Medicinal Herbs Market Dynamics: Key Drivers and Restraints

Other |

2026-03-02 04:30:50

As PW Consulting’s lead industry analyst, I present a focused strategic preview of the Pad Printing Supplies market designed to inform executive decision-making for 2026. This brief demonstrates the types of insight and actionable guidance contained in our full study (base year 2025; historical window 2020–2025; forecast horizon 2026–2032). It purposefully surfaces high‑value signals — growth trajectory, competitive fault lines, regulatory inflection points and near‑term commercial plays — while reserving detailed subsegment tables and regional splits for the full report.

Pad Printing Supplies Market

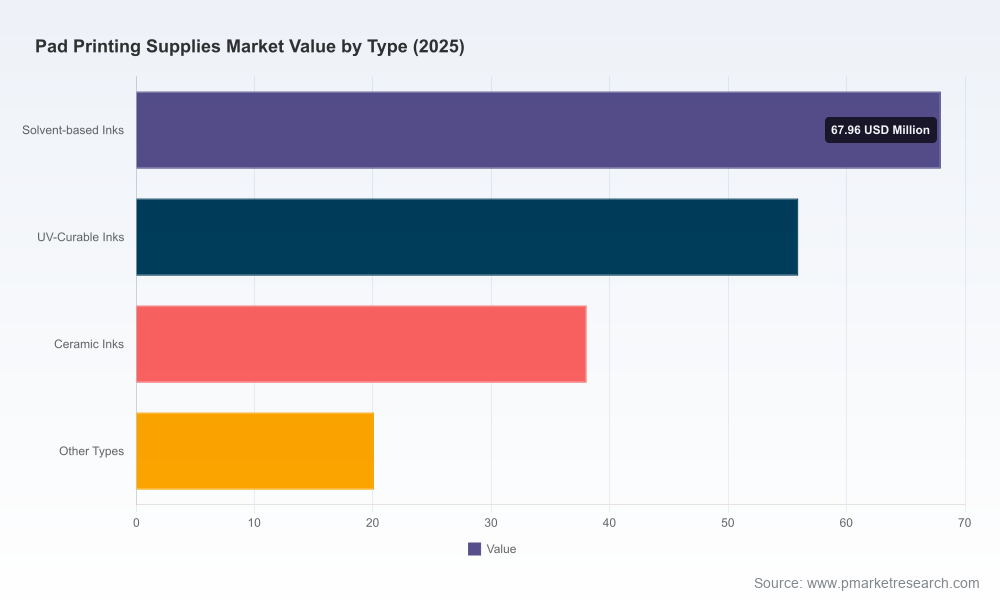

The pad printing supplies market has moved from a niche industrial specialty into a stable, mid‑single‑digit growth market. Our analysis benchmarks the market at a base year value in 2025 and identifies a compound annual growth rate of approximately 5.65% across the forecast window. That trajectory reflects steady demand elasticity across end‑markets such as product decoration, electronics marking, medical/biocompatible printing and packaging decoration, combined with incremental price and value capture from premium eco‑compliant formulations and automation enablement.

Pad Printing Supplies Market

For 2026, the implication is clear: the market is large enough to support differentiated players yet fluid enough for focused strategies to materially change competitive positioning within 12–24 months. Suppliers that can demonstrate regulatory compliance, validated eco‑credentials and integration capability with automated production lines will command pricing power and faster route‑to‑adoption among OEMs and contract manufacturers.

Pad Printing Supplies Market

Regulation is a market shaper. Recent product launches and certifications underscore how compliance credentials (REACH, RoHS, toy‑safety standards, and voluntary schemes such as GOTS or Eco‑Passport) are moving from “nice to have” to procurement gatekeepers. Buyers increasingly place certified ink systems and documented biocompatibility at the front of RFQs, creating premium segments for compliant suppliers.

Eco‑formulations that remove phthalates, PAHs and problem solvents are driving buying decisions in packaging, toys and consumer electronics. Suppliers that can back sustainability claims with third‑party certification and lifecycle logic (e.g., recyclability on printed substrates) reduce buyer friction and shorten qualification cycles.

As customers automate decoration and high‑volume marking, they prefer suppliers who deliver more than inks — pads, printing plates, tooling and process integration support. Companies that offer turnkey automation or tight machine‑to‑consumable compatibility shorten installation time and total cost of ownership, creating sticky commercial relationships.

Incremental material advances (UV‑curable chemistries with improved adhesion; solvent systems balanced for faster cure and lower VOCs; ceramics with improved firing windows) are where immediate margin uplift is achievable. These innovations require supporting application data; hence, field validation programs and co‑development pilots are powerful go‑to‑market tools.

Speed of fulfillment is a differentiator in 2026. Suppliers with regional warehousing and rapid custom‑mix capabilities will win in time‑sensitive verticals. Conversely, players that accept longer lead times must compete on price or niche properties.

The competitive field contains a mix of specialized pad‑printing manufacturers, ink houses with broader print portfolios, and machine/consumable integrators. Below are distilled strategic profiles of core incumbents we tracked; these snapshots highlight where each player is likely to pressure margins, set standards or create switching costs in 2026.

Strengths: Comprehensive product breadth — from inks and pads to laser cliché production — positions TAMPOPRINT as a technical incumbent for OEMs requiring full‑stack solutions. Strategic posture: deepen systems integration and leverage engineering services to defend higher ASPs.

Strengths: Recent product introductions emphasize solvent‑based and sustainable formulations. Their INXPad T200 launch demonstrates how product innovation tied to regulatory compliance can accelerate adoption in packaging and consumer segments. Strategic posture: use certification and application case studies to expand into adjacent high‑volume markets.

Strengths: Broad portfolio of solvent and UV systems targeted at industrial decoration. Their compliance posture reduces procurement friction in regulated industries. Strategic posture: cross‑sell into existing industrial channels and prioritize technical service for adhesion/chrome applications.

Strengths: Focus on consumables, custom mixing and automation support makes them a partner of choice for contract printers seeking turnkey conversion. Strategic posture: scale service offerings and proprietary pad formulations to increase customer lifetime value.

Strengths: Eco‑centric product series with third‑party certifications, plus hardware consumables such as ink cups and ceramic rings. Recent certifications position them well in child‑sensitive and consumer packaging segments. Strategic posture: elevate verified sustainability as a primary sales narrative.

Strengths: Custom machines and tooling for high‑volume automated deployments; appeal is strongest where throughput and repeatability matter. Strategic posture: bundle machines with consumable supply agreements to capture recurring revenue.

Strengths: Full‑range supplier with one of the largest regional ink warehouses; distribution muscles provide speed and service advantages. Strategic posture: monetize inventory advantage through service‑level guarantees and short‑cycle delivery premiums.

Strengths: In‑house silicone pad production and tooling; strong in customization and small‑lot specialty runs. Strategic posture: position as agile partner for product innovation and low‑volume high‑margin runs.

Collectively, these firms illustrate a market where product development, certification and systems integration are primary battlegrounds. Recent public developments — e.g., the INXPad T200 product launch and Inkcups’ GOTS and regulatory certifications — are representative: product announcements that combine performance and compliance get rapid traction with purchasing teams.

The full PW Consulting report converts market context into executable plans. Highlights include:

Importantly, the full dataset contains the detailed subsegment breakdowns, regional allocations, and company‑level share tables that commercial teams need to build tactical plans. Those tables are intentionally omitted here to preserve the “preview” nature of this summary.

Within 30 days, map current SKUs against buyer compliance requirements for priority verticals. Identify quick‑win certifications or test partners to eliminate procurement blockers.

In 60 days, run process compatibility pilots combining your inks/pads with leading automation platforms. Capture OEE and scrap‑rate improvements to build customer ROI cases.

In 90 days, launch an evidence‑based kit (certificates, LCA highlights, compatibility notes) to shorten buyer qualification cycles in packaging and consumer segments.

Our findings are grounded in multi‑method research: market transaction mapping, supplier financials, proprietary demand models, and over 40 qualitative interviews with OEM procurement leads, contract decorators and technical R&D managers. We triangulate supplier claims (product launches, certifications) with third‑party standards and on‑the‑ground pilot data to ensure that growth trajectories and margin forecasts are operationally realistic.

The base year, 2025, anchors current market scale and supplier positioning; the forecast period through 2032 models alternate adoption curves for UV and green chemistries, plus sensitivity to raw material and regulatory shocks. The result is a practical forecast and decision framework that procurement, product and corporate development teams can use immediately.

This preview highlights the strategic value of the full PW Consulting study for 2026 planning cycles: it connects macro growth, competitive dynamics and regulatory pressures to concrete operational moves. If your objective for 2026 is to accelerate share in higher‑value segments, shorten qualification times, or design a defensible product roadmap, the full report contains the complete subsegment tables, regional breakdowns and supplier scorecards required to execute those plays.

Request the full report to access:

Contact PW Consulting to schedule a briefing where we will: validate your strategic priorities against our findings, run a tailored scenario for your portfolio and outline an implementation roadmap you can start executing in Q1 2026.

For detailed analysis of this topic, please visit the official page:Pad Printing Supplies Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com