Binders for Lithium‑Ion Batteries Market: Strategic Imperatives for 2026

Binders are the invisible enablers of lithium‑ion cell performance — a small fraction of bill of materials cost, but disproportionately influential on manufacturability, cycle life and safety. As we enter 2026, the global binders market sits at a strategic inflection point. Our PW Consulting base‑year synthesis (2025) values the global market at approximately USD 5.63 Billion, following a robust five‑year expansion from 2020. Under the baseline trajectory embedded in this study, the market is projected to continue expanding at a compound annual growth rate of 15.8% through 2032, reaching a multi‑billion dollar scale by the end of the forecast window. This report is designed as an executive map for commercial, procurement and investment leaders who must convert that growth projection into defensible 2026 actions.

Binders for Lithium Ion Batteries Market

Why this study is essential for decisions in 2026

- Timing of capital and capacity commitments: The binder market is expanding rapidly, but lead times for qualified, high‑purity production lines remain lengthy. Our analysis identifies the windows where commitments materially reduce technology and supply risk.

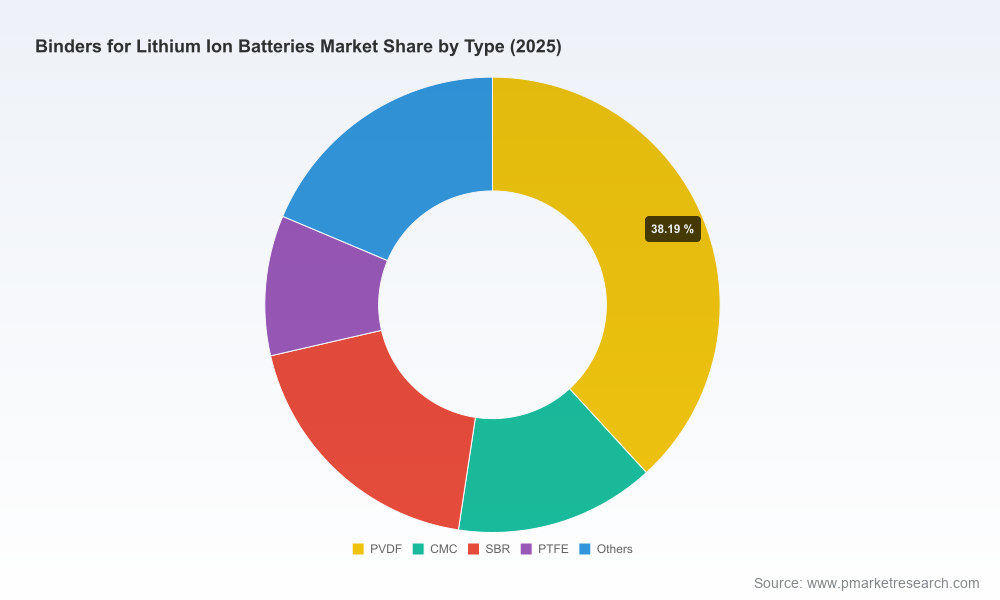

- Supplier and chemistry selection: Choices between PVDF, water‑based chemistries (CMC, SBR, PAA and others) and blended/co‑binder systems have knock‑on effects across cell design, electrode coating processes and downstream qualification with OEMs.

- Regulatory and qualification readiness: New ISO updates and OEM qualification gates introduced in 2025 require proactive test programs; failure to anticipate them can delay product launches by quarters.

- Risk mitigation and sourcing strategy: Raw‑material volatility and concentrated feedstock sources mean that procurement strategies must incorporate hedging, multi‑sourcing and design‑for‑material‑flexibility.

In short: 2026 will be a year where near‑term supplier choices and modest capital decisions determine whether companies capture disproportionate share of the next phase of growth.

Binders for Lithium Ion Batteries Market

Market dynamics shaping 2026 strategy

- Demand drivers remain structural: Vehicle electrification, grid storage deployments and continued demand from consumer electronics sustain long‑run upward pressure on binder volumes. While end‑market composition varies by region and customer segment, the aggregate demand curve in our base case supports the high‑teens CAGR embedded in this study.

- Raw material volatility compresses margins and forces reformulation: PVDF feedstock prices have exhibited significant swing — industry monitoring indicates volatility in the mid‑teens to mid‑twenties percentile range — while CMC and SBR feedstock variation has raised costs materially in 2025. These swings have prompted formulators to optimize co‑binder ratios and to accelerate water‑based technology adoption.

- Regulatory and policy tailwinds for water‑based systems: Environmental mandates and procurement incentives are accelerating displacement of solvent‑based processes. Adoption of water‑based binder processes can reduce NMP usage in electrode manufacturing by up to 90%, a material compliance and operating‑cost consideration for cell manufacturers.

- Government support and capacity additions: DOE‑backed supply‑chain initiatives and other public investments have catalyzed significant capacity additions in North America, supporting local PVDF and SBR production. These programs are changing lead‑time dynamics and creating new domestic sourcing options for OEMs and cell makers.

- Industry qualification bar is rising: ISO updates released in 2025 tighten electrolyte‑compatibility testing and performance thresholds. For commercial teams, earlier engagement in test programs and longer qualification pipelines should be factored into 2026 product roadmaps.

Technology and formulation trends — what to watch

- Water‑based chemistries go mainstream: CMC/SBR systems and advanced water‑borne PVDF/suspension emulsions are being optimized to match solvent‑based performance, enabling lower emissions and simplified factory operations.

- Binders engineered for silicon‑dominant anodes: PAA and modified CMC chemistries, along with multi‑functional co‑binders, are rapidly moving from lab to line to cope with silicon expansion in anode formulations.

- Multi‑function binders: Next‑generation products emphasize adhesion, mechanical resilience, electrolyte compatibility and ionic transport; suppliers increasingly market binders as enablers of higher volumetric and gravimetric energy density, not just as adhesives.

- Process compatibility and scale‑up: Gelation prevention, viscosity control and coating rheology remain practical bottlenecks; suppliers that can deliver scaleable, predictable binder batches create a tangible competitive advantage for cell manufacturers.

Competitive landscape — implications for buyers and investors

The supplier space blends legacy polymer companies with specialty chemical houses and regional formulators. Notable players include technology‑centric manufacturers and commodity suppliers; each brings a distinct set of strengths:

Binders for Lithium Ion Batteries Market

- Technology leaders with specialty PVDF offerings: Incumbent PVDF suppliers deliver high‑performance grades optimized for tensile strength and electrochemical stability. These players command trust in critical electrode systems where long cycle life is prioritized.

- Specialists in water‑based and anode binders: Suppliers focused on CMC/SBR and water‑borne formulations are benefiting from environmental mandates and the move to silicon‑enabled anodes.

- Global distributors and integrators: Companies supplying a broad binder portfolio and logistics capability are winning multi‑site OEM contracts by simplifying qualification and securing multi‑region supply continuity.

Recent strategic moves underline these dynamics. In early 2025, a major chemical supplier announced U.S. manufacturing expansions for anode binders, reflecting a broader trend of localized capacity to de‑risk supply chains. Another specialty manufacturer announced preparations for a new production line in Texas to be online in 2026 — a clear signal of supplier investment timed to OEM localization. Taken together with the market concentration metrics we track (CR3 ≈ 29.4%, CR5 ≈ 36.2%), the sector shows moderate concentration: recognized global leaders coexist with a competitive field of capable regional players and emerging specialists. For buyers, that means tangible opportunity to negotiate but also the need to qualify multiple partners to manage supplier risk.

What the full PW Consulting report delivers

Our market study provides operational intelligence designed for immediate use in 2026 planning cycles. Key deliverables include:

- Macro and micro market sizing (historical 2020–2025 and granular forecast 2026–2032) with scenario paths aligned to EV penetration and ESS deployment assumptions.

- Supply‑chain maps and capacity tracking for PVDF, SBR, CMC and alternative binders — including planned expansions and lead‑time impact analysis.

- Price‑elasticity and raw‑material sensitivity models showing the P&L impact of feedstock swings and plausible disruption scenarios.

- Supplier scorecards and qualification checklists, with technology fit recommendations for common cell chemistries.

- Procurement playbooks: contracting structures, inventory strategies and hedging options tailored for binders.

- Regulatory and certification playbook, covering ISO updates, OEM qualification timelines and environmental compliance pathways.

- Strategic action roadmaps: investment trigger points for capacity, M&A screening lenses, JV structuring options and go‑to‑market recommendations for binder producers.

Scenario planning and recommended near‑term actions for 2026

- Base case (our central 15.8% CAGR): Prioritize multi‑supplier qualification, lock medium‑term offtake with incremental price collars, and invest modestly in water‑based process readiness to keep margin upside.

- Upside (accelerated EV and ESS adoption): Accelerate long‑lead capex commitments, secure feedstock supply agreements and consider strategic equity stakes in regional binder capacity to guarantee supply and capture margin.

- Downside (raw material shock or slower OEM adoption): Implement contingency reformulations, defer marginal capacity expansions, and deploy flexible procurement clauses that allow rapid chemistry substitution without requalification delays.

Immediate tactical steps we recommend for 2026 execution:

- Initiate parallel qualification streams with at least two chemically distinct binders for each critical cell platform.

- Engage early with suppliers announcing capacity additions to shape product specifications and secure first‑wave allocations.

- Implement raw‑material monitoring dashboards and negotiate indexed pricing where possible to smooth input cost volatility.

- Leverage public funding and DOE programs to co‑fund capacity or pilot lines that lower customer pick‑up risk and shorten qualification timelines.

Conclusion — a practical call to action

Binders will remain a strategic, not just tactical, consideration for cell and pack manufacturers in 2026. The interplay of robust demand growth, raw‑material swings, regulatory tightening and targeted capacity investments creates both risk and opportunity. Our PW Consulting study translates those macro forces into actionable decisions — from procurement and qualification sequencing to capex timing and partner selection.

We have intentionally presented a high‑signal executive view here while withholding detailed segment matrices and granular regional/application breakouts to preserve the value of the full dataset and modeling. To access the complete scenario models, supplier scorecards, price sensitivity tools and the full set of operational recommendations that support 2026 decision‑making, please visit the full research release on our site or contact your PW Consulting analyst for a briefing and data package.

For detailed analysis of this topic, please visit the official page:Binders for Lithium Ion Batteries Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com