Dry Eye Syndrome Market: Insights and Competitive Analysis

Other |

2026-02-24 09:21:53

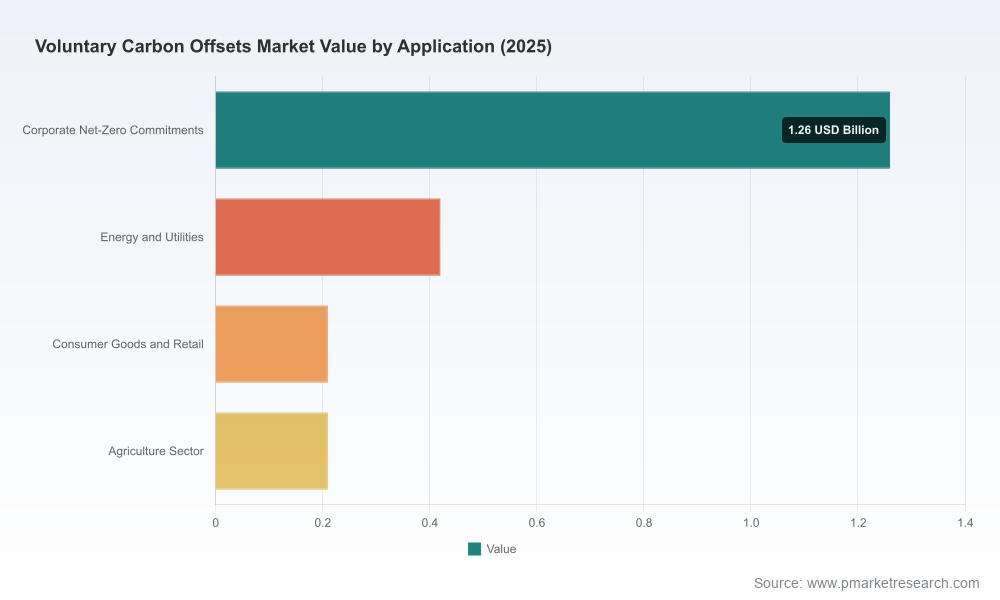

The voluntary carbon offsets market is entering a phase of rapid structural expansion and quality consolidation that will materially affect corporate decarbonization strategy in 2026. Our analysis shows the market expanding from a base of approximately USD 2.1 billion in 2025 to an expected USD 13.6 billion by 2032, implying a high‑growth trajectory underpinned by a 30.7% CAGR through the forecast window. That headline growth masks meaningful near‑term volatility (a volatile 2020–2025 history) and a supplier landscape that remains highly fragmented (CR3 ~24.6%, CR5 ~26.2%).

Voluntary Carbon Offsets Market

For corporate leaders planning 2026 budgets, procurement windows, or M&A plays, these dynamics create an urgent need to reframe voluntary offsets not as a commodity purchase but as a strategic portfolio instrument — one that requires active governance, scenario planning, and supplier/credit quality integration into core procurement and sustainability functions.

Voluntary Carbon Offsets Market

Budgeting and capital allocation: The market’s steep growth trajectory means the cost and availability assumptions companies used in 2024–25 are likely outdated. Finance teams must model both price convergence and bifurcation — inexpensive nature‑based credits at the low end of the price spectrum versus rapidly appreciating tech‑based carbon dioxide removal (CDR) credits — when setting 2026 allowances and procurement windows.

Voluntary Carbon Offsets Market

Procurement strategy: Offsets are transitioning from spot purchases to multi‑year contracted portfolios. Corporates should move quickly to design layered procurement strategies that combine short‑term compliance with medium‑term offtakes for higher‑integrity credits and strategic investments in removals. This reduces exposure to price shocks and supply shortages while preserving access to high‑integrity inventory.

Regulatory and compliance risk: Emerging frameworks — from ICVCM’s Core Carbon Principles to EU transparency rules and the CRCF regulation — are already reshaping what constitutes “bankable” credits. Companies that ignore evolving certification baselines risk stranded assets in their offset portfolios and disclosure gaps in sustainability reporting.

Scope 3 and supply chain alignment: With standard‑setting bodies and registries moving to enable Scope 3 use cases, corporate decarbonization teams should prioritize credits and methodologies that can be defensibly mobilized against supply‑chain emissions. Early alignment with registry programs and supply‑chain partners creates first‑mover advantage in supplier decarbonization initiatives.

M&A and partnerships: The market structure — dominated by many specialist providers rather than a few incumbents — creates fertile ground for bolt‑on acquisitions, strategic partnerships with originators, and investments into verification or digital traceability capabilities.

Our report is intentionally practical: beyond market sizing and topline forecasts, it provides tools and playbooks that corporate teams can deploy in 2026. Key deliverables include:

Each module pairs actionable templates with anonymized benchmarking, so procurement, sustainability, and legal teams can move from insight to execution within 60–90 days.

The voluntary market remains fragmented and service‑oriented. The competitive set includes a mix of project originators, brokers, and integrated service providers. Below is a high‑level strategic read on selected players and the roles they play in corporate supply chains:

3Degrees (United States) — Integrated provider combining credits with sustainability consulting. Strength: turnkey solutions for corporates seeking single‑vendor accountability (https://3degreesinc.com).

Earthly (United Kingdom) — Focused on developing high‑integrity project credits. Strength: strong product development and methodology work in nature‑based solutions (https://earthly.org).

ClimatePartner (Germany) — Offers verified credits and offsetting tools geared to corporates. Strength: tight integration with corporate reporting and client services (https://climatepartner.com).

South Pole (Switzerland) — Large originator and verifier with global project footprint. Strength: scale in project management and certification (https://southpole.com).

EKI Energy Services (UK) — Renewable energy and energy‑efficiency focus. Strength: project execution in renewables/efficiency sectors (https://ekenergy.co.uk).

NativeEnergy (US) — Specialises in conservation forestry and community projects; strong reputational positioning for corporates seeking community co‑benefits (https://native.ec).

Terrapass (US) — Retail and SME solutions; useful benchmark for mass‑market productization of credits (https://terrapass.com).

Carbon Credit Capital (US) — Project sourcing and brokerage, useful for tailored portfolios and bespoke offtakes (https://carboncreditcapital.com).

Greenfleet (AU/US outreach) — Reforestation and conservation specialist; relevant for biodiversity‑linked objectives (https://greenfleet.org.au).

Strategic takeaways: incumbents that combine origination with verification and corporate services are best positioned to capture multi‑year contracts; smaller specialists provide access to niche, high‑integrity credits but expose buyers to supply concentration risk. Expect consolidation and vertical integration as buyers seek simplified governance.

Standards and regulation: The Core Carbon Principles and recent EU implementing rules are raising the bar for what is considered acceptable in corporate disclosures. Companies should prioritize credits aligned to these emerging baselines to avoid future write‑downs.

Methodological innovation: New methodologies and jurisdictional approaches, such as recent REDD+ methodology launches and the Scaling JREDD+ Coalition, are increasing supply of jurisdictional credits but will take time to scale in marketable form. Corporates should evaluate jurisdictional instruments for strategic partnerships but avoid over‑reliance in the near term.

Registry and program updates: Leading registries are updating standards to align with CCPs and Scope 3 use cases; for example, Verra’s program updates and Scope 3 program announcements create new opportunities for supply‑chain applications.

Price dispersion: Pricing remains highly tiered. Nature‑based credits typically trade at the lower end of the spectrum, while emerging tech‑CDR credits trade materially higher. That dispersion will persist as quality differentials, co‑benefits, and permanence tradeoffs are priced in.

0–90 days: Conduct a portfolio audit of current offset holdings and disclosure exposure; establish an internal credit‑quality baseline tied to ICVCM/registry alignment; start 2026 procurement with layered purchase commitments that combine spot and forward offtakes.

3–12 months: Execute at least one strategic offtake for higher‑integrity removals, implement contractual safeguards for delivery and permanence, and integrate offset procurement into broader procurement and supply‑chain governance frameworks. Consider small equity stakes or JV pilots with originators for preferential supply.

The voluntary carbon market in 2026 presents both strategic risk and distinctive opportunities. Rapid market growth, evolving standards, and a fragmented supply base mean companies that move early to professionalize procurement, embed quality‑led decision criteria, and align offsets with broader decarbonization pipelines will materially reduce execution risk and secure cost‑effective access to high‑integrity credits.

PW Consulting’s full Voluntary Carbon Offsets Market study contains the detailed datasets, supplier scoring matrices, contract language, and scenario models needed to operationalize the approach outlined above. We have deliberately withheld granular segmentation tables and proprietary project‑level datasets from this preview to protect client value and to ensure that tactical execution tools are accessed via our full report portal.

To obtain the complete market dataset (including regional and application splits, supplier scorecards, and downloadable procurement templates), contact PW Consulting or visit our report page for access to the full suite of strategic playbooks and models.

For detailed analysis of this topic, please visit the official page:Voluntary Carbon Offsets Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com