IP Cameras Market 2026: Strategic Preview for Decision-Makers

Introduction: Why this briefing matters to your 2026 strategy

As enterprises, healthcare systems, integrators, and public agencies plan budgets and technology roadmaps for 2026, IP camera strategies are moving from tactical security purchases to strategic infrastructure investments. At PW Consulting we have distilled our latest IP Cameras Market research into an executive-grade preview that highlights the structural drivers, competitive dynamics, regulatory inflection points, and go-to-market implications that will define winners and losers over the coming investment cycle.

IP Cameras Market

Market snapshot—what the numbers say (macro level)

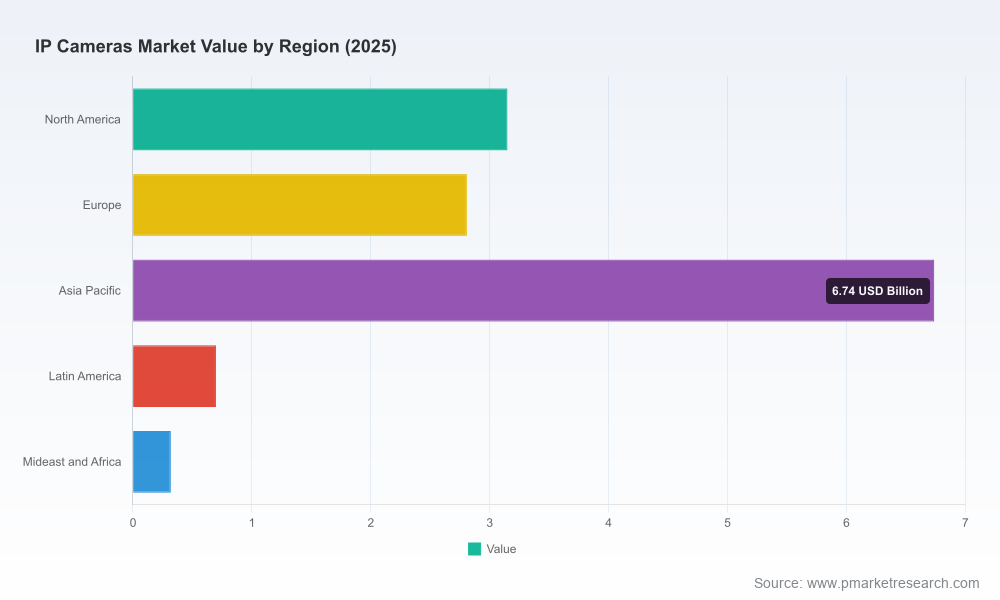

The global IP cameras market has accelerated from a measured growth phase in the early 2020s to a sustained, technology-driven expansion. Using USD Billion as our unit and 2025 as the base year, the market increased materially between 2020 and 2025 and is forecast to continue expanding through 2032 at a compound annual growth rate (CAGR) of approximately 13.0% during the 2026–2032 forecast period. By our forecasts the market crosses into the multiples of tens of billions of USD in the latter half of the decade, reflecting strong demand for networked video, analytics, and cloud-enabled security services.

IP Cameras Market

Two structural facts are worth stressing for strategy planning: first, the market shows moderate-to-high concentration among established vendors (top-three and top-five vendor groups capture meaningful shares of revenue), and second, growth is being re-shaped by software and services (analytics, cloud management, privacy tooling) rather than by camera hardware alone. These macro dynamics should drive how organizations prioritize procurement, partner selection, and capital allocation in 2026.

IP Cameras Market

Key demand-side drivers

- Shift from hardware to platform value: purchasers increasingly evaluate cameras as entry points to analytics, operational tooling, and cloud-managed services. The ability to monetize video streams through operations analytics, patient-safety integrations, or retail conversion metrics is now a primary procurement criterion.

- Regulatory and procurement constraints: government and federal procurement rules, as well as healthcare privacy requirements, are materially changing vendor eligibility and technical specifications for many buyers.

- Healthcare as a strategic vertical: hospitals and care facilities are accelerating deployments for patient safety, fall detection, and workflow integration, but face CapEx limits that make subscription or phased upgrade models attractive.

- Localization and compliance: national technical certifications and import restrictions are creating differentiated regional market access dynamics that vendors must plan for.

Competitive landscape: how leading vendors are positioning

Our qualitative and quantitative work identifies several competitive archetypes shaping the market:

- Platform-first innovators: vendors combining hardware, analytics, and cloud management to offer integrated subscriptions and rapid feature updates.

- Edge-AI specialists: providers optimizing on-device processing for low-latency analytics, privacy-preserving features, and constrained-bandwidth deployments.

- Commodity hardware players: manufacturers competing on unit economics, channel breadth, and integration ecosystems.

- Regulation-focused suppliers: firms that emphasize supply-chain transparency, certifications, and procurement compliance for public-sector and healthcare customers.

Profiles — what the market needs to know about core incumbents

- Axis Communications AB (Lund, Sweden) — A leader in ARTPEC-based network IP cameras. Axis emphasizes image quality, embedded processing and a strong compliance posture, making it a common choice for healthcare deployments where privacy and clinical workflows intersect. Recent product introductions also signal a sustainability orientation.

- Hanwha Vision (South Korea) — Differentiates with AI-enabled cameras and modular systems that integrate with healthcare EHR/clinical systems. Positioning around fall detection and clinical workflow integration makes Hanwha attractive for hospital customers seeking application-specific solutions.

- Dahua Technology (Hangzhou, China) — Offers comprehensive video-centric AIoT solutions for facility operations and security. Its scale and product breadth are advantages in commercial and infrastructure projects, though procurement restrictions may limit access in some public-sector markets.

- Bosch Security Systems (Stuttgart, Germany) — Known for deep integration capabilities with building and hospital infrastructure, positioning its cameras as components of broader facility security and safety systems.

- Pelco (Fresno, CA, USA) — Focused product lines designed for regulatory-compliant hospital monitoring and patient-safety use cases. Pelco’s Sarix series is positioned for critical indoor coverage and compliance-focused buyers.

- Hikvision (Hangzhou, China) — Large-scale supplier of network IP cameras and solutions for facility operations. Regulatory exclusions in some procurement environments constrain its addressable market for public-sector and federally funded projects.

- Verkada (San Mateo, CA, USA) — Cloud-managed platform emphasizing privacy controls and enterprise-grade compliance features, including tooling to support HIPAA-constrained deployments, which appeals to healthcare and enterprise customers prioritizing cloud simplicity and governance.

- Honeywell International Inc. (Charlotte, NC, USA) — Provides robust performance-series and specialized (including explosion-proof) cameras for critical infrastructure and secure healthcare environments, backed by broad systems integration capabilities.

- Arecont Vision (USA) — Offers high-resolution megapixel cameras for projects that prioritize image fidelity and large-area coverage—relevant for renovation projects and upgrades where legacy analog systems are being replaced.

Regulatory and procurement posture: what changes in 2026 mean for buyers and vendors

- US federal procurement: Section 889 and NDAA eligibility rules continue to influence vendor selection. Federal and federally funded buyers are required to source NDAA-compliant devices; vendors excluded under these provisions face restricted access to a meaningful segment of public procurement.

- Healthcare privacy: HIPAA requirements remain a gating factor for any deployment capturing patient or clinical data. Features such as selective face blurring, role-based access controls, and audit trails are no longer optional for healthcare customers.

- National technical certification: new mandatory standards (for example, recent STQC-type requirements in key markets) are raising the bar for device-level security and compliance. Vendors should prioritize certification roadmaps to avoid market access delays.

Deployment realities and buyer constraints

Hospitals and large facilities present a unique mix of demands: discreet hardware (e.g., fixed dome designs for corridors and waiting areas), integration with clinical systems, and strict privacy controls. However, many healthcare providers face CapEx pressures that slow full-scope refresh programs for AI-enabled systems. We therefore observe a rise in hybrid procurement approaches—phased rollouts, managed service contracts, and analytics-as-a-service pilots—that align upfront expenditure with measurable operational outcomes.

Actionable strategic plays for 2026

- For vendors: prioritize product architectures that balance edge analytics with cloud orchestration, and accelerate certification programs (security and national technical standards). Offer flexible commercial models (CapEx-friendly and subscription/multi-year Opex) to overcome buyer budget cycles.

- For integrators and systems houses: develop repeatable reference architectures for healthcare and public-sector projects that embed compliance controls and interoperability with major EHR and facility management systems; this reduces friction in procurement and tender evaluations.

- For enterprise and healthcare buyers: treat IP camera projects as platform decisions. Require vendor roadmaps for analytics, privacy features, and supply-chain transparency. Consider staged pilots that measure operational savings (reduced falls, faster incident resolution, optimized staffing) before broader rollouts.

- For investors and M&A teams: look for targets with defensible software stacks, certification footprints, and channel strengths in regulated verticals. A premium is likely for companies that combine on-device AI with strong compliance credentials and recurring revenue models.

What the full PW Consulting report delivers

This strategic preview highlights core themes and implications; the complete study provides the granular intelligence decision-makers need to act. The full report includes:

- A detailed market model (historical 2020–2025 and forecast 2026–2032) with scenario analysis

- Segment-level demand drivers and sensitivity testing (by camera architecture, application vertical, and procurement channel)

- Competitive benchmarking, including product feature matrices, go-to-market strengths, and certification status

- Procurement playbooks for healthcare, federal, and commercial buyers—covering compliance checklists, RFP language, and total cost of ownership frameworks

- M&A and partnership scouting templates for strategic buyers and investors

To protect the strategic value of the report and to follow the “trailer” principle, we have intentionally withheld granular subsegment tables and regional/application share breakdowns from this preview. Those detailed breakdowns—critical for capital allocation and procurement decisions—are available in the full study.

Closing—immediate next steps for leaders

As 2026 budgets are finalized, IP camera decisions will have outsized impact on both operational efficiency and regulatory compliance. Executives should prioritize three near-term actions: (1) require vendor compliance certifications as a pass/fail criterion in procurement, (2) budget pilots that demonstrate measurable operational ROI before enterprise-wide commitments, and (3) align security and clinical leadership early to resolve privacy and integration requirements.

PW Consulting’s full IP Cameras Market report contains the proprietary models and playbooks to operationalize these recommendations. Contact our research desk to access the complete dataset, vendor scorecards, and the procurement templates that will allow your organization to turn 2026 uncertainty into strategic advantage.

For detailed analysis of this topic, please visit the official page:IP Cameras Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com