Computer Aided Detection (CAD) Market: Insights, Key Players, and Growth Analysis

Other |

2026-02-24 06:20:28

As organizations rush to decarbonize buildings, optimize ventilation for health, and enable smarter industrial controls, advanced CO2 sensing has moved from a niche technical requirement to a strategic lever across multiple industries. PW Consulting’s Advanced CO2 Sensors Market study (base year 2025, historical 2020–2025, forecast 2026–2032) synthesizes years of primary research, vendor interviews, and bottom-up market modeling to quantify this shift. The global market, measured in Million USD, rose sharply through the early 2020s and enters a new growth phase in our forecast window at a compound annual growth rate (CAGR) of 7.1% (2026–2032). This preview highlights why the report is essential for executives planning product roadmaps, channel strategies, M&A, and regulatory compliance programs in 2026 — while intentionally withholding detailed segment-level figures to direct you to the full analysis for transaction-grade intelligence.

Advanced CO2 Sensors Market

Regulation is accelerating adoption: Building codes and energy performance directives are increasingly prescriptive about indoor air quality (IAQ) and demand-controlled ventilation (DCV). Recent addenda to internationally recognized standards have elevated precision CO2 measurement from a best practice to a compliance requirement for many commercial and institutional projects.

Advanced CO2 Sensors Market

Technology is reaching industrial scale: Miniaturization, low-power NDIR and photoacoustic sensing, and integrated environmental sensing stacks make CO2 modules viable in cost-sensitive, battery-powered IoT products as well as mission-critical industrial and data-center systems.

Advanced CO2 Sensors Market

Economics favor retrofit and greenfield investments: Owners can now meet energy and emissions targets while aligning occupant-health goals, creating a unique value proposition for advanced CO2 sensing in building automation and HVAC retrofit markets.

Our topline modeling shows the advanced CO2 sensors market expanding from mid-single hundreds of Million USD in the early 2020s to substantially higher levels by the end of the forecast window, reflecting steady adoption across building automation, healthcare, industrial control, and IoT-enabled consumer segments. The 2026–2032 CAGR of 7.1% encapsulates both unit-price erosion in commodity modules and premiumization as higher-accuracy sensor technologies and system-level integrations command price premiums in regulated environments.

Standards and codes: Recent amendments to demand-controlled ventilation standards and the EU’s tightening of building energy performance criteria are the near-term accelerants. Products that demonstrate compliance with these standards unlock large procurement pipelines in commercial construction and civic infrastructure.

Sensor performance innovation: Photoacoustic NDIR and optimized solid-state NDIR platforms are delivering accuracy and low power that were previously mutually exclusive. These technical advances expand addressable use cases into battery-operated sensors and dense IoT deployments for continuous IAQ monitoring.

System integration and software: Value is shifting from standalone sensors to sensor-plus-software offerings that provide analytics, calibration drift compensation, and lifecycle management — an important margin and differentiation channel for both component suppliers and solution integrators.

Supply chain and manufacturing scale: Several vendors are transitioning to SMD-compatible packages and smaller optical stacks, enabling higher-volume manufacturing and lower unit costs while supporting automated assembly into HVAC controllers and IoT modules.

The market displays a moderately concentrated structure: the top three players account for a meaningful share of revenue, and the top five control a clear majority of the market by our estimates. That concentration creates both stability and strategic inflection points for challengers.

Senseair (Sweden) — Focus: ultra-compact NDIR for DCV and smart buildings. Recent launches of SMD-compatible, ultra-compact modules position the company to capture retrofit and OEM windows where size and standards compliance are decisive buying criteria.

Sensirion AG (Switzerland) — Focus: high-accuracy photoacoustic NDIR. Sensirion’s rollouts of drop-in, high-accuracy modules address the compliance-driven segment (standards-grade accuracy) and are attractive for device makers seeking simple upgrades from lower-accuracy sensors.

Gas Sensing Solutions (UK) — Focus: ultra-low-power solid-state NDIR for IoT. The firm’s power-optimized platforms are well-suited for distributed sensing topologies where battery life and form factor dictate deployment feasibility.

Vaisala, Amphenol Advanced Sensors, Siemens, Honeywell — These incumbents compete across precision applications, building systems integration, and industrial segments. They hold strategic advantages in channel access, brand recognition, and integrated system sales.

Recent product developments illustrate how incumbent and niche players are pursuing distinct routes to growth: miniaturization for OEMs, photoacoustic accuracy for standards-driven buyers, and low-power designs for large-scale IoT rollout. For buyers and investors, this divergence signals differentiated risk and reward profiles across subsegments — the full report maps these to revenue and margin outcomes under multiple scenarios.

Regulation is no longer an abstract tailwind: amendments to demand-controlled ventilation standards and evolving building performance directives are creating hard procurement triggers. Devices compliant with these standards gain immediate market access in many public and private procurement frameworks. Conversely, non-compliant modules face elimination from specification lists — increasing certification timelines and validation costs for manufacturers who do not prioritize compliance early in development.

Implication for product teams: Prioritize early alignment with applicable standards and third-party validation. Compliance is a value driver, not merely a checkbox.

Implication for procurement: Include verification of calibration stability and long-term drift performance as core selection criteria to protect against lifecycle surprises.

Companies that treat 2026 as a strategic inflection point should align investments across five pillars:

Product differentiation: Map sensing technologies (e.g., photoacoustic NDIR, solid-state NDIR) to targeted value propositions — compliance, low power, or cost-leadership — rather than pursuing one-size-fits-all designs.

Integration and services: Bundle sensors with cloud analytics, calibration services, and firmware lifecycle management to create recurring revenue streams and lock-ins with building operators and industrial customers.

Channel strategy: For component vendors, invest in reference designs and co-marketing with HVAC OEMs and system integrators. For system providers, secure long-term supply agreements to mitigate component sourcing risk as demand scales.

M&A and partnerships: Look for bolt-on acquisitions that fill gaps in calibration, software, or regional distribution. Strategic partnerships with calibration labs and standards bodies can accelerate certification and market entry.

Manufacturing resilience: Adopt SMD-ready packaging and diversify manufacturing footprints to reduce lead-time risk and capture OEM opportunities that demand automated assembly compatibility.

The full Advanced CO2 Sensors Market report is structured to support executive decision-making and transaction diligence. Key deliverables include:

Comprehensive market model (historical 2020–2025; forecast 2026–2032) with scenario sensitivity to regulatory adoption rates and technology cost curves.

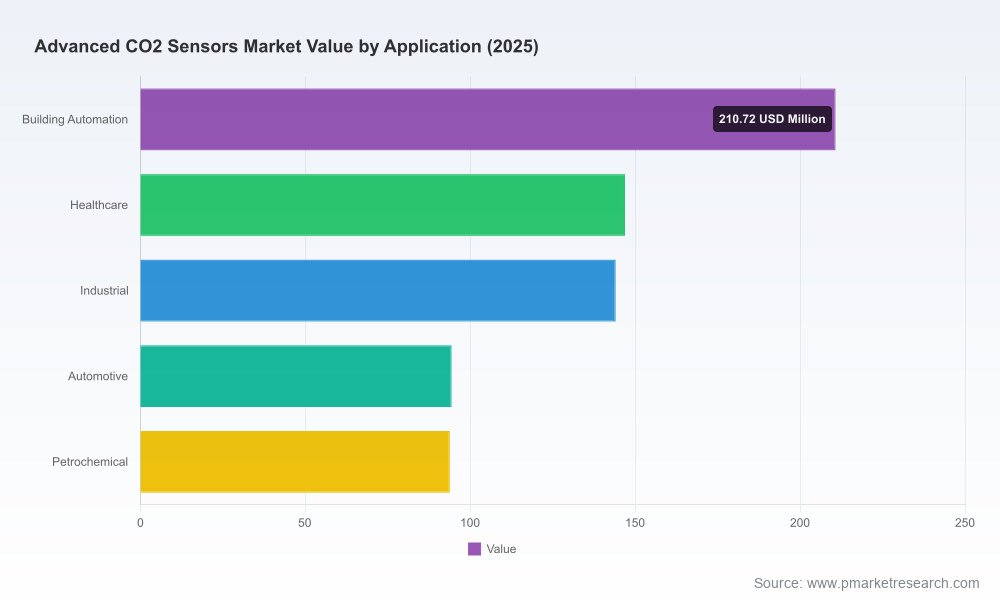

Segment-level demand drivers and adopter archetypes across building automation, healthcare, industrial, automotive, and petrochemical applications — mapped to procurement levers and specification gates.

Technology deep-dive: performance trade-offs, calibration strategies, power and form-factor roadmaps, and an R&D timeline for emerging sensing modalities.

Competitive intelligence: vendor profiles, product benchmarking, go-to-market strategies, and a supplier matrix that highlights fit-for-purpose partners for OEMs and integrators.

Commercial playbooks and financial impact templates: product roadmap prioritization, pricing levers, and a short list of M&A targets and partnership opportunities prioritized by strategic fit.

Regulatory & standards impact assessment: timelines, certification pathways, and a compliance risk register that operational teams can act on immediately.

CEOs & corporate strategy: Translate the 7.1% CAGR and market trajectories into portfolio allocations and inorganic growth targets; model downside scenarios if regulatory adoption lags.

Product leaders: Use the technology stack analysis to decide between pursuing miniaturization, accuracy, or ultra-low-power roadmaps — each with distinct margin implications.

Procurement & operations: Build sourcing strategies that account for SMD compatibility, calibration service dependencies, and long-term replacement cycles.

Investors & M&A teams: Assess target valuations with our revenue and margin forecasts under multiple market-penetration assumptions and standards-compliance scenarios.

This article is intentionally a strategic preview: it surfaces actionable implications, market dynamics, and vendor strategies to inform executive priorities in 2026. It does not reproduce the full segmentation tables, regional breakdowns, or granular revenue figures for subsegments — that level of detail is reserved for the full report, which contains the transaction-grade charts and downloadable modeling worksheets that many clients require for procurement and M&A diligence.

If you are defining a 2026 product roadmap: request the technology benchmarking appendix and the sensor-performance comparison matrix to align R&D milestones with certification timelines.

If you are evaluating strategic partnerships or targets: ask for the supplier fit matrix and regional channel readiness assessment to expedite diligence.

If you are a policy or compliance leader: obtain the regulatory impact scenarios to quantify the procurement and retrofit volumes that will likely flow from code updates.

Advanced CO2 sensing has moved from a specialized measurement task to a strategic enabler across energy, health, and industrial efficiency agendas. With sustained, standards-driven demand and meaningful technology differentiation, 2026 is a pivotal year for aligning product, channel, and regulatory strategies. PW Consulting’s full Advanced CO2 Sensors Market report provides the granular data, scenario modeling, and commercial playbooks needed to convert this macro momentum into defensible business outcomes. Contact PW Consulting to access the full dataset, vendor scorecards, and our bespoke advisory services that operationalize these insights.

For detailed analysis of this topic, please visit the official page:Advanced CO2 Sensors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com