100M Electrical Port Module Market 2025: US$ 385 Million by 2032 at 8.7% CAGR

Other |

2026-06-01 09:29:30

As PW Consulting’s senior strategy team and lead industry analysts, we present a focused orientation to our full Bone Morphogenetic Protein (BMP) 2 Market study and its direct utility for leadership teams making decisions in 2026. This preview is designed as a strategic “trailer”: it surfaces the analytical architecture, the macro trajectory, and the highest‑value implications we identify — while intentionally withholding granular segment-level figures to preserve the consultative value of the full report and encourage direct access to the underlying models and appendices.

Bone Morphogenetic Protein (BMP) 2 Market

At the aggregate level, BMP‑2 is a growth market with sustained mid‑single digit expansion. Our consolidated market model — covering historical performance (2020–2025), a base year of 2025, and a forward forecast window through 2026–2032 — quantifies a compound annual growth rate (CAGR) of approximately 5.5% over the forecast period. The market has moved from mid‑2020s baseline values into a considerably larger market by the end of the decade, reflecting rising clinical adoption, incremental indication updates, and steady price/volume dynamics.

Bone Morphogenetic Protein (BMP) 2 Market

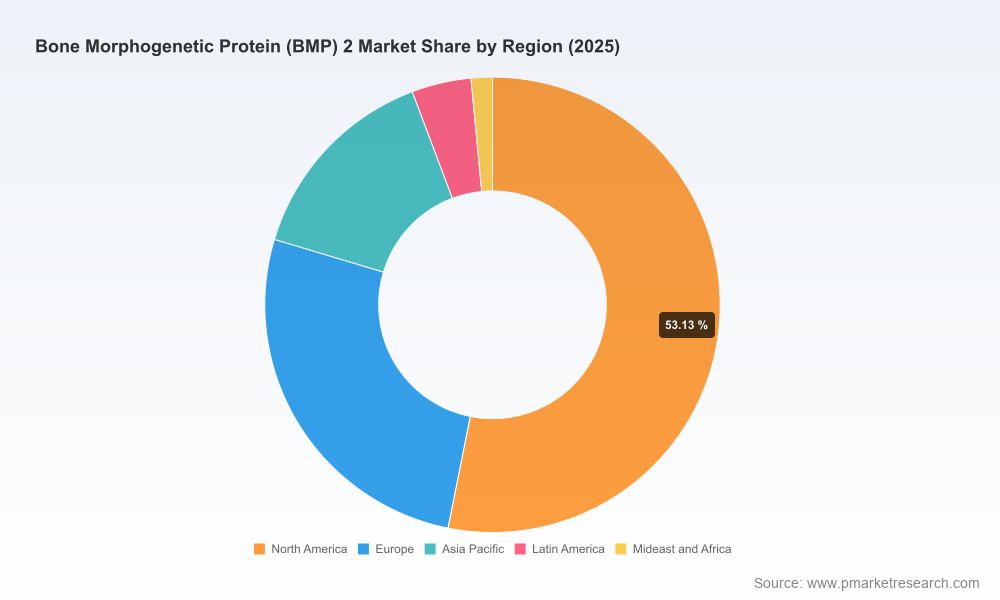

Two structural observations follow from this macro picture. First, the growth profile is predictable enough to support multi‑year commercial and manufacturing planning, yet it is punctuated by episodic policy and regulatory shifts that materially affect near‑term uptake. Second, concentration is meaningful: the incumbent cohort commands a dominant share of commercialized, approved therapeutic BMP‑2 offerings, which creates both barriers and strategic opportunities for challengers and adjacent players.

Bone Morphogenetic Protein (BMP) 2 Market

Medtronic remains the anchor competitor in the BMP‑2 ecosystem through ownership and manufacture of its INFUSE Bone Graft (containing recombinant human BMP‑2 on an absorbable collagen sponge). The product portfolio is positioned across several surgical specialties and indications, and the company retains a unique regulatory footprint as the primary approved vendor in multiple procedural categories.

Notably, regulatory/reimbursement developments in 2026 have practical implications for market participants. In March 2026, the Centers for Medicare & Medicaid Services (CMS) issued Spring ICD‑10‑PCS Questions and Answers that reaffirm ongoing FDA‑approved indications for INFUSE Bone Graft and introduced new procedural coding guidance related to the introduction of recombinant BMP‑2 into joints. This development reduces near‑term coding ambiguity and, by extension, execution risk for providers and payers considering use of BMP‑2 in expanded procedural settings.

For strategy teams, the combination of a concentrated supplier market and clearer reimbursement coding reduces one class of uncertainty (coverage/coding) while sharpening attention on others (clinical evidence generation, off‑label use management, and supply chain scale). Our full study includes a clinic‑to‑payer impact synthesis that translates these policy updates into revenue sensitivity scenarios under alternative adoption curves.

Comprehensive market model: historical (2020–2025) and forecast (2026–2032) demand and revenue model denominated in USD, with configurable assumptions for price evolution, procedure volumes, and substitution dynamics.

Scenario and sensitivity analysis: three deployment scenarios (conservative, base, upside) that stress test the 5.5% CAGR baseline against alternative reimbursement, regulatory, and clinical adoption pathways.

Regulatory and reimbursement mapping: a timeline and decision matrix for regulatory filings, coding shifts, and payer policy triggers; includes implications of the March 2026 CMS ICD‑10‑PCS update for joint introductions.

Competitive diagnostics: strategic profiles for incumbent and emerging players, capability assessments (manufacturing, clinical evidence, distribution), and an M&A/divestiture playbook. We profile Medtronic in depth and benchmark its position against market concentration metrics.

Commercial playbooks: go‑to‑market options by channel (hospital systems, OEM partnerships, specialty distributors), pricing levers, and stakeholder engagement approaches for surgeons, health systems, and payers.

Clinical and pipeline assessment: curated review of late‑stage clinical programs, device/device‑combination developments, and the evidence thresholds required to expand indications into elective joint, trauma, and reconstructive domains.

Operational readiness checklist: manufacturing scale requirements, quality/regulatory controls, and supplier risk matrices that matter if stakeholders plan to commercialize or source BMP‑2 products at scale.

Primary research annex: interview extracts from leading orthopaedic surgeons, hospital procurement leads, and payers, supplemented by a proprietary provider survey that informs adoption assumptions.

The BMP‑2 market exhibits marked concentration among a handful of firms. Firms at the top of the stack capture a substantial proportion of commercial activity, which creates a two‑edged environment: predictable ordering and clinical familiarity where incumbents operate, but higher friction for entrants seeking OR time, formulary placement, and payer acceptance. Our CR3 and CR5 concentration metrics — included in the full report — quantify this dynamic and are used to calibrate competitive scenarios and M&A valuations.

Align evidence generation to payer decision points: With CMS clarifying codes in 2026, commercial success will hinge on targeted post‑market studies and economic models that speak directly to hospital CFOs and MAC‑level coverage committees. Sponsors should prioritize health economic data packages that demonstrate cost neutrality or system‑level savings in the first 12–24 months post‑procedure.

Design a phased regulatory and launch roadmap: Pursue a prioritized indication sequencing that balances clinical returns with cost‑to‑serve. Early wins in clearly coded procedural areas can underwrite later expansion into more elective or niche applications.

Operationally de‑risk manufacturing: Scale plans should be aligned with the predictable mid‑single digit market growth baseline but include contingency capacity for demand surges tied to new indications or large system adoption. Quality and supply continuity are material differentiators given the concentrated buyer base.

Consider strategic partnerships and licensing: For non‑incumbents, partnering with established distribution channels or OEMs can accelerate access to hospitals and surgical centers where incumbents maintain deep relationships. For incumbents, licensing or co‑development can extend an IP moat into adjacent product formats or delivery matrices.

M&A as a scale and capability lever: Given the market concentration, bolt‑on acquisitions that add clinical evidence, novel delivery platforms, or manufacturing capacity can be value‑accretive. Our report provides an M&A screening matrix that aligns target profiles with value creation levers.

Refine surgeon and health system engagement: Clinical champions remain the dominant adoption vector. Coordinate training, evidence dissemination, and OR support to shorten the adoption lifecycle and minimize practice inertia.

Prepare for payer playbooks around utilization management: Expect payers to require pathway governance, prior authorization templates, and registry participation in exchange for favorable coverage. Early engagement and joint value agreements can materially de‑risk uptake.

For strategic acquirers, the market’s concentration and regulatory clarity create defined pockets for consolidation and technology acquisition. For growth equity and late‑stage investors, predictable macro growth (CAGR ~5.5%) combined with identifiable operational levers offers a planning horizon to model return on investment with moderate confidence. For new entrants and smaller innovators, success will depend on asymmetric advantages (novel delivery modalities, compelling cost‑offset data, or unique manufacturing economics) that can displace incumbent preference hierarchies.

This briefing surfaces the decision‑relevant contours of the BMP‑2 opportunity set for strategic planning in 2026. It is explicitly a directional and diagnostic asset: the full PW Consulting BMP‑2 Market study contains the underlying models, scenario outputs, and proprietary interview transcripts that translate this orientation into executable plans. We have intentionally withheld granular segment‑level breakdowns from this preview to preserve the strategic advantage embedded in our primary research and modeling.

If your team is preparing capital allocation, commercial entry, or product strategy decisions for 2026, the full report provides the quantitative backbone and the playbooks needed to move from intent to execution.

For detailed analysis of this topic, please visit the official page:Bone Morphogenetic Protein (BMP) 2 Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com