Iron Deficiency Injectable Market Dynamics: Key Drivers and Restraints

Other |

2026-06-04 03:51:17

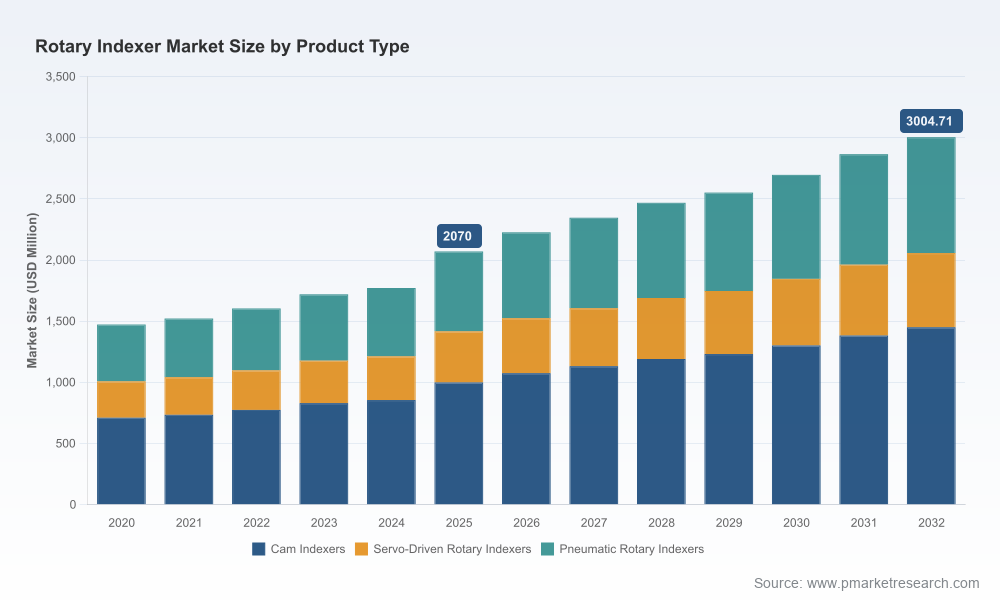

As manufacturers accelerate automation investments, rotary indexers are transitioning from commoditized motion components to strategic system elements that determine cycle time, uptime, and line flexibility. PW Consulting’s Rotary Indexer Market study (base year 2025) synthesizes seven years of historical performance and a seven‑year forecast horizon to 2032. The market has grown materially from the early 2020s and, under our base forecast, advances from roughly USD 2.07 billion in 2025 to just over USD 3.00 billion by 2032 — a trajectory that reflects a mid-single‑digit CAGR (report CAGR: 5.49%).

Rotary Indexer Market

This preview highlights why that topline matters for capital planning, supplier strategy, and product development choices in 2026, while deliberately reserving our granular segmentation and vendor-scoring data for the full report. The goal: convince executive teams that rotary indexer strategy should sit squarely on the 2026 priority list, and show how PW Consulting’s report converts market signals into executable options.

Rotary Indexer Market

Investment velocity meets digitization expectations. Production lines installed in 2023–25 are reaching their first major rework windows in 2026. Decisions on whether to retrofit with servo-driven or maintain cam/pneumatic architectures will determine throughput and OEE for the next decade.

Rotary Indexer Market

Supply‑chain normalization is partial and fragile. Inventory policies, dual‑sourcing clauses, and buffer strategies implemented now will materially affect delivery lead times and time‑to‑market in fast‑growing end markets (notably electronics and food & beverage segments).

Regulatory and certification timelines compress procurement cycles. Compliance with OSHA (29 CFR 1910 Subpart O), the EU Machinery Directive (2006/42/EC) and key regional machine‑safety standards is increasingly embedded into vendor selection — creating a premium for compliant and well‑documented indexer systems.

The rotary indexer market exhibits a clear structural growth path: steady expansion through 2020–2025 followed by continued growth across the 2026–2032 forecast window at an implied mid‑single‑digit CAGR (5.49%). That expansion is underpinned by a few observable dynamics:

End‑user sophistication. OEMs and contract manufacturers are prioritizing indexers that integrate tightly with PLCs, motion controllers, and plant‑level MES for deterministic positioning and traceability.

Technology migration. There is an accelerated shift toward programmable and servo‑enabled indexers in applications demanding high precision and dynamic changeover, while mechanical cam and pneumatic solutions remain relevant where low cost and simplicity dominate.

Service and lifecycle revenue. Vendors are monetizing after‑sales through retrofit kits, spare parts agreements, and predictive maintenance services — expanding the lifetime value of an installed base.

Adopt a tiered procurement strategy: prioritize modular, digitally instrumented indexers for high‑value, high‑variability lines; retain proven mechanical solutions for stable, high‑volume operations. Our full report includes a decision matrix that maps application profiles to procurement levers.

Design for retrofitability: mandate mechanical and electrical interfaces now — motor mounts, encoder interfaces, and control protocols — to reduce future conversion costs. We model retrofit ROI thresholds across multiple cycle‑time scenarios.

Embed regulatory checks into vendor scorecards: ensure vendors furnish CE/UL declarations and regional safety certificates (e.g., GB/T 5226.1, IS/ISO 12100). The absence of proper certification is a contract‑level risk.

Price the total cost of automation (TCA), not just the unit price. Our TCO templates quantify upfront cost, integration labor, downtime risk, and spare parts provisioning over a 7–10 year horizon.

The market remains moderately fragmented; leading global suppliers capture a meaningful but not overwhelming share of demand, leaving room for regional specialists and systems integrators. Below are the strategic postures of the primary providers profiled in the study — the full vendor scorecards and capability matrices are included in the paid report.

Motion Index Drives (Troy, MI, USA) — Strength: cam‑driven tables and high‑cycle mechanical solutions tailored for aerospace and packaging. Strategic fit for high‑durability, high‑throughput lines where proven mechanical repeatability is prioritized.

Nexen Group (Providence, RI, USA) — Strength: servo and ring‑drive technology with high torque and moment capacity. Ideal for precision positioning and heavy‑duty indexing in automated assembly contexts.

WEISS GmbH (Buchen, Germany) — Strength: programmable indexers and digital controls; strong systems integration pedigree for automotive and medical assembly. Recent activity includes trade‑show product showcases and a strategic technology partnership with a major semiconductor automation player — signals of a deliberate push into high‑precision markets.

Destaco (Wixom, MI, USA) — Strength: combined mechanical and servo offerings with a strong presence in assembly and packaging automation OEMs.

Sanko Automation (China) — Strength: competitive hollow and fixed‑station solutions with cost advantages for regional OEMs and integrators.

Centricity Automation (USA) — Strength: PLC‑integrated, high‑precision servo indexers suited to retrofit and standalone applications.

Taktomat GmbH (Germany) — Strength: high‑speed fixed and flexible division indexers for continuous production lines.

TallMan Robotics (China) — Strength: engineered motion solutions and bespoke cam drive systems for specialized applications.

Festo (Germany) — Strength: pneumatic DHTG series and well‑established automation ecosystem for partially automated and buffer systems.

The competitive landscape favors vendors that can demonstrate end‑to‑end capability: reliable mechanical design, digital controls, and regional service networks. PW Consulting’s full competitive module provides vendor heat maps, product‑portfolio clustering, and M&A watchlists to guide sourcing and partnership decisions.

Regulatory compliance is not optional. Conformity with the EU Machinery Directive 2006/42/EC (CE marking) and relevant OSHA standards in North America is a gating criterion for acceptance into many OEM supplier panels.

Regional standards (e.g., China’s GB/T 5226.1 and India’s IS/ISO 12100) require local documentation and sometimes recertification after modification — plan for lead times and testing costs accordingly.

Supply‑chain fragility remains a practical constraint. Geopolitical tensions and trade restrictions continue to create sporadic lead‑time spikes for precision components (bearings, gears, encoders). Our scenario stress tests quantify the inventory and contractual buffers required to maintain line continuity under three disruption scenarios.

Electrical safety and interoperability: UL certification in North America and clear control‑interface standards reduce integration friction for automation integrators.

PW Consulting’s full Rotary Indexer Market study is built as a working toolkit for decision‑makers. Highlights include:

Consolidated market model with historical series (2020–2025) and a detailed 2026–2032 forecast at market, product‑type and end‑use layers (note: detailed numeric splits are available in the paid report).

Vendor scorecards and product‑fit matrices—comparing mechanical, pneumatic, and servo alternatives across precision, uptime, and TCO dimensions.

Procurement playbook—supplier selection criteria, contracting templates, and preferred warranty/service terms tailored to indexer types.

Retrofit and greenfield decision frameworks, including ROI calculators and break‑even models sensitive to labor rates, downtime cost, and upgrade cadence.

Supply‑chain stress scenarios and recommended mitigation: dual sourcing thresholds, safety stock models, and logistics contingency plans.

Compliance checklist and region‑specific certification roadmaps to accelerate approvals and reduce audit friction.

Go‑to‑market playbooks for vendors: product positioning, channel strategies, and service packaging models we found effective in 2024–25 commercial pilots.

Capital planners: re‑evaluate spend bands using the TCO templates — capital savings on low‑cost indexers can be easily eroded by integration labor and unplanned downtime.

Product teams: prioritize modularity and digital interfaces. Products that simplify retrofitability capture a disproportionate share of late‑cycle OEM order flow.

Supply‑chain leads: implement staged dual‑sourcing and critical component pools now to avoid the lead‑time penalty on high‑priority programs.

Commercial teams: use our vendor heat maps and partner scorecards to identify alliance opportunities and carve out regional service footprints.

The rotary indexer market is at an inflection where engineering choices translate directly into operational agility and commercial resilience. With a market advancing from the low‑billion range in 2025 toward a USD 3.00+ billion outlook by 2032 under a ~5.5% CAGR, 2026 is the practical inflection point for re‑architecting production strategy.

PW Consulting’s full report offers the granular segmentation, vendor benchmarking, and executable tools you need to convert these macro trends into defensible 2026 plans. This preview intentionally omits the detailed numerical splits and vendor rankings so that procurement, engineering and strategy leaders who require the full decisioning toolkit can access the complete intelligence on our report page.

To obtain the complete dataset, interactive models, and vendor scorecards referenced above, please consult the PW Consulting Rotary Indexer Market report page or contact our advisory team for a tailored briefing and scenario walk‑through.

For detailed analysis of this topic, please visit the official page:Rotary Indexer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com