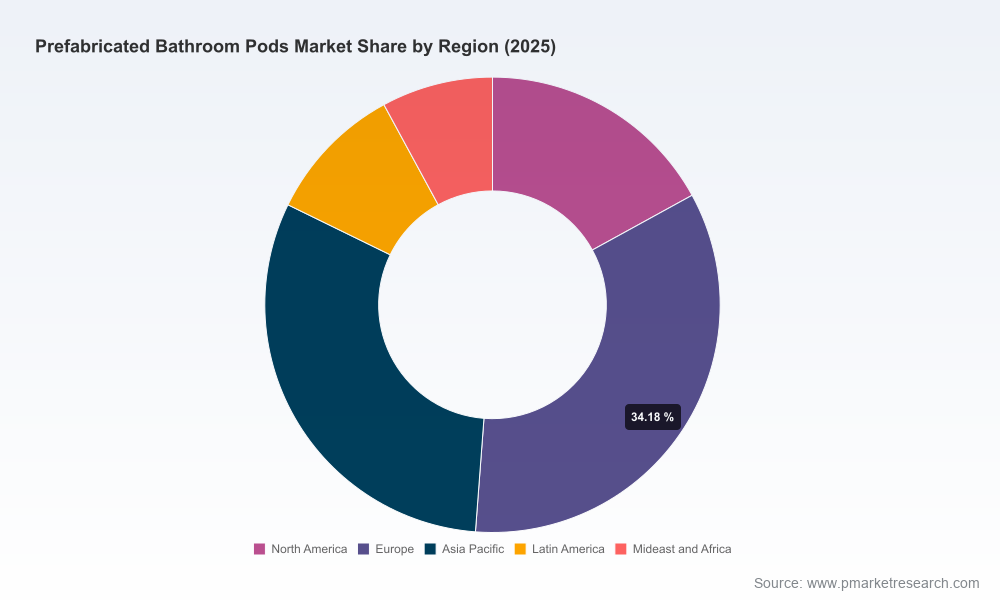

Prefabricated Bathroom Pods Market — Strategic Outlook for 2026 Decision-Makers

Executive summary

The prefabricated bathroom pods market has moved from niche experiment to mainstream delivery model for cost, speed and quality-driven construction programs. Our PW Consulting baseline shows the market expanding from roughly USD 4.3 Billion in 2020 to an estimated USD 6.7 Billion in the base year 2025, with a compound annual growth rate (CAGR) of 9.4% underpinning projections through the 2026–2032 forecast window. Under the central scenario we model a continued acceleration of factory-build adoption across hospitality, healthcare, student housing and multi-family residential segments, producing a market in excess of USD 12 Billion by the end of our forecast horizon.

Prefabricated Bathroom Pods Market

For executive teams making capital allocation, footprint and product strategy decisions in 2026, these topline dynamics matter: offsite bathroom pods are no longer a marginal value play — they are a strategic lever for faster programme delivery, predictable quality and measurable cost control. This briefing highlights where our full study delivers tactical, executable intelligence and why those deliverables should inform board-level decisions this year.

Prefabricated Bathroom Pods Market

Why this report matters in 2026

- Timing and scale: Buyers and specifiers increasingly demand offsite‑manufactured bathroom solutions to meet compressed delivery schedules. Our primary research quantifies the time-to-completion advantages (typical programme acceleration of 40–50%) and maps where that time-savings converts directly into P&L impact.

- Capital allocation: The report translates sector growth into factory sizing, plant-location and CapEx phasing options — enabling CFOs to test low-, base- and high-adoption scenarios against real-world operating metrics.

- Commercial strategy: Procurement and commercial teams receive benchmarks for supplier selection, performance SLAs and negotiation levers aligned with real market concentration dynamics and manufacturing capabilities.

- Risk management: We map the regulatory, material and logistical risks that can blunt adoption, and offer pragmatic mitigation playbooks that can be deployed during 2026 rollouts.

What the PW Consulting study contains (practical deliverables)

- Comprehensive market sizing and a seven-year forecast (2026–2032) built on a 2020–2025 historical base; topline figures are presented in USD (Billion) and stress‑tested across three adoption scenarios.

- Demand-driver analysis linking macro construction trends to pod demand, including segment-level adoption dynamics, procurement cycle changes and lifecycle-cost comparisons versus in-situ construction.

- Supply-side deep dive with a modular cost model: raw material indices, labour-arbitrage sensitivity, factory throughput modelling and logistics cost-to-site calculations.

- Product technology benchmarking covering GRP composites, light-gauge steel, galvanized/galvanized steel frames and lightweight concrete solutions — evaluating durability, weight, fire performance and installation fit-for-purpose.

- Regulatory and compliance matrix aligned with IBC/IRC plumbing codes, inspection regimes and transport/packaging standards (including guidance addressing loss-prevention standards for fire-retardant coverings and on-site protection).

- Operational playbooks for plant design, lean manufacturing adoption, BIM integration and quality control protocols to reduce punch-list risk and speed final sign-off.

- Competitive landscape dossiers and supplier scorecards (manufacturing footprint, production technology, sector focus, digital maturity and strategic partnerships) together with a repo of primary interviews.

- Actionable go-to-market and M&A frameworks: buy vs build decision trees, JV structures for market entry and due diligence checklists tailored for scale plays in 2026.

Competitive landscape — strategic takeaways

The market sits in a phase of moderate consolidation. The top three players capture a material portion of supply, and the top five further extend that concentration — a dynamic that creates both competitive pressure and acquisition opportunity. Larger manufacturers combine scale, standardised production and digital design tools; mid‑sized specialist players differentiate through bespoke design, finish quality and regional responsiveness.

Prefabricated Bathroom Pods Market

Representative company archetypes identified in our research:

- Scale-integrators with standardized lines and international customer pipelines — firms that prioritise capacity and repeatability. These suppliers typically support large hotel chains, healthcare systems and multi-site housing specialists.

- Technology-specialists that advance composite materials and patented framing systems — innovators who trade margin for technical differentiation and speed-to-installation benefits.

- Regional bespoke manufacturers focused on custom finishes and local code compliance — these players win projects requiring design flexibility and tight on-site coordination.

Examples from our company dossiers: several UK and European manufacturers combine GRP and steel-framed production lines and serve hotel, healthcare and student accommodation programmes; a number of North American firms leverage BIM and lean manufacturing to deliver plug-and-play pods for healthcare and hospitality customers; other suppliers operate specialised factories for bespoke defence, remote or luxury hospitality projects. Notable recent developments tracked in the market include a next‑generation steel-framed line launched by a UK supplier in early 2026, significant project deliveries by a French turnkey supplier to hotel and student housing clients, and renewed trade show engagement by North American systems integrators demonstrating code-compliant, rapid-deployment solutions.

Industry dynamics and operational considerations

- Material choice matters: steel-based systems deliver structural strength and load-bearing convenience for multi-storey programmes, while composite (GRP) solutions increasingly win where weight, corrosion resistance and long-term maintenance are priorities.

- Regulation and packaging: manufacturers must design for compliance — not just with building and plumbing codes, but also with transport and storage loss-prevention standards that dictate protective materials and fire-retardant packaging procedures.

- Manufacturing economics: throughput and yield are the dominant drivers of unit marginal cost. Our cost model shows that incremental improvements in cycle time, panel handling and secondary finishing can materially shift gross margins.

- Digital enablement: suppliers using BIM and integrated ERP/PLM systems shorten design-review cycles, reduce RFIs and enable JIT logistics to site. Buyers that mandate BIM deliverables reduce fit-out risk and speed approvals.

- Time-to-market benefit: offsite manufacture continues to prove its case with significant time savings on projects, routinely reducing on-site programmes by 40–50% where supply chain integration is mature.

Actionable recommendations for 2026

- Define a three-horizon manufacturing footprint plan: (1) tactical short-term partnerships and co-packaging agreements to meet immediate demand, (2) medium-term investment in a modular production line aligned with expected adoption curves, and (3) long-term regional plants configured for scale and multi-product capability.

- Adopt a differentiated product strategy: standardise a “workhorse” pod for high-volume projects and maintain a separate bespoke track for premium or complex programmes that command higher margins.

- Hedge material exposure: implement steel procurement hedges, secondary sourcing for critical polymers and index-linked contracts where appropriate to stabilise margins in 2026 procurement cycles.

- Prioritise certification and code engagement: invest in pre-certification and third-party testing to reduce on-site inspection friction and accelerate sign-off timelines in regulated environments.

- Leverage digital mandates: require BIM deliverables from suppliers, adopt integrated QA dashboards and measure supplier KPIs tied to cycle time, rework rates and on‑site punch-list closures.

- Pursue consolidation selectively: given the market concentration dynamics, acquisitive strategies can rapidly expand capacity and customer access; focus on targets with complementary geography, proprietary framing tech or established channel partnerships.

- Run rapid pilot programmes: execute 2–3 controlled pilot builds in 2026 to validate the end-to-end supply chain, test installation workflows and quantify client-level lifecycle benefits for future sales conversations.

Scenario planning — what to watch in 2026

Our forecast framework presents a base case aligned with the 9.4% CAGR, an upside scenario driven by accelerated adoption in healthcare and hospitality, and a downside moderated by raw-material shocks or abrupt regulatory tightening. Key lead indicators to monitor in 2026 include: steel and polymer price trajectories, large-scale developer procurement cycles, incremental building-code amendments, and the velocity of BIM adoption among specifiers.

Next steps and where to find the granular intelligence

This briefing has been designed as a high-value executive preview. The full PW Consulting Prefabricated Bathroom Pods Market report includes the confidential, actionable detail required for transaction diligence, procurement playbooks, plant design economics, and region/application-level demand models that are deliberately omitted here to preserve competitive sensitivity.

For access to the full dataset, Excel-ready financial models, supplier scorecards, primary-interview transcripts and proprietary segmentation tables necessary to operationalise a 2026 strategy, please visit our report page or contact the PW Consulting advisory team. The full study is the working tool we recommend boards and commercial teams use to convert the 2026 market opportunity into measurable, executable outcomes.

For detailed analysis of this topic, please visit the official page:Prefabricated Bathroom Pods Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com