Grinding Wheels Market 2026: Strategic Preview for Decision-Makers

As companies prepare strategy and capital plans for 2026, the Grinding Wheels market presents a blend of structural growth, technological transition and regulatory tightening that will determine winners and losers over the next investment cycle. PW Consulting’s latest market study — grounded in a 2020–2025 historical baseline and a 2026–2032 forecast horizon — shows a steady medium-term expansion (compound annual growth of 4.1%) and a market trajectory that rewards targeted product and supply-chain strategies rather than broad-brush volume plays.

Grinding Wheels Market

Market snapshot: scale, trajectory and structure

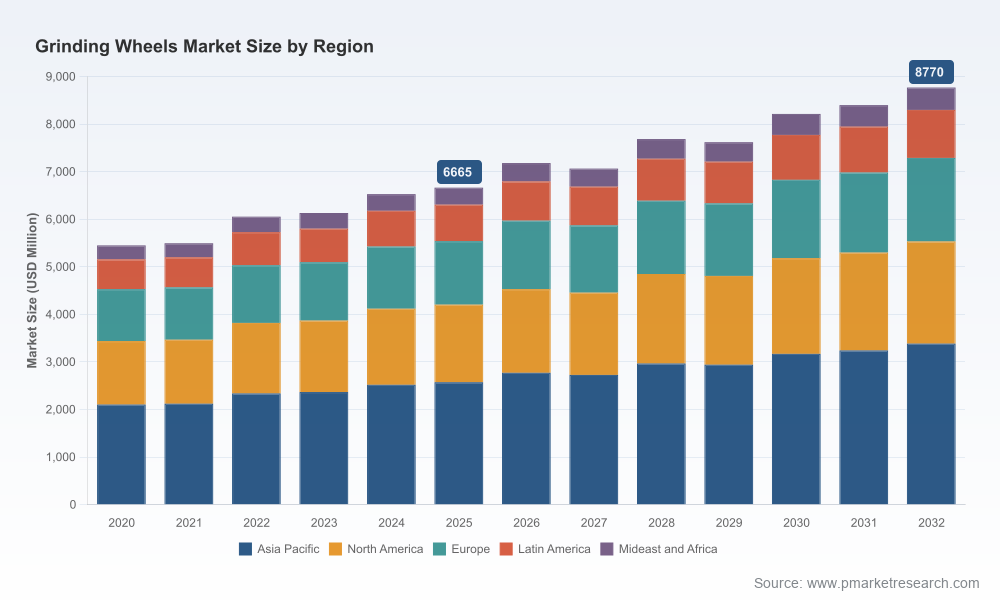

The market’s total revenue base has grown from an estimated USD 5,450 Million in 2020 to USD 6,665 Million in the report’s base year (2025), with the first forecast year (2026) beginning around USD 7,182 Million and a modeled path reaching approximately USD 8,770 Million by 2032. That headline growth masks short-cycle oscillations tied to capital goods demand, raw-material price cycles and cyclical end-markets such as automotive and steel, which create both tactical opportunities and timing risks for producers, distributors and OEMs.

Grinding Wheels Market

Concentration metrics indicate a moderately fragmented supplier landscape: the three-largest players account for under one-third of market revenue, while the five-largest capture roughly one-third. For strategic planners, that combination of scale and fragmentation favors disciplined consolidation and specialization moves — there is room to build scale advantages through focused M&A, value-added services, or regional supply-chain optimization.

Grinding Wheels Market

Why this matters for 2026 corporate decisions

- Capex and product-mix choices: With mid-single-digit CAGR and episodic demand swings, 2026 is a year for selective capacity investments. Players should prioritize investments that raise margin through product differentiation (superabrasives, precision vitrified bonds) rather than undirected volume expansion.

- R&D and application engineering: The next wave of value capture is technical: engineers want wheels that enable tighter tolerances, faster cycle times and longer life on advanced steels and hardened materials. Firms that pair abrasive chemistry with application-specific dressing and machine compatibility will command a premium.

- Supply-chain resilience: Raw-material dynamics — notably the continued dominance of aluminum oxide among abrasive grains — and regulatory controls on safety and traceability mean procurement and compliance must be integrated into strategic planning. Expect procurement-led margin volatility unless material sourcing and hedging are tightened in 2026.

- Regulatory compliance as a cost and differentiation factor: Revised standards and machine classifications require validated marking, burst-guard calculations and explicit operating parameters. Compliance is non-negotiable; companies that embed traceability and safety documentation into product offerings can convert compliance costs into differentiated service features.

Report deliverables: practical tools inside

PWC’s Grinding Wheels Market report is designed for executives and functional leaders making 2026 decisions. The study goes beyond high-level forecasting and delivers actionable assets:

- Forward-looking demand model (2026–2032) with scenario variants keyed to macroeconomic elasticity and capital goods cycles.

- Risk-adjusted supply-chain heatmaps and raw-material exposure matrices, including sensitivity to abrasive-grain price moves and logistics bottlenecks.

- Regulatory compliance playbook that maps new and revised standards to required product and process changes, and estimates implementation timelines and capex.

- Commercial playbooks for OEM, distribution and aftermarket channels with pricing levers, margin waterfall templates and go-to-market segmentation strategies.

- Vendor benchmarking framework and scorecards for technology, service, geographic reach and channel coverage — set up for quick use in M&A screening or procurement re-sourcing.

- Hands-on case studies and technology deep dives (vitrified vs. resin bonds, CBN/diamond applications, precision-shaped grains) focused on improving cycle times, life and cost-per-part.

Note: the preview above intentionally omits the full set of regional and application-level data tables; those granular splits and downloadable models are available in the full report for subscribers.

Competitive landscape: core players and strategic postures

The market combines global incumbents with regional specialists. Leading industrial brands maintain broad portfolios spanning conventional abrasives to high-performance superabrasives; at the same time, regional players retain cost and proximity advantages that matter for heavy industrial end-users.

- Saint-Gobain Abrasives (Norton brand): A diversified portfolio that spans vitrified and resin-bonded wheels and CBN products aimed at automotive and aerospace. Strategic strength: global application engineering, strong OEM relationships and cross-selling into other abrasive segments.

- Norton Abrasives (US operations): Focus on conventional aluminum oxide and silicon carbide products plus superabrasives. Strategic posture: incremental innovation in grain and bond chemistry to protect volume in legacy applications while migrating customers to higher-value solutions.

- 3M Abrasives: Known for precision-shaped grain technologies (e.g., Cubitron II) and performance-oriented cut-off and depressed-center wheels. Strength lies in materials science and branded premium positioning that command margin on performance claims.

- Tyrolit Group: Emphasis on precision and superabrasive applications for automotive, aerospace and toolmaking. Strategic advantage: specialized product lines and deep machine-tool compatibility expertise.

- Klingspor: Broad abrasive and bonded-wheel product portfolio with strong presence in European industrial distribution channels.

- Camel Grinding Wheels & Carborundum Universal Limited: Regional champions with strong manufacturing footprints and distribution networks in key emerging and industrial markets; they are often the partners of choice for high-volume, locally-served accounts.

For 2026, the competitive playbook should be mixed: global players must defend premium segments and engineering leadership while regional players can exploit proximity and cost advantages. Strategic alliances — particularly around machine compatibility and predictive dressing — will be a force multiplier.

Near-term dynamics shaping operational choices

- Raw-materials: Aluminum oxide continues to represent the largest single abrasive grain group, underpinning commodity wheel production. Price and availability trends for alumina and superabrasive feedstocks should be modeled directly into procurement and pricing strategies.

- Standards and safety: Recent updates in national and international standards tighten requirements for marking, maximum operating speeds, burst-guard verification and machine risk classification. Buyers increasingly demand documented traceability and shelf-life controls — requirements that affect packaging, inventory management and warranty terms.

- Technology and product innovation: Trade shows in 2026 revealed intensified activity around CBN/diamond applications, electroplated and dressable wheels, and very-large-diameter grinding solutions. These advances favor suppliers who invest in application labs and machine-to-wheel co-development.

Strategic recommendations for 2026 planning

- Prioritize engineering-led segments: Allocate R&D and application-support spend to superabrasive and precision vitrified offerings where margin expansion is realistic.

- Embed compliance in product lifecycle: Convert regulatory obligations into customer-facing benefits (traceability, safety-certification bundles, documented burst-testing) to support premium pricing.

- De-risk supply chains: Hedge critical feedstock exposure, develop dual-sourcing strategies for key grains, and relocate strategic inventory closer to high-value customers.

- Pursue bolt-on M&A selectively: Look for regional manufacturers with distribution strengths or niche superabrasive capabilities that complement core portfolios and accelerate customer access.

- Commercialize services: Offer dressed-wheel lifecycle management, dressing optimization services and predictive replacement contracts — service revenues stabilize cash flow in a cyclical market.

What you’ll find in the full PW Consulting deliverable

The full report contains the complete set of regional and application splits, downloadable forecasting models, price index histories, and a vendor-by-vendor scorecard with capability matrices and contact intelligence. It also includes our consultants’ scenario playbooks for inflation-driven cost shocks, EV-driven drivetrain shifts and rapid regulatory adoption — all modelled to illustrate P&L and balance-sheet impacts under alternative planning assumptions.

For teams making 2026 investment, procurement and M&A decisions, this is an operational toolbox: not just projection tables but executable plans, timelines and playbooks designed to shorten decision cycles and reduce execution risk.

Next steps

If your 2026 plan needs to reconcile constrained capex with higher product complexity and tighter safety obligations, the full PW Consulting Grinding Wheels Market report is the practical intelligence kit to accelerate decision-making. Access to the granular datasets, vendor scorecards and scenario models is available through our research portal and advisory desk.

Contact PW Consulting to schedule a briefing where we’ll walk your leadership team through the model, stress-test your 2026 scenarios and identify the 90-day actions that unlock the highest ROI in the current market environment.

For detailed analysis of this topic, please visit the official page:Grinding Wheels Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com