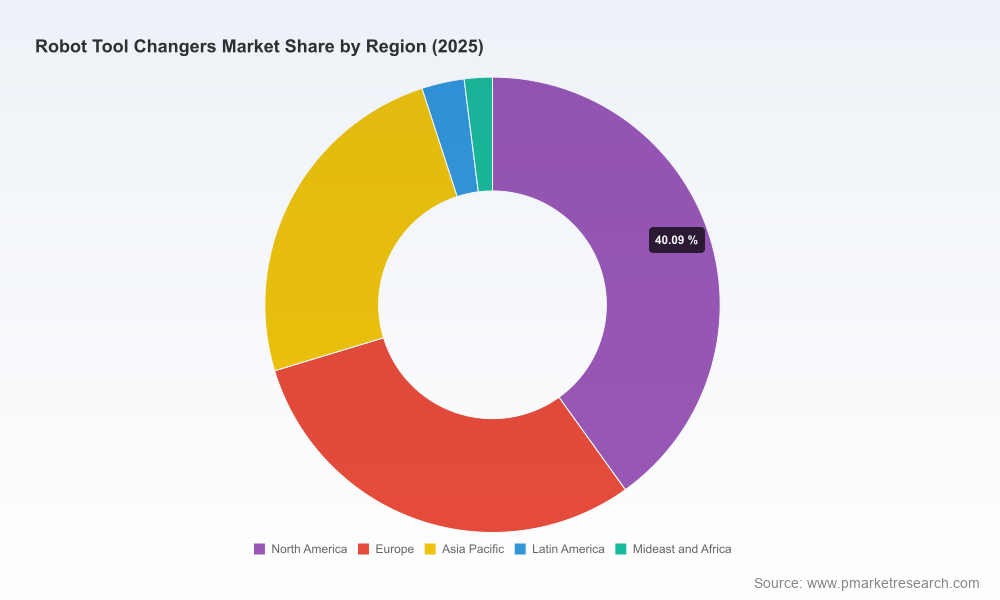

Robot Tool Changers Market — Strategic Briefing for 2026 Decision Makers

As automation continues its steady march from isolated cells toward fully reconfigurable, mixed-technology production lines, tool changers have moved from being auxiliary accessories to strategic enablers. PW Consulting’s new Robot Tool Changers Market study (base year 2025) maps this transition across history and a forward-looking forecast window to 2032. This briefing synthesizes the report’s most consequential implications for corporate strategy in 2026 — revealing the market’s trajectory, competitive dynamics, regulatory inflection points and the pragmatic playbooks procurement and R&D teams will need to execute successful deployments. While this article demonstrates the depth of our analysis, it intentionally withholds proprietary segment-level tables and line-item dollar splits; the full intelligence package is available through our research portal.

Robot Tool Changers Market

Market trajectory: growth, scale and what it means for 2026 plans

Between 2020 and 2025 the robot tool changers market exhibited sustained expansion driven by rising demand for flexible automation, increased adoption of collaborative robot cells, and a rising emphasis on quick changeover to support high-mix, low-volume manufacturing. Our base-year analysis captures that momentum and projects continued acceleration across the forecast period (2026–2032). The market is expected to compound at a robust rate, reflecting both organic replacement cycles and new installations tied to reshoring and advanced manufacturing initiatives.

Robot Tool Changers Market

For 2026 strategic planning, the implication is clear: tool changers will be a material line item in automation CapEx and an enabler of operational agility. Leading manufacturing firms should budget for not only hardware acquisition but also integration engineering, operator training and lifecycle maintenance. Sourcing strategies that assume static demand or slow uptake will be outpaced by competitors who embed tool-change capability into their modular automation roadmaps.

Robot Tool Changers Market

Key demand drivers and strategic levers

- Modularity as competitive advantage. Manufacturers seeking rapid product changeovers are prioritizing robotic cells designed for tool-agnostic redeployment. Tool changers convert robot arms into multi-role assets — shortening changeover time, lowering floor-space requirements and increasing effective robot utilization.

- Rise of collaborative and lightweight robots. The proliferation of cobots has broadened the addressable market for smaller, pneumatic and electrically integrated tool changers. This trend creates cross-sell opportunities for suppliers who can certify tool changer compatibility across multiple OEM platforms.

- Service-led deployment models. As complexity grows, many end-users will favor bundled hardware-plus-services agreements (commissioning, preventative maintenance, spare-part provisioning and digital monitoring) to de-risk integration and accelerate ROI realization.

- Regulatory and safety harmonization. Updated global standards — including ISO 10218-2:2025 — are reshaping expectations for system-level validation and safety-certified interfaces, increasing the premium for compliant, well-documented tool changer systems in regulated industries.

Inhibitors and strategic mitigations

- Integration complexity. Tool changers vary in mechanical interface, pneumatic/electrical pass-throughs and control semantics. Firms must invest in standardized mechanical flanges, interface adapters and software abstraction layers to avoid costly point solutions.

- Supply chain volatility. Tariff policies and localized sourcing requirements are prompting manufacturers to reconfigure supply chains; pragmatic buyers should pursue multi-sourced components and regional manufacturing partners to lower exposure.

- Safety compliance burden. New or revised safety standards raise the bar on validation testing. Early engagement with compliance engineers and independent safety assessors can prevent late-stage rework.

Product and technology roadmap

Tool changers are converging along several technological vectors that will shape vendor selection and product development in 2026:

- Smart, sensorized interfaces. Integrated force/torque sensing and quick-status diagnostics accelerate troubleshooting and enable more advanced pick-and-place strategies where tool sensing informs adaptive motion.

- Universal mechanical interfaces. Market leaders are investing in flange compatibility and modular adaptors to reduce integration time. The winners will be those that combine mechanical neutrality with robust electrical and pneumatic pass-through standards.

- Electro-pneumatic hybrids. Designers are combining electrical signaling for communication with pneumatic actuation where weight and cost are critical — especially in small-payload cobot applications.

- Software and digital twin support. Compatibility with robot controllers, cell-level orchestration software and digital twin simulation tools will be a decisive procurement criterion for high-changeover environments.

Competitive landscape — who matters and why

The market exhibits a meaningful degree of concentration: a small set of well-established component and automation specialists control a sizeable portion of revenue and channel access, while a growing tier of specialized newcomers is competing on speed-to-deploy and application fit. In broad terms, the top three players account for roughly two-thirds of market revenue, and the top five approach roughly four-fifths — a dynamic that favors incumbents with deep distribution networks, certification footprints and system-level IP.

Highlighted vendor positions from our study (representative, not exhaustive):

- Stäubli (Pfäffikon, Switzerland) — Known for its MPS series automatic tool changers that support high payloads with ISO-standard flange compatibility. Stäubli’s emphasis on modularity and payload range makes it a preferred choice for heavy-duty industrial cells and OEM robot providers.

- Zimmer Group (Markgröningen, Germany) — Offers a broad portfolio spanning automatic, manual, pneumatic and magnetic interfaces. Zimmer’s strength lies in configuration breadth and manufacturing systems integration for high-mix operations.

- SMC Corporation (Tokyo, Japan) — A leader in pneumatic tool changers and grippers for collaborative robots, SMC brings manufacturing scale and pneumatics expertise — particularly attractive where force control and lightweight tooling matter.

- ATI Industrial Automation (Oxford, NC, USA) — Specializes in tool changers combined with force/torque sensing. ATI’s value proposition centers on precise in-line measurement capabilities that enable more advanced quality assurance at the point of operation.

- SCHUNK (Lauffen am Neckar, Germany) — Known for pneumatically actuated automatic systems with safety-focused features (e.g., self-retaining mechanisms in air-loss scenarios). Recent product promotions emphasize machine-tending use cases and reduction of manual changeover risk.

- Destaco (Auburn Hills, MI, USA) — Focuses on cobot end-of-arm tooling and manual changers with utility pass-throughs for air and power — a practical choice for materials-handling and lower-capex projects.

- Robot System Products (Germany) — Markets collaborative-focused systems such as the CoboShift family, which speed automated exchanges in flexible cell designs.

- SmartShift Robotics (USA) — A newer entrant pushing universal tool changer concepts emphasizing rapid redeployment and simplified commissioning for short-run production converters.

Each vendor brings different strengths — payload range, sensor integration, pneumatics, cobot compatibility, or service models — and the right supplier choice depends on a buyer’s mix of payload needs, safety requirements, integration resources and lifecycle support expectations.

Regulatory and supply considerations shaping 2026 procurement

- Standards landscape. ISO 10218-2:2025 introduces updated global safety requirements that affect how tool changers are validated as part of robot systems. In the U.S., ANSI/RIA guidance remains a key reference for integrating robots into completed machinery. Buyers should insist on documented compliance packages as part of any procurement RFP.

- Tariffs and localization. Geopolitical and tariff dynamics are driving manufacturers to reassess sourcing footprints. Organizations planning installations in 2026 should include scenario analyses for lead-time variance and component reshoring costs in their procurement models.

What the full PW Consulting report delivers for 2026 execution

Our full market study goes beyond trend narrative to deliver operationally actionable insight for executives, procurement leaders and R&D planners. Key deliverables include:

- Validated market sizing and scenario-based forecasts (2026–2032) to support budget planning and investment prioritization;

- Proprietary vendor scorecards that evaluate suppliers across technical compatibility, service footprint, certification readiness and total cost of ownership;

- Integration playbooks and an ROI modelling toolkit tailored to common use-cases (machine tending, electronics assembly, medical device production, chemical handling and high-mix assembly lines);

- Compliance checklists aligned to the latest standards and recommended test protocols to reduce commissioning delays;

- M&A and partnership scouting lists identifying strategic targets and bolt-on capabilities for OEMs and system integrators;

- Operational templates for spare-parts stocking, lifecycle maintenance contracts and field-upgrade paths that reduce downtime and capex waste.

To maintain the strategic “trailer” effect: the public summary above surfaces the analytical themes and strategic prompts you need for initial planning. The detailed, segmented datasets, vendor-level financial benchmarks, and the step-by-step procurement and integration checklists are reserved for report subscribers and clients who require executable intelligence to act in 2026.

Immediate strategic actions for 2026

- Embed tool changer scenarios into your capital planning cycles now — treat them as enablers of flexible capacity, not optional peripherals.

- Prioritize suppliers who offer documented safety compliance and a clear roadmap for software/communication compatibility with your fleet of robot controllers.

- Design supply resilience into procurement: qualify multiple vendors, require regional spares, and model tariff exposure in TCO analyses.

- Adopt a service-first approach when working with smaller integrators or new suppliers — pilot projects with clear KPIs (changeover time, uptime, mean-time-to-repair) de-risk scale-up.

PW Consulting’s Robot Tool Changers Market study is crafted to move decision-makers from conceptual intent to executable programs. If your 2026 plans involve reconfigurable automation, mixed-technology production cells, or a shift toward flexible manufacturing, the full report provides the granular segmentation, vendor benchmarking and procurement playbooks required to turn opportunity into measurable advantage. For access to the complete dataset, supplier scorecards and industry-grade implementation templates, please consult our research portal or contact PW Consulting directly.

For detailed analysis of this topic, please visit the official page:Robot Tool Changers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com