Versatility Across Industries Keeps the Glycerinee Market Growing Strong

Networking |

2026-06-17 14:11:31

As the shipping software market moves from point solutions to platformized, API-first ecosystems, executives face a compressed window in 2026 to convert opportunity into durable advantage. This primer — prepared by PW Consulting’s senior strategy team — synthesizes the directional market forces, competitive fault lines, and practical actions that should frame boardroom discussions this year. It demonstrates the strategic value of the underlying market study while deliberately withholding granular segment tables and proprietary scorecards so you will consult the full report for transaction- and deployment-level intelligence.

Shipping Software Market

The shipping software market has matured from its origins as label and postage utilities into a multi-functional stack that now spans rate shopping, carrier orchestration, fulfillment execution, post-purchase customer experience, and embedded marketplace integrations. On a macro basis, the market was worth roughly USD 2.19 billion in 2025 and is projected to grow to about USD 3.87 billion by 2032 — a compound annual growth rate of approximately 8.5% over the forecast window. That trajectory reflects both secular digitalization in logistics and accelerated adoption by e-commerce, 3PLs, and enterprise shippers seeking to automate complexity.

Shipping Software Market

Market structure is informative: concentration is moderate — the top three vendors account for roughly a third of market revenue, while the top five approach half. That mix creates space for specialized entrants (API providers, e-commerce-focused platforms) to scale quickly, while legacy enterprise vendors defend by leveraging ERP/WMS integration, installed-base relationships, and broader supply chain suites.

Shipping Software Market

Cloud and API economics are now center stage. Platform buyers judge vendors less by feature lists and more by API coverage, reliability, and operational economics. Decision-makers must build realistic TCOs that include cloud hosting, API transaction fees, and third-party middleware costs. As an industry benchmark, cloud hosting variability ranges widely month-to-month; API licensing for mid-to-high-volume use cases can add material monthly cost (benchmarks show processing 100,000 API calls/month can incur hundreds to low thousands of dollars in fees). These line items materially affect unit economics for high-volume fulfillment models.

Labor and downtime drive urgency. Labor remains the dominant expense in many distribution-intensive industries, and automation in shipping execution is one of the clearest levers to control that spend. Equally, downtime is costly: enterprises report minute-level incident costs that rapidly escalate into material financial exposure. High-availability architectures and well-practiced incident response plans are no longer optional.

Regulatory and data-transfer pressures are rising. The EU Data Act and related cross-border data regimes introduce new cost and compliance vectors for cloud-based providers and their customers, particularly where shipment telemetry, returns processing, and customer data cross jurisdictions. These rules are poised to affect cloud transfer pricing and contractual terms beginning in the near term, and vendors’ contractual agility will influence enterprise adoption.

Integration velocity is a competitive moat. Shipping software does not sell in isolation — it wins or loses based on the quality and breadth of integrations (marketplaces, carriers, ERPs, WMS, OMS). The ability to deliver out-of-the-box connectors and low-friction migration paths materially shortens payback on implementation.

Feature convergence, product differentiation moves to platform-level services. Basic features — label printing, tracking, rate shopping — are table stakes. Differentiation is shifting to intelligent routing (AI delivery estimates), branded post-purchase experiences, returns orchestration, and freight/parcel hybridization for LTL and parcel workflows.

The vendor ecosystem spans several archetypes: legacy enterprise suites, dedicated e-commerce platforms, API-first pure plays, and specialist integrators. Understanding strategic positioning across these archetypes is critical when evaluating vendors for scale, flexibility, and long-term lock-in risk.

Enterprise integrators and suites (SAP, Oracle, Manhattan Associates, BluJay): These incumbents sell depth across supply chain modules and draw adoption from organizations prioritizing tight ERP/WMS coupling and governance. Their strength is in end-to-end process integration and enterprise support, but buyers should expect longer implementation cycles and the potential need for additional middleware for carrier breadth.

Multi-carrier and fulfillment platforms (Pitney Bowes, Descartes, Metapack, ProShip, ConnectShip): These vendors combine carrier ecosystems with fulfillment execution capabilities. For example, Pitney Bowes continues to evolve its SaaS shipping and mailing solutions — recent product updates and leadership moves in 2025–2026 underscore active product and go-to-market investment. ConnectShip’s introduction of new broker rating functionality demonstrates how feature evolution targets enterprise freight orchestration gaps.

API-first pure plays and e-commerce specialists (EasyPost, Shippo, ShipStation, AfterShip, Stamps.com): These providers prioritize developer experience, fast integrations with storefronts and marketplaces, and modular billing. They are attractive to mid-market and high-growth e-commerce customers that value time-to-market and flexible routing. AfterShip’s investments in post-purchase UX and returns tools highlight the increasing importance of delivery experience as a revenue driver.

Emerging orchestration and marketplace-focused players: Vendors that bridge marketplace compliance, cross-border logistics, and branded customer experiences are gaining traction. Expect continued alliances between niche vendors and larger ERP/SCM channels to accelerate distribution.

Recent vendor activity — leadership hires, product releases, and partnerships — signals two things: incumbents are actively modernizing, and channel partnerships (for example, integrations with Oracle Fusion Cloud SCM) are a preferred route to expand enterprise footprint. For deal teams, this implies that strategic diligence should include not only product fit but partnership durability and roadmaps.

The full study is structured as a playbook for 2026 execution. Highlights include:

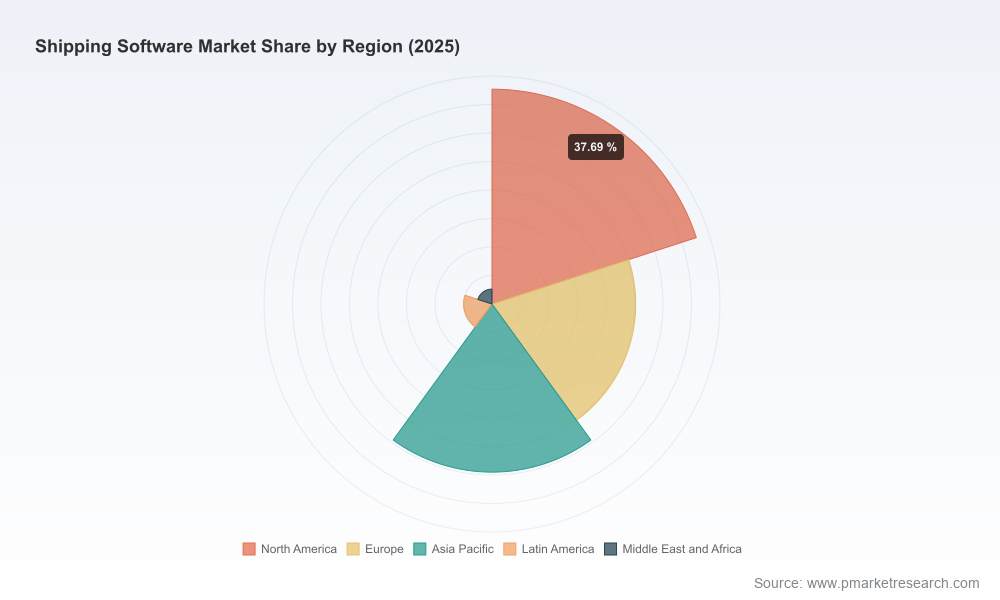

Note: this primer intentionally omits the granular regional and application-level splits that appear in the full study. Those segmentation details and the vendor-by-segment revenue matrices are available only in the complete report and are essential for deal-level decisions.

For executive teams, 2026 represents an inflection where decisions on platform architecture, vendor selection, and commercial terms will determine whether shipping becomes a cost center or a customer-acquisition advantage. The market’s steady expansion — underpinned by an expected ~8.5% CAGR and a near-term base exceeding USD 2 billion — makes the opportunity clear. But the path to capture value requires disciplined cost modeling (APIs and hosting), regulatory foresight, and pragmatic vendor evaluation.

PW Consulting’s full Shipping Software Market report provides the segmented tables, vendor scorecards, and deployment-level models needed to translate this strategic primer into executable plans. For access to the detailed segmentation, vendor comparisons, and implementation assets that senior decision-makers require, consult the PW Consulting report page linked from our 2026 research release.

For detailed analysis of this topic, please visit the official page:Shipping Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com