The Rise of India’s Gas Turbine Market as a Power Generation Leader

Other |

2026-05-11 07:27:12

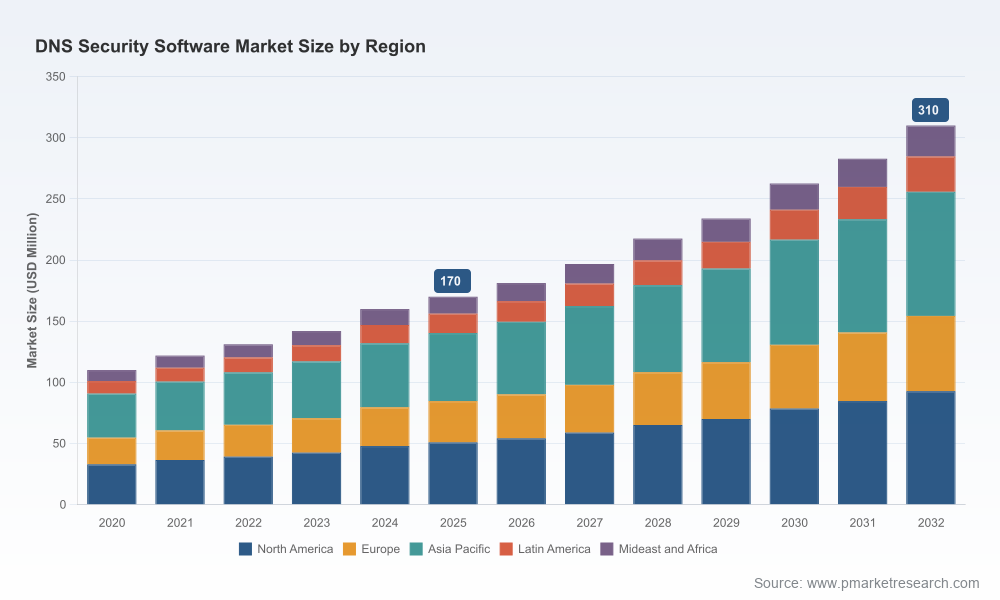

As enterprises finalize cyber budgets and vendor roadmaps for 2026, DNS security has moved from a niche network hygiene topic to a strategic control plane for resilience, visibility and threat mitigation. Our PW Consulting market study—summarized here as a preview—captures the market’s trajectory and the actionable choices that will determine enterprise success in the next procurement cycle. At the macro level, the DNS security software market has expanded markedly over the past half-decade and, driven by cloud adoption, AI-enabled detection, and regulatory mandates, is forecast to sustain robust growth at a compound annual growth rate (CAGR) of 8.9% through the 2026–2032 horizon, with the overall market roughly doubling from the early-2020s into the early-2030s.

DNS Security Software Market

DNS is the implicit routing layer for modern enterprises: adversaries increasingly weaponize DNS for data exfiltration, command-and-control, and as a staging vector for supply-chain attacks. Traditional perimeter defenses are insufficient when DNS queries and resolvers are distributed across cloud, branches and remote endpoints.

DNS Security Software Market

Cloud and hybrid architectures have shifted authoritative and recursive responsibilities outside classic network boundaries, forcing a rethink of security controls, outage tolerance and vendor SLAs. DNS failures or poisoning events now translate directly into business downtime and reputational risk.

DNS Security Software Market

Regulatory and procurement dynamics are reshaping minimum requirements: recent U.S. executive guidance makes encrypted DNS support a procurement criterion for federal resolvers, while sectoral guidance (notably CISA) is steering investment toward AI-enabled DNS defenses for critical infrastructure. National strategies in markets such as Japan further accelerate adoption of machine-assisted threat detection at the DNS layer.

Several interlocking forces are defining buyer behavior and vendor strategy. First, cloud-first digital transformations and distributed work models are increasing demand for cloud-native DNS protections that can instrument and enforce policy across a hybrid estate. Second, attackers’ use of low-and-slow DNS channels has pushed security teams toward solutions with behavioural analytics and AI to detect subtle anomalies. Third, resilience requirements—particularly DDoS mitigation for authoritative services—are elevating expectations for carrier-grade DNS delivery and multi-provider redundancy. Finally, market structure remains moderately fragmented, creating both opportunity for specialized innovation and for strategic consolidation by platform players looking to bundle DNS controls with broader secure access and edge security stacks.

Cisco — Offers a cloud-delivered DNS-layer security solution that integrates threat intelligence at scale. Its strength is a broad enterprise footprint and integration with existing secure access and EDR investments, appealing to buyers seeking consolidated security platforms.

Infoblox — Focuses on protective DNS and threat defense for infrastructure resilience and governance. It is often chosen by organizations prioritizing DNS infrastructure hardening and centralized operational control.

Cloudflare — Competes through a high-performance resolver and DNS firewall services that combine DDoS mitigation with global edge delivery. Cloudflare’s proposition is attractive to organizations seeking a performant, internet-scale control plane.

Akamai — Has extended its delivery portfolio with offerings that provide DDoS-resilient DNS and, recently, introduced DNS posture management to give multicloud visibility and remediation without agents—addressing a critical operational gap for large, distributed estates.

F5 — Leverages its application and traffic management heritage to offer DNS services that blend security with advanced load balancing—valuable in hybrid data-center plus cloud environments where traffic steering and resilience are priorities.

Verisign and Neustar — Both provide authoritative and managed DNS services with strong DDoS protection and enterprise-grade SLAs, positioning themselves as strategic partners for critical infrastructure and high-availability use cases.

Taken together, vendor activity highlights two strategic plays: one is platform consolidation (bundling DNS with secure access and threat intelligence); the other is specialized capability leadership (edge-scale resolvers, posture management, or authoritative DNS resilience). Recent product launches and partnerships confirm both vectors: for example, a leading edge provider introduced agentless DNS posture management in mid‑2025, and regional alliances have formed to accelerate security application deployments across targeted geographies.

This study is designed for practitioners who need immediate, implementable guidance rather than academic descriptions. The deliverables—crafted for CISOs, procurement leads, and architecture teams—include:

Proprietary market sizing model and methodology that reconciles license, service and managed offerings across a 2020–2032 time series.

Vendor scorecards and a decision matrix mapping technical capabilities, operational fit, and contractual risk

Use-case playbooks (resolver protection, authoritative DNS resilience, DNS threat hunting, and cloud-native policy enforcement) with deployment patterns and implementation checkpoints

Migration and integration guides for common architectures (on-premises → cloud, hybrid multi‑DNS, and resolver consolidation), including testing protocols and rollback criteria

Procurement artifacts: RFP language templates, SLA clauses, incident response commitments, and compliance mapping aligned to recent regulatory expectations

Executive decision frameworks and ROI/TCO calculators to quantify business impact and prioritize spend across projects

Operational tools: attack surface inventory templates for DNS assets, threat-case catalogues, and runbooks for tabletop exercises

Treat DNS as an enterprise control plane: assign accountability to a cross-functional owner (security-architecture plus network-operations) and include DNS KPIs in board-level dashboards.

Prioritize encrypted DNS and resolver requirements in procurement: recent federal procurement criteria set a clear market floor—so buyers should bake encrypted DNS and protocol support into baseline vendor acceptance tests.

Invest in AI-enabled detection capabilities but validate transparency: CISA-oriented guidance is accelerating AI adoption; insist on explainability for ML models that will be used for blocking or automated remediation.

Design for multi-provider resilience: combine managed authoritative services with cloud-native resolver protections and on-prem fallbacks to avoid single‑provider failure modes.

Use posture management to close discovery blind spots: agentless posture approaches can rapidly inventory disparate DNS assets across multicloud estates and feed into prioritised remediation plans.

Apply a staged procurement approach: pilot selective use cases with narrow SLAs, measure operational overhead and false positive rates, then scale by use-case rather than by vendor feature checklists.

Align cyber-insurance and compliance teams early: DNS incidents intersect contractual uptime commitments and regulatory obligations—pre‑negotiated clauses and testing evidence will materially change underwriting discussions.

This preview is intended to surface the strategic questions and operational levers that should shape 2026 decisions. For procurement teams and CISOs preparing vendor shortlists or migration plans, the full PW Consulting study contains the quantitative segmentations, vendor-level benchmarking, and contract templates necessary to execute—alongside the full time-series market model and regional and vertical breakdowns that inform budget allocation and go-to-market timing.

If you are setting priorities for the coming fiscal year, start with a compact cross-functional workshop: validate current DNS estate visibility, stress-test recovery runbooks for authoritative failures, and run a small pilot to evaluate an AI-detection vendor’s false positive profile. Use the decision frameworks in our full report to convert pilot outcomes into a phased enterprise rollout plan.

DNS security is no longer a checklist item: it is an operational and strategic lever that affects resilience, compliance and competitive continuity. Our research shows a market accelerating on the twin engines of cloud migration and AI-enabled detection, expanding at a sustained CAGR through the next planning window. The PW Consulting report synthesizes market dynamics, vendor profiles and procurement-grade artifacts to reduce implementation risk and fast‑track measurable outcomes. For teams preparing capital allocations and vendor selections for 2026, the full study is the practical next step to turn strategic intent into operational momentum.

For detailed analysis of this topic, please visit the official page:DNS Security Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com