Optical Transceivers Market Outlook: Strategic Imperatives for 2026 — PW Consulting Preview

As hyperscale cloud providers, AI infrastructure builders and traditional telecom operators accelerate the shift to higher per-lane speeds and tighter electrical‑optical integration, the optical transceivers market is entering a phase of structurally higher growth and strategic repositioning. PW Consulting’s latest market study — with a 2025 base year and a 2026–2032 forecast horizon — projects a sustained compound annual growth rate (CAGR) of 13.5%, reflecting rapid adoption of 400G–1.6T class modules, early commercialization of co‑packaged optics, and ongoing upgrades across data center interconnect (DCI), carrier and enterprise segments.

Optical Transceivers Market

Market Snapshot: Macro Trajectory and What It Means for 2026 Planning

Our aggregate market model shows clear momentum: the global optical transceivers market expands from a 2025 base of USD 13,900 Million to a materially larger market by the end of the forecast window. Year‑on‑year growth in 2026 is driven by replacement cycles in hyperscale data centers, new AI/ML connectivity requirements, and increased coherent pluggable uptake in metro and long‑haul networks. For decision-makers planning investments in 2026, the headline implication is straightforward — demand will not only continue but will accelerate into higher‑speed, higher‑value product segments, creating both opportunities and margin pressure across the value chain.

Optical Transceivers Market

Strategic Value of This Research for 2026 Decisions

- Procurement and Capacity Planning: Procurement leaders can translate the CAGR and short‑term demand inflection into actionable capacity roadmaps. The study quantifies the timing and velocity of demand shifts so OEMs, contract manufacturers and CEMs can avoid costly under- or over‑capacity in 2026.

- R&D and Product Roadmapping: Engineering and product teams can prioritize investments between pluggable versus co‑packaged architectures, PAM4 vs. coherent solutions, and silicon photonics vs. hybrid integration. Our scenario analysis shows which technology paths are likely to deliver commercial payback within a 24–36 month window.

- M&A and Partnership Screening: The market’s concentration and the pace of technological consolidation inform buy vs. partner decisions. The study identifies value pools where bolt‑on acquisitions or JV structures are most likely to accelerate time‑to‑market and improve technology differentiation.

- Supply Chain Risk Management: With component concentration and geopolitical policy shifts altering supply reliability, procurement and strategy teams can use our stress‑tested forecasts to design dual‑sourcing strategies and near‑shoring scenarios for critical photonics components.

What the Report Contains — Practical, Actionable Modules

PW Consulting’s report was written with a practitioner audience in mind. It does not merely present numbers; it maps those numbers to commercial levers. Key deliverables include:

Optical Transceivers Market

- Market sizing and forward projections (2026–2032) with high‑granularity scenario runs tied to technology adoption curves and hyperscale deployment schedules.

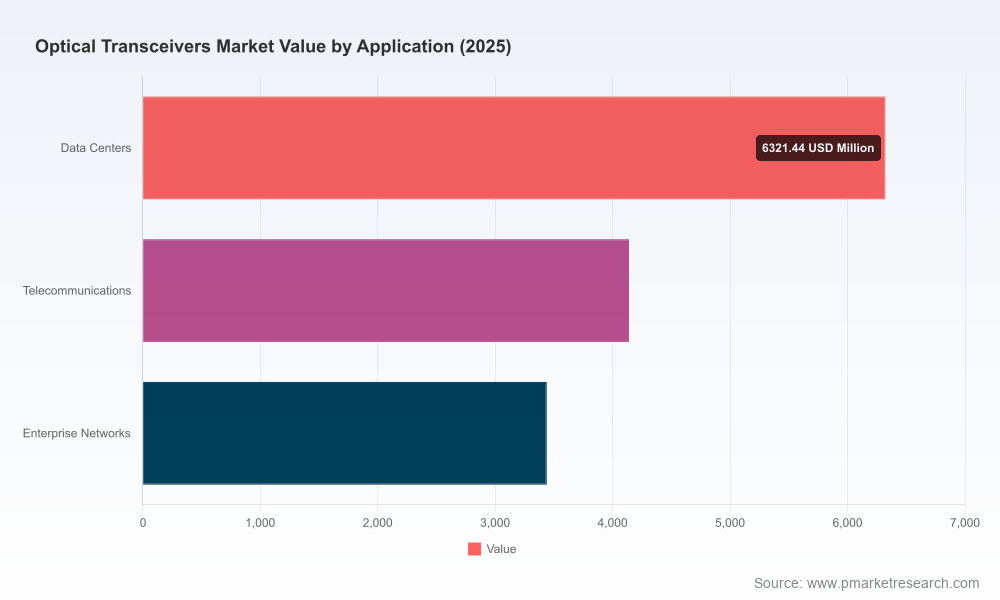

- Demand‑side segmentation by product family, application and region, with actionable demand triggers and timing indicators (note: detailed segment tables and raw model files are available in the full report).

- Cost‑to‑serve and margin sensitivity layers that model the impact of material costs, labor inflation and yield improvements on unit economics across transceiver classes.

- Risk matrices for supply chain disruptions, regulatory shocks and component scarcity mapped to contingency actions and procurement tactics.

- Commercial playbooks for vendors, OEMs and service providers: go‑to‑market approaches, pricing strategies and bundling techniques for 2026 market entry or expansion.

Competitive Landscape — Who’s Shaping the Next Phase?

The market is characterized by a mix of vertically integrated incumbents, photonics‑specialist challengers and regional manufacturers advancing scale. A near‑term implication for 2026 is that the leading vendors will increasingly compete on system‑level integration, manufacturing footprint and ecosystem partnerships rather than on isolated component pricing.

- Coherent and Silicon Photonics Leaders: Companies that pursue vertical integration of silicon photonics, VCSEL arrays and coherent engines — thereby controlling optics, drivers and sub‑assemblies — gain advantages in performance tuning and cost trajectory. Demonstrations of next‑generation 1.6T modules and advanced VCSELs underscore how integrated roadmaps shorten time‑to‑market for hyperscale customers.

- System and Switch Vendors: Network infrastructure vendors that broaden their pluggable portfolios and internal optics engineering (including recent acquisitions expanding optical teams) can own more of the value chain between switch ASICs and optical I/O — a strategic edge for large cloud customers demanding validated, multi‑vendor interoperability.

- CPO and Optical I/O Innovators: Suppliers investing in co‑packaged optics and optical I/O engines are positioning for a future where chip‑to‑chip optical links meaningfully displace copper at top‑of‑rack and inter‑switch tiers. Early shipments of high‑bandwidth CPO switches signal that 2026 will be a crucible year for adoption pilots and design‑win accumulation.

- Regional Manufacturers: Localized manufacturers are scaling production for pluggable and active optical cable segments, amplifying resilience for customers wanting supply‑chain diversity — a capability that will be prioritized more heavily in 2026 under geopolitical pressures.

Recent commercial moves — from first shipments of extremely high‑throughput CPO platforms to demonstrations of 1.6T optical modules and strategic acquisitions that expand optical engineering talent — confirm a market transitioning from proof‑of‑concept to commercial deployment. These developments are accelerating supplier differentiation on manufacturing scale, technology depth, and ecosystem access.

Industry Dynamics and External Noise to Monitor

Three non‑market forces will materially shape 2026 outcomes:

- Geopolitical and Regulatory Friction: Technology export controls and national industrial policies are already impacting sourcing decisions for lasers, photodetectors and advanced PICs. Firms with diversified supplier bases and localized manufacturing options will have an execution advantage in 2026.

- Cost Pressures in Advanced Nodes: Higher manufacturing costs and component sensitivity for 400G/800G modules keep unit economics tight. Yield and automation improvements are the most direct levers for margin recovery.

- Standards and Harmonized Regulation: Regional regulatory frameworks that streamline infrastructure approvals and spectrum planning can reduce deployment friction, particularly in Europe where digital‑sovereignty initiatives are incentivizing local supply chains.

Scenario Planning: Four Plausible Pathways into 2026

Our model evaluates four scenarios — Base, Accelerated AI Uptake, Trade Fragmentation, and Tech‑Open Collaboration — each producing different demand timing and supplier advantage maps. The strategic takeaway for 2026 is not a single “right” move but a set of contingent options:

- Base Scenario: Linear continuation of current upgrade cycles. Tactical emphasis: secure volume contracts and incremental manufacturing investments.

- AI Acceleration: Rapid hyperscale demand for 800G–1.6T transceivers. Tactical emphasis: prioritise silicon photonics and co‑packaged optical design wins; fast‑track validation and supply agreements.

- Trade Fragmentation: Increased localization driven by export controls. Tactical emphasis: redistribute production footprint, dual‑source critical components, and pursue strategic JV/outsourcing agreements.

- Tech‑Open Collaboration: Standardization and cooperative industry consortia lower integration barriers. Tactical emphasis: pursue interoperability certifications and platform partnerships to win large RFPs.

Recommended Actions for Executives Preparing for 2026

- Map demand scenarios to a 24‑month product cadence: prioritize which transceiver classes to accelerate and which to defer based on customer commitments and anticipated price elasticity.

- Invest selectively in manufacturing automation and yield analytics for higher‑speed modules to protect margins as unit cost pressure intensifies.

- Implement a geopolitical stress test across your supplier base and create a prioritized list of components for near‑shoring or dual sourcing.

- Pursue targeted M&A or partnership plays to acquire photonics IP, accelerate silicon photonics roadmaps, or secure co‑packaged optics design capabilities.

- Establish commercial pilots with hyperscalers and switch vendors to build reference designs — buyers prioritize proven interoperability in 2026 procurements.

Why PW Consulting’s Analysis Is a 2026 Decision Catalyst

Our report blends quantitative market sizing and scenario modeling with practitioner guidance — not just what the market will look like, but how to act. We reveal timing windows for capex, the likely winners by integration strategy, and the operational levers that shift unit economics. That combination of timing, technology and tactics is exactly what procurement chiefs, CTOs and strategy leads need to make informed 2026 commitments.

Next Steps — Where to Get the Full Intelligence

This preview intentionally highlights strategic implications while preserving the detailed segmentation matrices, company‑level forecasts and downloadable financial models for subscribers. For access to the full dataset — complete regional and application splits, vendor shares, and executable playbooks — please consult PW Consulting’s full Optical Transceivers Market report. The complete deliverable contains the underlying model and vendor scorecards you will need to operationalize a 2026 strategy.

For detailed analysis of this topic, please visit the official page:Optical Transceivers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com