Soft Ferrite Core Market: A Strategic Briefing for 2026 Decision-Makers

PW Consulting presents a focused strategic introduction to our full Soft Ferrite Core Market study. This briefing synthesizes the market trajectory, supply-chain dynamics, competitive posture and the operational playbook that senior executives, procurement leaders and product strategy teams need to consider as they set course for 2026. The narrative demonstrates the analytic depth in our work while preserving the detailed segment-level tables and proprietary models that are available in the full report.

Soft Ferrite Core Market

Executive snapshot

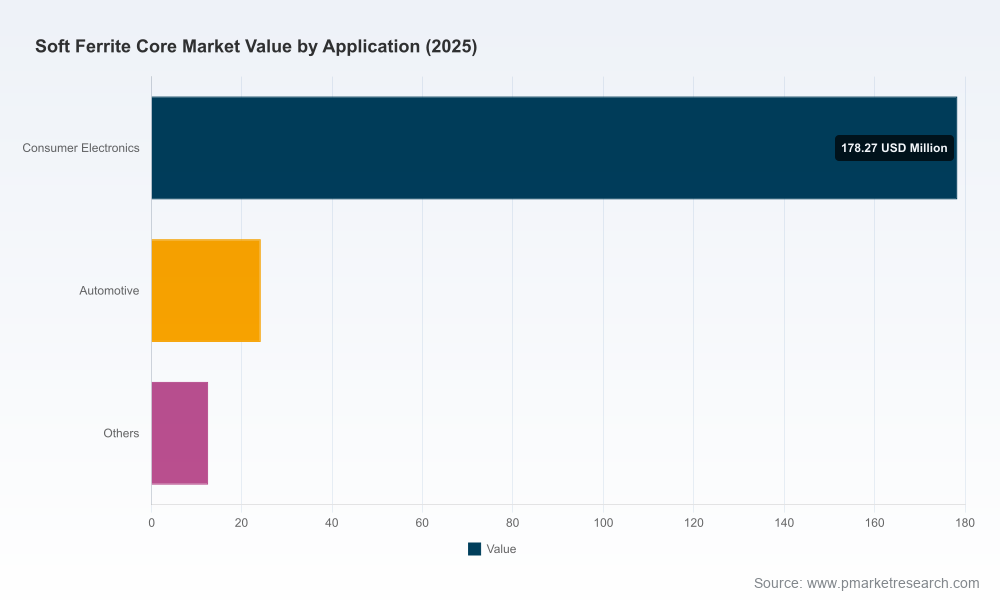

The soft ferrite core market has shown steady expansion through the mid-2020s. Our base year is 2025, when total industry revenues reached USD 215.0 Million. Under our central forecast the market grows at a compound annual growth rate (CAGR) of 6.98% across the 2026–2032 horizon, reaching roughly USD 345 Million by 2032. Historical context (2020–2025) and this medium-term forecast together illuminate the structural growth drivers—electrification, power conversion density, EMI mitigation and high-frequency designs—while also revealing material and policy headwinds that will shape supplier economics and capacity planning in 2026 and beyond.

Soft Ferrite Core Market

Why this matters for 2026 strategy

- Capital expenditure and capacity timing: With a sub-7% CAGR and pockets of accelerated demand, investment decisions for new tooling and lines must be timed to avoid both underutilization and missed demand windows.

- Procurement and input-cost risk: Raw-material volatility and regulatory constraints are elevating procurement risk; 2026 is a year to move from transactional spot buying to hedged, contract-based sourcing.

- Product roadmaps and design-for-supply: Designers must optimize magnetic component choices for manufacturability and supply resilience rather than only for component-level performance.

- M&A and partnerships: Market fragmentation creates opportunities for consolidation, regional partnerships, and vertical integration—especially where raw-material access or specialized geometries confer advantage.

Market dynamics and material realities

The market’s growth profile coexists with important supply-side constraints and regulatory shifts that materially affect margins and decision risk in 2026.

Soft Ferrite Core Market

- Input-cost inflation: Producer Price Index data for Nonmetallic Mineral Products reached 352.91 by August 2025, reflecting steady moderate inflation across inputs relevant to ferrite manufacturing. This trend compresses margins where pricing is fixed or slow to adjust.

- Commodity pressures: Manganese oxide—critical for certain ferrite chemistries—saw sharp price moves historically (notably a 19% rise in 2023) and remains subject to episodic supply tightness. For Ni-Zn ferrite product lines, raw materials (iron oxide, zinc oxide, nickel) can represent a substantial share of manufacturing cost; historical annual price swings of 15–35% mean cost pass-through and hedging strategies are essential.

- Supply disruptions and purity impacts: Declines in iron-oxide grade availability due to mining interruptions have reduced certain high-purity feedstocks, extending lead times and forcing qualification cycles for alternative sources.

- Regulatory constraint: New quotas take effect in 2026—example: tighter manganese import quotas implemented by regulatory authorities require companies to model scenarios with roughly 15% lower manganese import availability in baseline shock cases.

These dynamics translate into five operational imperatives for 2026: secure diversified suppliers, price for volatility, validate alternative chemistries, increase inventory at critical nodes selectively, and strengthen raw-material intelligence.

Competitive landscape — positioning and options

The sector is neither a tight oligopoly nor uniformly fragmented. Market concentration metrics indicate moderate dispersion: the share controlled by the top three firms is roughly in the mid-20-percent range, and the top five add only a few percentage points beyond that. That profile creates a market of established global players alongside regional specialists and contract manufacturers.

- TDK Corporation (Tokyo) — A technology leader with broad product breadth across Mn-Zn and Ni-Zn cores and multiple form factors (PQ, E, toroid, planar). Its recent product expansion into large-size cores for EV charging, UPS, solar inverters and motor drives underscores a strategic pivot to electrification applications and higher-value industrial use-cases.

- Ferroxcube (Weert) — A global producer with European roots and manufacturing spread across Europe, Asia and North America. Strengths include supply-chain reach and a product portfolio positioned for telecom, power and industrial segments.

- DMEGC Magnetics (China) — Large-scale Chinese manufacturer offering standard and custom geometries with cost-competitive supply; important in power-supply and automotive component ecosystems.

- MAGNETICS Inc. (USA) — Focused on Mn-Zn cores for chokes and inductors with strong placement in telecom, aerospace and medical verticals where qualification cycles and reliability command premiums.

- Proterial, Cosmo Ferrites, Acme Electronics and other regional players — Offer complementary capabilities in advanced low-loss materials, export-oriented manufacturing, and local-service responsiveness.

Recent corporate moves—such as TDK’s July 2025 lineup expansion for EV charging and Premo & Delta Manufacturing’s June 2025 joint venture to strengthen component manufacturing in India—signal strategic shifts: emphasis on electrification, regional capacity-building and closer manufacturer-EMS integrations. For buyers and investors, these moves are early indicators of where capacity and technology differentiation will concentrate.

What the full report delivers (practical, actionable content)

PW Consulting’s full study converts the above qualitative signals into operational tools executives can use in 2026. Highlights include:

- Multi-scenario demand model (tailored to electrification, consumer electronics cycles and industrial spend), with downloadable spreadsheets you can parameterize for your portfolio.

- Manufacturing cost and margin model that maps raw-material cost drivers, energy and labor inputs, and scale economics across common form factors.

- Supplier heatmap and qualification scorecards that combine capability, geography, lead time, and risk—built to support dual-sourcing and nearshoring decisions.

- Regulatory-impact assessment and compliance playbook (including import quota scenarios and mitigation tactics such as bonded inventory and tariff engineering).

- Procurement playbook with contract templates, hedging approaches, inventory strategies (safety stock vs just-in-time), and negotiation levers tied to volume and design flexibility.

- Commercial and product roadmaps mapping which core geometries and chemistries deliver the best TCO across target applications, plus go-to-market options for premium and cost-sensitive segments.

- M&A and partnership screen identifying targets by capability, geography and synergy potential—supported by valuation heuristics and integration checklists.

To preserve the value of our primary research and models, this briefing intentionally withholds the granular region-by-region and application-by-application tables, price curves and supplier-level revenue shares. Those detailed exhibits are available in the full report package and accompanying data workbook.

Priority actions for 2026

- Stress-test your BOM and supply base against a 15% manganese supply contraction and 25% commodity-price shock. Move critical long-lead items to contracted coverage where margins permit.

- Initiate a material-substitution pilot for high-cost chemistries and evaluate qualification timelines—particularly where Ni-Zn alternatives can deliver acceptable performance at lower supply risk.

- Negotiate multi-year, indexed contracts with select suppliers that include volume flexibility, quality clauses and expedited capacity access to protect against episodic demand spikes.

- Prioritize product modularization—standardize on a limited set of core geometries and materials to amplify scale and reduce SKU proliferation across global manufacturing sites.

- Pursue targeted partnerships or bolt-on acquisitions to secure feedstock access or specialized process capability rather than attempting broad-based, capital-intensive vertical integration immediately.

How to use this briefing and next steps

This preview is designed to align executive teams around the market logic and immediate operational priorities for 2026. For procurement leaders, the full dataset enables contract-level negotiation scenarios. For R&D and product teams, the report’s TCO and qualification models provide the evidence base to revisit component choices. For corporate development teams, our M&A screens and valuation heuristics identify pragmatic targets for consolidation or capability extension.

PW Consulting’s full Soft Ferrite Core Market report includes the proprietary models, supplier scorecards and the segment-level intelligence that underpin these strategic recommendations. If your 2026 planning process requires rapid, defensible inputs—capex timing, supplier strategy or M&A origination—this is the study designed to be used directly in board-level decision packs.

For access to the full dataset, proprietary spreadsheets and supplier matrices, please refer to the PW Consulting report page. Our team is available to run bespoke scenario workshops and to tailor the models to your product portfolio and procurement profile.

Prepared by PW Consulting — Senior Strategy & Industry Analysis. This briefing is intended to accelerate high-confidence decisions entering 2026 while preserving the full analytic depth for licensed users of the complete study.

For detailed analysis of this topic, please visit the official page:Soft Ferrite Core Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com