SSD Market 2026: Strategic Imperatives for Leaders — A PW Consulting Preview

Executive snapshot

The global Solid State Drive (SSD) market is entering a decisive phase in 2026. After a period of steady expansion from 2020–2025, our base-year analysis (2025) shows the industry accelerating into a high-growth trajectory with a compound annual growth rate (CAGR) of 19.9% across the 2026–2032 forecast window. The market size is projected to expand materially over this period, roughly tripling by the end of the forecast horizon. For executives making procurement, product, investment, and M&A decisions in 2026, this is not an incremental market — it is the epicenter of near-term infrastructure and AI compute economics.

Solid State Drive (SSD) Market

Why this preview matters for 2026 decision-making

- Timing matters: The 2026 planning cycle is the point at which corporate budgets, capacity commitments, and vendor roadmaps synchronize with a structural supply-demand inflection in NAND flash. Tactical decisions taken now will determine cost exposure and performance positioning through the rest of the decade.

- Scale and speed are strategic levers: Rapid SSD adoption in data centers, AI training/inference clusters, edge compute, and high-performance client systems is changing how CIOs and product leaders define TCO and performance SLAs.

- Risk concentration is real: Market concentration among leading suppliers is high, which increases supplier power and the systemic impact of capacity constraints or policy-driven disruptions.

Market snapshot — the macro view

PW Consulting’s longitudinal dataset captures market performance from 2020 through our base year, 2025, and projects an aggressive expansion beginning in 2026. The market demonstrated resilient demand during 2020–2025 and enters 2026 with momentum driven by hyperscale AI workloads, enterprise modernization, and new form-factor adoption. Our models forecast the market continuing to scale at ~19.9% CAGR through 2032, with the absolute market reaching levels that will reshape capital allocation across OEMs, hyperscalers, and component suppliers.

Solid State Drive (SSD) Market

Two structural takeaways underpin this macro picture. First, performance-led upgrades (NVMe, PCIe Gen4/Gen5 transitions, and new E3 form factors) are creating durable pockets of premium pricing. Second, high-capacity QLC and multi-terabyte offerings are redefining cost-per-TB economics for archive and AI datasets. Together, these forces create both margin expansion opportunities and sourcing stress points for buyers.

Solid State Drive (SSD) Market

Key dynamics affecting 2026 decisions

- Committed NAND capacity and scarcity: Industry intelligence indicates most NAND flash capacity for 2026 is already committed. High-density NAND is effectively sold out in key markets, and major cloud providers have locked capacity to support AI projects. This reduces buyers’ optionality and elevates the strategic value of long-term supplier relationships.

- Inventory and stockout risk: Multiple module manufacturers are reported to carry NAND inventories that will last only into early 2026, with stockouts beginning as early as March and shortages becoming widespread after Q2. This front-loads sourcing risk into the first half of 2026.

- Upstream financing pressure: Some NAND foundries and suppliers are demanding multi-year cash prepayments from customers as a condition of allocation. Buyers must assess working capital impacts and negotiate favorable terms or seek alternative supply strategies.

- Regulatory fragmentation: Export controls on advanced semiconductor manufacturing equipment and select inputs are restricting supply-chain access for certain entities — a factor that can alter supplier footprints, lead times, and long-term capacity expansion plans.

Competitive landscape — what leaders are doing

The SSD supplier ecosystem combines vertically integrated incumbents, specialized flash foundries, controller vendors, and ODMs. Market concentration is significant: the top three players control a majority share, and the top five capture an even larger portion of industry revenue. That concentration has immediate implications for negotiation leverage, innovation pacing, and consolidation risk.

- Samsung Electronics (Suwon, South Korea): A technology and scale leader, with flagship enterprise SSDs characterized by extreme read/write performance. Samsung’s vertical integration across memory fabrication and controller R&D keeps it at the forefront of premium, high-capacity offerings.

- SK hynix (Seoul, South Korea): Focused on high-performance enterprise SSDs and advancing high-layer QLC NAND processes that push capacity density. Their product roadmaps reflect an emphasis on cost-effective large-capacity solutions.

- Micron Technology (Boise, USA) & Crucial: Micron is scaling Gen5 NVMe and very high-capacity drives for hyperscale and enterprise customers. Its strategy combines product breadth with manufacturing investments to secure high-density supply.

- Kioxia (Tokyo, Japan): An early mover on ultra-high-capacity NVMe drives that are targeted at generative AI and dense data applications; recent sampling activities indicate a focus on new form factors and customer validation cycles.

- Western Digital / SanDisk (California, USA): Competing across consumer, client, and enterprise segments, with strategic supply agreements intended to lock in volume and revenue stability.

- Solidigm, Seagate, Corsair, Kingston, ADATA, Apacer, ATP, Phison: These firms cover niches from hyperscale SSDs to gaming and industrial drives, and include controller specialists (e.g., Phison) that influence performance differentiation and time-to-market for OEMs.

Recent corporate moves underscore how competition is playing out: high-capacity product sampling by leading vendors, multi-year supply agreements from Western Digital to secure demand, and controller partnerships and extensions to address AI workloads. These are not isolated product announcements — they are tactical maneuvers to capture allocation and revenue in a constrained cycle.

What PW Consulting’s full report includes (practical deliverables)

Our full SSD Market research report is structured to be operationally useful to procurement heads, product managers, CTOs, and corporate strategists. It contains:

- Proprietary time-series market sizing (2020–2032) with scenario variants for demand shocks and capacity ramp changes.

- Supply-chain risk heat maps and supplier scorecards that evaluate technical roadmap, financial strength, allocation policies, and geopolitical exposure.

- Procurement playbooks and contracting templates oriented around multi-year allocation, price-indexing clauses, and prepayment risk mitigation.

- TCO and performance models for NVMe vs SATA/SAS transitions, factoring in density, endurance, and power consumption for data-center and edge deployments.

- Go-to-market frameworks for vendors and OEMs including segmentation strategies, pricing tactics, and feature differentiation using controller/software stacks.

- Scenario-driven strategic options for vertical integration, capacity co-investment, and strategic inventory staging.

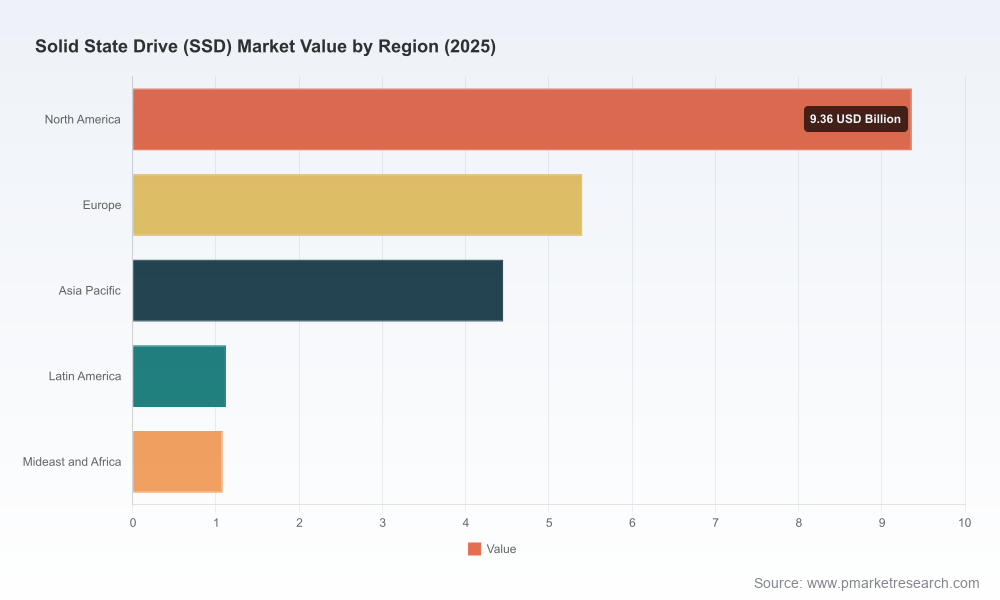

Note: This preview intentionally omits the granular segment-level revenue breakdowns and regional/application percentages found in the full dataset. Those segmented insights — including interface, capacity band, and regional composition across the historical and forecast periods — are available only in the full report and live data workbook.

Actionable strategy checklist for 2026

- Secure supply early: Prioritize multi-year agreements with allocation guarantees and include clauses that balance supplier cash demands with buyer protections (escrow, performance milestones, or inventory-sharing mechanisms).

- Stress-test working capital plans: Model the impact of prepayment demands on liquidity and consider staged payment structures or partnership financing with financiers that specialize in semiconductor supply chains.

- Diversify controller and firmware partners: Use controller suppliers and reference designs to shorten development cycles; partnering with established controller vendors mitigates integration risk as Gen5 and new form factors proliferate.

- Design for modularity: Make system architectures SSD-agnostic where possible to enable rapid supplier substitution based on availability and price shifts.

- Prioritize software differentiation: For vendors, develop firmware and management software that extract performance from lower-cost NAND (e.g., QLC) while delivering predictable QoS to enterprise customers.

- Hedging and inventory strategies: Evaluate pre-emptive inventory buys for critical workloads, but balance against obsolescence and warranty exposure; use staged rollouts for high-density drives to manage risk.

- Regulatory contingency planning: Build alternative sourcing and manufacturing scenarios that accommodate export-control developments and regional policy shifts.

Strategic scenarios to model in 2026 planning cycles

- Constrained supply, high demand: Prioritize flagship workloads, negotiate long-term capacity, and accept higher unit costs for guaranteed supply.

- Capacity re-expansion: If new fabs come online faster than expected, be ready to renegotiate terms or opportunistically refresh equipment at lower price points.

- Geopolitical fragmentation: Implement dual-track sourcing and qualify regional vendors to avoid single-country exposure.

Conclusion — the takeaways for executives

The SSD market in 2026 is both an opportunity and a strategic test. Growth dynamics driven by AI, hyperscale, and client-performance renewals are reshaping value chains and supplier economics. At the same time, committed NAND capacity, inventory timing, prepayment demands, and regulatory friction create real and immediate procurement and design risks. For organizations that act now — securing diversified supply lines, embedding flexibility into architecture, and using data-driven contracting tactics — the market expansion represents a sustainable competitive advantage. For those that delay, the 2026 allocation environment risks materially higher costs and constrained innovation windows.

PW Consulting’s full SSD Market report provides the datasets, scenario models, supplier scorecards, and playbooks necessary to turn these insights into executable plans. This preview highlights the strategic contours and actionable priorities for leaders, while withholding the granular segment-level tables that are essential for detailed procurement and product planning. Access the complete research and interactive data workbook to translate our forecasts into your 2026 operational and capital decisions.

For detailed analysis of this topic, please visit the official page:Solid State Drive (SSD) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com