Ignition Coil Market: Strategic Implications for 2026 Decisions — A PW Consulting Preview

As OEMs, tier suppliers, aftermarket players, and private equity firms plan their 2026 roadmaps, the ignition coil market presents a blend of steady growth, supply-side volatility, and compliance-driven product evolution. PW Consulting’s forthcoming Ignition Coil Market study (base year 2025; historical 2020–2025; forecast 2026–2032) synthesizes macro trajectories with actionable operational playbooks. This preview highlights the study’s strategic value for executives making resource allocation, sourcing, and M&A decisions in 2026, while reserving the full segmentation intelligence for the complete report.

Ignition Coil Market

Market trajectory at a glance — what leaders need to know

After a period of recovery and incremental product innovation through 2020–2025, the ignition coil market is moving into a phase of measured, technology-led expansion. In USD terms (expressed in billions), market size rose from roughly 9.5 in 2020 to approximately 11.8 in 2025. PW Consulting’s modeling indicates a continuation of that growth through the 2026–2032 forecast window, propelled by combustion-optimization requirements, aftermarket replacement demand, and regulatory tightening. Our compound annual growth rate (CAGR) through the forecast is 4.4%.

Ignition Coil Market

These headline numbers matter because they frame three practical planning constraints for 2026:

Ignition Coil Market

- Capital allocation horizons: suppliers should plan multi-year investments in coil R&D and manufacturing capacity on the assumption of steady mid-single-digit growth, rather than rapid expansion or steep contraction.

- Product prioritization: competition will intensify around design features that deliver measurable emission and fuel-efficiency advantages, making targeted product roadmaps imperative.

- Supply-chain strategy: the steady growth profile reduces the risk of demand collapse but amplifies the strategic importance of materials and tariff management.

Market dynamics that will shape 2026 strategy

Our research identifies four interlocking dynamics that should be at the top of every board and procurement agenda in 2026.

- Material concentration and sourcing risk. In 2025 copper was formally designated a critical mineral by the U.S. Geological Survey. Ignition coils rely on high-purity copper windings and iron cores; this designation, coupled with tariff adjustments (notably Section 232 changes effective July 30, 2025), has introduced new cost and availability pressures. For 2026, executives must assume continued price volatility and evaluate near-sourcing, hedging, and substitution strategies.

- Regulatory and standards-driven product re-specification. ISO 6518-1:2025 introduces updated requirements for ignition systems, clarifying expectations for single-ended and other coil types in road vehicles. Simultaneously, tightening emission norms demand ignition-system performance improvements (studies point to potential emissions reductions of up to 30% when ignition timing and stability are optimized). Product roadmaps need to embed compliance testing and certification as early-stage development milestones.

- Aftermarket resilience and OE integration. The market continues to bifurcate between OE-integrated solutions and a resilient aftermarket serving a large vehicle parc. The aftermarket remains attractive for margin and volume capture if players maintain VIO coverage and OE-equivalent testing regimes. For OEM suppliers, closer electrical-system integration (for precise spark timing and engine-control interfaces) is a differentiator.

- Supply-chain policy and localization pressures. With copper and other inputs under regulatory scrutiny, many buyers are evaluating supply-chain localization to avoid tariff exposure and logistical disruptions. 2026 sourcing strategies must balance cost, lead-time, and geopolitical risk—particularly for components with copper windings and iron cores.

Competitive landscape — what the players signal for 2026

The ignition coil field is populated by global OEM suppliers, specialized aftermarket brands, and vertically integrated systems providers. Market concentration is meaningful: the top firms collectively control a substantial share of industry value. The competitive dynamics emphasize engineering depth, quality certification, and supply reliability over pure price competition.

- Denso Corporation (Japan) — Denso’s emphasis on high-precision ignition coils for OEMs positions it to capture platform-level integration opportunities. Expect Denso to lean on combustion-efficiency claims and emission-compliance credentials when negotiating platform content with global automakers.

- Niterra / NGK (Niterra North America, Inc.) (United States) — A prominent aftermarket player with broad vehicle-in-operation (VIO) coverage and robust bench testing. Niterra’s strength is distribution breadth and OE-spec replication, making it a go-to partner for independent channels and warranty-centric buyers.

- Robert Bosch GmbH (Germany) — Bosch integrates ignition coils into broader vehicle electrical and powertrain systems. Their value proposition centers on system-level tuning for precise spark timing and fuel efficiency, an advantage for platforms requiring tightly coupled engine-electronics functionality.

- BorgWarner Inc. (United States) — Known for diesel cold-start coils and heavy-duty applications, BorgWarner captures segment-specific technical niches. Their capabilities are strategic for commercial-vehicle OEMs and fleet customers focused on reliability and emission control.

- Diamond Electric, Hitachi, Taiwan Ignition, Walker, Wells, Standard Motor Products, Nissens, SMP Corporation — This collection ranges from OEM-focused suppliers to aftermarket specialists. Several firms emphasize IATF 16949 and ISO certifications, aligning manufacturing and quality processes with global automaker expectations.

Recent corporate activity underscores competitive signaling. Notably, Nissens Automotive hosted a major product-focused event in May 2026 showcasing a new ignition coil range and opened its manufacturing capability to media scrutiny; earlier, in December 2025, Nissens partnered with Standard Motor Products to expand aftermarket system-critical content. Such moves highlight two trends: aftermarket consolidation/partnerships and marketing investments to rebuild trust around new product introductions.

Strategic plays for 2026 — what to prioritize now

We recommend executives concentrate on five practical workstreams in 2026 to convert market signals into defensible advantage.

- Material-risk mitigation program. Implement a cross-functional initiative (procurement, engineering, treasury) to quantify copper exposure, establish multi-sourcing lanes, evaluate form-factor redesigns that reduce copper use without performance loss, and consider strategic inventory policies for critical inputs.

- Standards-first product roadmaps. Integrate ISO 6518-1:2025 and emissions-driven performance targets into product requirements documents (PRDs). Early-stage test protocols and a documented certification timeline will reduce time-to-market risk and avoid costly redesigns.

- Aftermarket / OE channel playbooks. For suppliers: sharpen the dual strategy of OE platform wins and aftermarket coverage. Aftermarket participants should accelerate VIO mapping, warranty-backed testing, and distributor partner incentives to protect share. OEM-facing suppliers must demonstrate system-level integration and reduced ECU calibration effort.

- Localized capability and tariff-aware footprinting. Use scenario planning around tariff regimes and localized content rules to optimize plant placement and supplier contracts. For many firms, partial localization of copper winding operations or final assembly can yield tariff avoidance and shorter lead times.

- M&A and partnership scouting. Identify small-to-mid-cap targets that offer complementary metallurgy, coil assembly automation, or aftermarket distribution. Partnerships—such as the Nissens/Standard Motor Products tie-up—can accelerate market-entry and broaden system coverage with lower capital intensity than greenfield investments.

The practical utility of the full PW Consulting Ignition Coil Market report

This preview has outlined the big-picture drivers and recommended 2026 priorities. The full report converts those insights into operational outputs that decision-makers can act on immediately. Key deliverables include:

- Scenario-modeled demand and supply curves across 2026–2032, with sensitivity to copper price, tariff scenarios, and accelerated electrification uptake.

- Supplier scorecards including quality certifications, geographic footprint, product portfolios, and manufacturing risk indices.

- A comprehensive go-to-market playbook for OEM suppliers and aftermarket entrants (pricing levers, channel incentives, test- and certification roadmaps).

- Pipeline of acquisition targets, with high-level transaction rationale, valuation bandwidths, and integration risk flags.

- Detailed supply-chain maps and a recommended seven-step procurement mitigation plan for critical-material exposure.

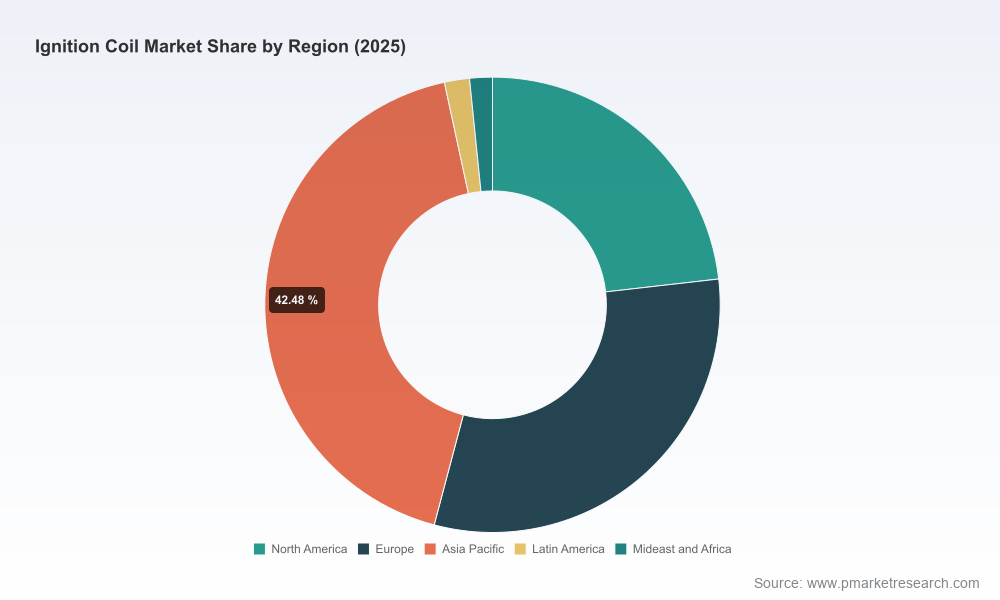

Note: in keeping with our “trailer” approach, this executive preview intentionally omits granular segmentation tables (regional and application-level splits) and precise company revenue shares. The full dataset and proprietary segmentation are available in the complete report and interactive dashboards.

How to use these insights in 90 days

Leaders who convert insight into early action tend to capture outsized advantage. PW Consulting recommends a three-month sprint plan for 2026:

- Week 1–4: Executive briefing plus one-day materials-risk war room to quantify immediate exposure and prioritize suppliers for dual-sourcing.

- Week 5–8: Standards alignment — update PRDs, set certification timelines, and commission bench testing for ISO 6518-1:2025 compliance.

- Week 9–12: Channel and M&A scouting — evaluate aftermarket partnerships and shortlist acquisition targets; prepare pilot localization schemes where tariffs materially affect landed cost.

These actions preserve optionality while embedding resilience into product and supply strategies—precisely the posture the 2026 competitive environment will reward.

Conclusion — why this matters for 2026

The ignition coil market in 2026 is not a binary bet on growth or decline; it is a nuanced arena where material sourcing, regulatory compliance, and system integration determine winners and laggards. With a steady mid-single-digit growth path and concentrated supplier power, companies that proactively address copper exposure, embed new standards into product development, and execute focused channel strategies will sustain margin and capture incremental content per vehicle.

PW Consulting’s full Ignition Coil Market report provides the proprietary segmentation, supplier-level analysis, and executable playbooks needed to make confident 2026 capital and commercial decisions. For access to the detailed datasets and interactive strategic tools, please consult the complete study on our website or contact your PW Consulting industry lead.

For detailed analysis of this topic, please visit the official page:Ignition Coil Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com