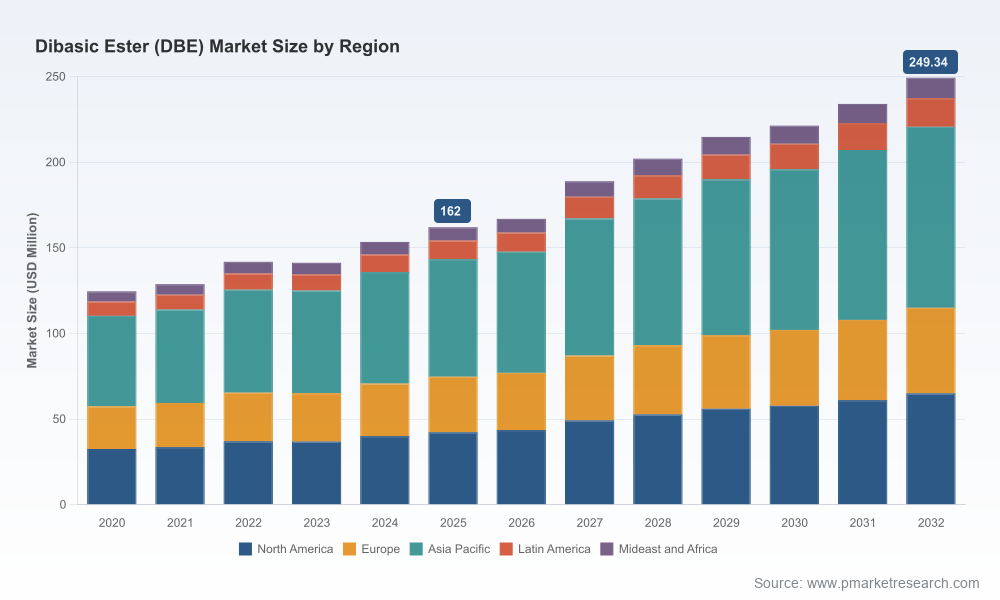

PW Consulting’s latest Dibasic Ester (DBE) Market study (base year 2025; historical 2020–2025; forecast 2026–2032) synthesizes what matters for executives who must convert regulatory pressure, sustainability momentum, and heterogeneous supply dynamics into concrete choices in 2026. The DBE market is on a steady expansion trajectory — our modelling reflects a compound annual growth rate of approximately 6.5% across the forecast window, with the global market moving meaningfully above its 2025 baseline by the end of the decade. This briefing sets out the strategic value of the full report, highlights high-conviction takeaways, and signals the tactical workstreams that will determine winners and losers next year. Detailed regional and application-level tables, plant-level capacity intelligence, and deal-scorecard outputs are intentionally withheld here to preserve the “trailer” function of this note and to encourage access to the full dataset and vendor-grade annexes on our site.

Dibasic Ester (DBE) Market

Regulatory acceleration is forcing formulation pivots. Global chemical governance and regional enforcement are tightening the universe of acceptable high-VOC and chlorinated solvents — DBE is increasingly positioned as a compliant alternative in multiple regulated markets. Executives must judge both timing and product specification to avoid late-stage reformulation costs.

Dibasic Ester (DBE) Market

Sustainability is moving from brand play to procurement condition. Bio-derived feedstocks and certified recycled-content DBE grades are moving from niche to commercial-scale viability; procurement teams will be asked to evaluate premiums against de-risked regulatory exposure and end-customer preferences.

Dibasic Ester (DBE) Market

Supplier concentration creates strategic dependency. The market’s structure exhibits a moderate level of concentration among a set of incumbent specialty producers and vertically integrated chemical groups — a fact that shapes negotiation strategy, contract tenors, and contingency planning.

Price & feedstock volatility will be a defining operating risk. Downstream formulators and coatings producers face margin pressure unless they adopt hedging approaches, dual-sourcing strategies, or integrated supply partnerships.

Decision-grade market sizing and trend analysis from 2020 through 2032, including alternative growth scenarios informed by regulatory stringency and bio-based conversion rates.

Demand-driver modelling linking end-market activity to DBE consumption intensity (coatings reformulation cycles, industrial cleaning adoption rates, plasticizer substitution pathways).

Supplier benchmarking and commercial scorecards — capacity, grade breadth, geographic coverage, sustainability credentials, and counterparty risk indicators.

Feedstock and pricing playbooks — comparative cost curves, margin impact analytics, and tactical procurement levers for 12–36 month planning horizons.

Scenario-based strategic options (e.g., build vs. buy, JV vs. off-take, licensing vs. contract manufacturing) with financial sensitivity and lead-time maps.

Implementation toolkits: RFP templates for secure sourcing, technical checklists for low-VOC reformulation, and M&A screening matrices keyed to strategic intent.

Large specialty chemical groups and integrated producers remain the backbone of DBE supply. Companies with legacy adipic and ester capabilities enjoy advantages in feedstock integration, grade breadth and the commercial reach necessary to serve global coatings and industrial accounts. Their strategic playbooks emphasize blended solutions, certified recycled-content grades, and bespoke technical support for formularies facing regulatory scrutiny.

European specialty players are orienting toward high-purity, low-VOC applications and enhanced technical services for demanding sectors (automotive, pharmaceutical intermediates, electronics). Expect continued product differentiation via low-emission formulations and tighter regulatory compliance positioning.

China-based high-volume producers are exerting competitive pressure on price and availability in regional and export markets. Their scale allows them to be price setters in certain corridors while also enabling investments in quality upgrades to reach specification-grade segments.

Japan and Korea specialists target extremely high-purity niches where quality tolerance and supply reliability command premiums — these suppliers are often indispensable for electronics and pharmaceutical supply chains.

The market concentration metrics in our analysis indicate a moderate aggregation of supply among a small set of global and regional players. That structure elevates the strategic importance of counterparty selection and long-term offtake arrangements.

Recent investments in bio-based DBE production and new low-VOC product introductions underline two concurrent industry responses: (1) securing bio-feedstock pathways to meet sustainability mandates; and (2) accelerating product launches to capture reformulation windows opened by regulatory enforcement.

Strategic partnerships between fermentation specialists and established ester producers — already announced for near-term commercialization — will be an early differentiator: first movers may command preferred supplier status for sustainability-conscious formulators.

Product & R&D strategy — Accelerate low-VOC and bio-based DBE variants into early adopter customer trials. Prioritize formulation stability and compatibility testing with incumbent resins to shorten adoption cycles. Allocate R&D spend to certification pathways (e.g., biodegradability, recycled-content verification) that unlock procurement mandates.

Supply chain & procurement — Adopt a layered sourcing approach: core long-term offtake agreements with incumbent producers for continuity, complemented by spot and regional suppliers to manage volume and price swings. Where possible, structure contracts with explicit sustainability KPIs tied to price or volume tiers.

Commercial go-to-market — For manufacturers and distributors, create differentiated value propositions (technical support, reformulation services, sustainability documentation) to defend margin as lower-cost entrants expand. For end-users, develop a supplier scorecard that weights regulatory compliance and lifecycle credentials alongside price.

M&A and partnership playbook — Targeted bolt-on acquisitions in specialty grades, fermentation partnerships, or regional distribution platforms can accelerate market access. Use our M&A screening templates to map acquisition targets by strategic fit, integration complexity, and deal economics.

Regulatory readiness — Build a regulatory roadmap tied to anticipated enforcement cycles. Prepare compliant formulations now to avoid last-minute reformulation expenses and supply disruptions when enforcement triggers accelerate demand for DBE alternatives.

Manufacturing & capacity planning — If contemplating greenfield capacity, incorporate lead-time sensitivity tied to bio-succinate feedstock availability and local permitting. If scaling via tolling or contract manufacturing, lock-in quality and traceability clauses to maintain grade integrity across the supply chain.

We provide board-ready scenario decks that show the P&L and cash-flow implications of key strategic choices (build vs. buy, premium bio-grade sourcing, long-term offtake vs. spot exposure).

Our supplier scorecards and plant-level intelligence enable procurement teams to shortlist counter-parties and draft negotiation playbooks with fact-based levers.

Market-entry playbooks and regulatory pathway maps give product, legal, and commercial teams an executable 6–18 month plan to move from pilot to scale.

For C-suite prioritization, we translate technical and regulatory complexity into three ranked strategic options — defend, diversify, or disrupt — each with recommended KPIs and investment ranges.

Granular regional and application-level demand splits, including bottom-up consumption models by end-use category.

Plant-level capacity maps and supplier contract archetypes that support negotiation and contingency planning.

Price-curve scenarios and feedstock sensitivity analyses tailored to alternative raw-material pathways (petrochemical vs. bio-derived routes).

Customer-level demand mapping and a prioritized list of pilot partners for early commercialisation of bio-DBE grades.

Conclusion — For organisations that will make or break market position in 2026, the key agenda items are clear: secure differentiated supply (quality + sustainability), accelerate product readiness for regulatory shifts, and use targeted partnerships to reduce technical and market risk. PW Consulting’s DBE Market study equips leadership teams with quantitative scenarios, supplier intelligence, and executable playbooks to decide confidently. Visit our report page for the comprehensive datasets and bespoke advisory offerings that convert this strategic briefing into operational commitment.

For detailed analysis of this topic, please visit the official page:Dibasic Ester (DBE) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com