Industrial Metal Casting Components Market Supporting Precision Manufacturing and Structural Applications

Other |

2026-02-11 10:46:58

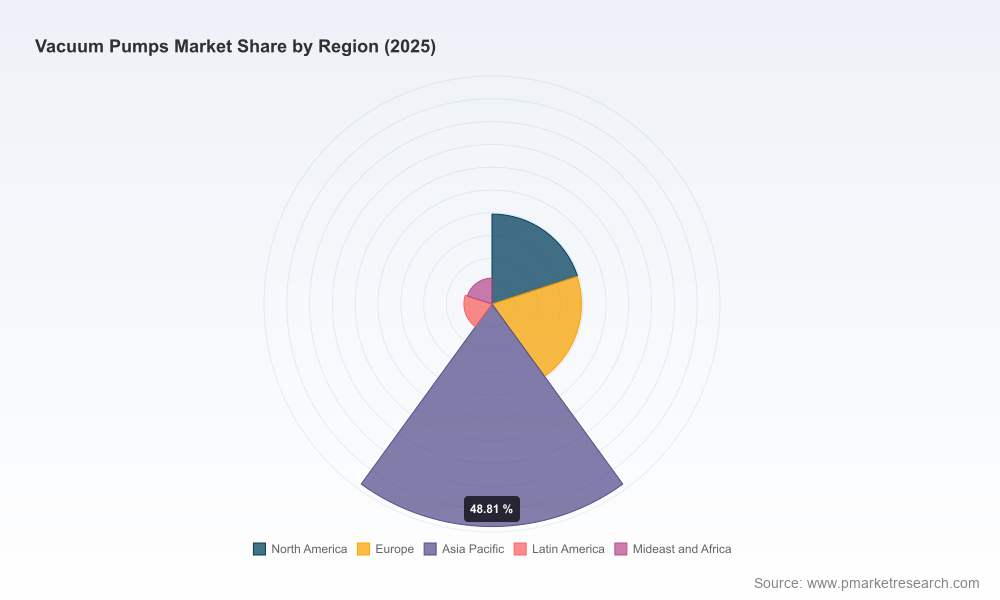

As PW Consulting’s lead industry analyst, I present a high-level briefing on our forthcoming Vacuum Pumps Market study—designed as a practical decision-support tool for executives planning capital allocation, product strategy, and market-entry moves in 2026. The vacuum pumps market is growing steadily from a 2025 base year sized at approximately USD 6,700 Million and, under our central scenario, reaches just under USD 9,910 Million by 2032—a compound annual growth rate of 5.74% across the 2026–2032 forecast window. This trajectory masks important shifts in technology preference, service economics, and regulatory exposure that will determine winners and losers in the next planning cycle.

Vacuum Pumps Market

Actionable horizon: 2026 is a pivot year for many industrial buyers—CapEx budgets set, supplier rationalizations under way, and product specifications being tightened to meet new regulatory and sustainability requirements. Our study translates market growth into practical near-term choices: where to commit manufacturing capacity, which aftermarket capabilities to scale, and which customer cohorts to prioritize.

Vacuum Pumps Market

Risk-adjusted investment: the market expansion is real, but exposure is uneven across technologies, end-markets, and geographies. We provide the risk overlays—tariff, standards, laboratory and environmental regulations—that alter project IRRs and supplier selection criteria.

Vacuum Pumps Market

Supplier ecosystem design: with moderate concentration among incumbents, industrial buyers face trade-offs between single-sourcing for scale and multi-sourcing for resilience. Our analysis quantifies concentration metrics and maps service-capability hotspots to support procurement optimization.

The vacuum pumps market is on a mid-single-digit annualized growth path. Underpinning this headline are several durable demand drivers: the continued build-out of advanced manufacturing capacity (notably in high-vacuum, semiconductor-related processes), regulatory-driven upgrades in environmental and safety-critical manufacturing, and an increased emphasis on energy efficiency and lifecycle cost in industrial equipment procurement. On the supply side, manufacturers are investing in dry technologies and electronic controls that allow higher uptime and lower lifecycle energy consumption—attributes that increasingly factor into purchasing decisions.

Dry versus wet technologies: buyers are accelerating moves toward dry vacuum pumps where process cleanliness, reduced contamination risk, and lower hazardous waste handling are essential. However, wet/liquid-sealed machines retain relevance in specific chemical and heavy-industrial contexts due to lower capital cost and different maintenance profiles.

Electrification, controls and IoT: variable-speed drives, integrated sealing and monitoring packages, and predictive maintenance software are shifting the value proposition from pure hardware to hardware-plus-services. Expect aftermarket and IoT-enabled service agreements to generate a higher share of lifetime revenue.

Materials and spark-resistance: adoption of A2L refrigerants and stricter HVAC standards is increasing demand for certified spark-resistant pumps and recovery units in building-service applications. Similarly, corrosion-resistant materials and coatings are differentiators in chemical-processing applications.

Regulatory changes and tariff classifications are non-trivial to procurement and market planning. Examples affecting supplier selection and product specification include tariff schedules that explicitly reference semiconductor use-cases, new refrigerant safety standards that mandate spark-resistant equipment, and evolving international standards driven through committees active in vacuum-technology standardization. Laboratory biosafety design standards are also tightening, which in turn raises the bar for central vacuum systems used in BSL-3 environments. Our full study provides an indexed regulatory tracker and decision matrix that links each relevant regulation to practical procurement and engineering responses.

The competitive field combines long-established OEMs with specialized niche manufacturers. Market concentration suggests a top-three cluster that holds a meaningful share, while a broader set of five to ten vendors compete across differentiated segments. Key players profiled and analyzed in the report include:

Edwards Vacuum (Burgess Hill, UK) — a wide portfolio spanning high- and ultra-high vacuum solutions, with recent visibility at plastics-focused trade events demonstrating application-led go-to-market tactics (see Edwards Vacuum official channels).

The Busch Group (Germany) — strong in both pumps and blowers, leveraging platform-series launches showcased at major industrial fairs (e.g., Hannover) to push modular product lines and aftermarket contracts.

Atlas Copco (Sweden) — a diversified industrial equipment leader that recently secured ISO certifications relevant to manufacturing and installation; its strength lies in global service networks and integrated offerings across compressed-air and vacuum systems.

Pfeiffer Vacuum, Leybold, Becker Pumps, KNF Neuberger, VACUUBRAND, Gast Manufacturing and Alcatel Vacuum Technology — each occupies differentiated niches from laboratory and research instruments to heavy industrial process pumps, with varying emphasis on aftermarket, channel partnerships and regional service footprints.

Our competitive analysis synthesizes product roadmaps, channel strategies, aftermarket economics and recent go-to-market activity—highlighting where incumbents are defending share and where challengers can find white space (e.g., energy-efficient retrofits, rental/leasing models, and semiconductor equipment supply chains).

Trade-show activity remains a key signal of product strategy. Firms have used global fairs to promote application-specific solutions—plastics degassing, blower series launches, and integrated coating systems—signaling demand pockets where OEMs see near-term growth.

Certifications and standards compliance are increasingly table stakes. The recent tranche of ISO certifications by leading manufacturers is a defensive response to procurement risk-averse buyers demanding documented quality and occupational safety frameworks.

Environmental and process regulations are nudging buyers toward upgraded vacuum solutions that support advanced catalysts and tighter emissions control—an area where vacuum system upgrades can be both compliance enablers and process-performance enhancers.

For executives planning resource allocation in 2026, four strategic plays stand out:

Prioritize service networks and digital offerings: as product differentiation narrows, aftermarket services and IoT-driven uptime guarantees become decisive contract levers. Investment in spares logistics and remote diagnostics yields quick payback on installed fleets.

Certify and modularize for regulatory compliance: embed compliance and safety certification into design releases where markets are regulated (HVAC refrigerants, biosafety, semiconductor equipment lists). Modular designs that allow field retrofits reduce future obsolescence risk.

Adopt an opportunistic M&A posture: mid-market consolidation opportunities exist where service-centric players can be acquired to accelerate local presence, particularly in regions where on-site service responsiveness is a procurement criterion.

Align product R&D to lifecycle cost: focus R&D on energy efficiency, lower maintenance intervals, and reduced waste handling. These attributes are becoming procurement binaries for corporate buyers with sustainability mandates.

This preview sketches the strategic contours; the full report is engineered as an operational playbook for 2026 decisions. Deliverables include:

Granular market-sizing models and scenario-based forecast outputs (interactive dashboards for sensitivity testing);

Segment-level deep dives (type, application, region) and buyer-persona maps that translate demand drivers into procurement specifications;

Detailed vendor profiles with capability heatmaps, channel strategies, recent product pipelines and M&A histories;

Regulation and standards tracker with compliance impact matrices linked to product design and procurement requirements;

Actionable growth playbooks, including target lists for partnership, integration checklists for aftersales roll-outs, and prioritized CapEx scenarios under alternative macro assumptions.

We intentionally withhold the full segmented tables and downloadable financial models in this brief: those are included in the subscription and bespoke consulting packages where clients can access the underlying datasets and scenario tools to run proprietary analyses.

Immediate actions for procurement leaders: update RFP templates to require certifications and IoT interoperability; pilot outcome-based service contracts with a subset of critical assets.

Immediate actions for product and R&D heads: prioritize low-carbon, low-maintenance variants in the 18–24 month roadmap; validate materials and spark-resistant designs against emerging safety standards.

Immediate actions for corporate development teams: screen service-centric targets in geographies where local uptime is a procurement gate—those assets accelerate access to installed-base revenue quickly.

The vacuum pumps market in 2026 is not merely growing; it is reconfiguring around services, regulation, and energy efficiency. Executives who translate the headline growth rate into targeted capability investments—service networks, certification, modular product upgrades, and data-enabled aftermarket offerings—will capture disproportionate value through 2032. For access to the full dataset, vendor scorecards, and scenario tools that support board-level decision-making, please consult the full PW Consulting Vacuum Pumps Market report and our bespoke advisory services.

For detailed analysis of this topic, please visit the official page:Vacuum Pumps Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com