Electronic Components Market 2026: Strategic Imperatives for Boardrooms and Product Teams

Introduction

As complexity in electronics design, supply chains and regulation accelerates, 2026 will be a decisive year for firms that supply, design with, or buy electronic components. PW Consulting's latest Electronic Components Market study—based on a 2025 base year and a 2026–2032 forecast horizon—translates market-scale momentum, supplier dynamics and regulatory shock scenarios into practical playbooks for executives. The market we modelled grew from roughly USD 300 billion in 2020 to about USD 438.5 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 7.36% through the 2026–2032 forecast window, reaching about USD 717.6 billion by 2032. Those headline numbers matter, but the real strategic value lies in the granular, executable guidance the report provides for 2026 planning cycles.

Electronic Components Market

Market at a Glance — A Strategic Snapshot

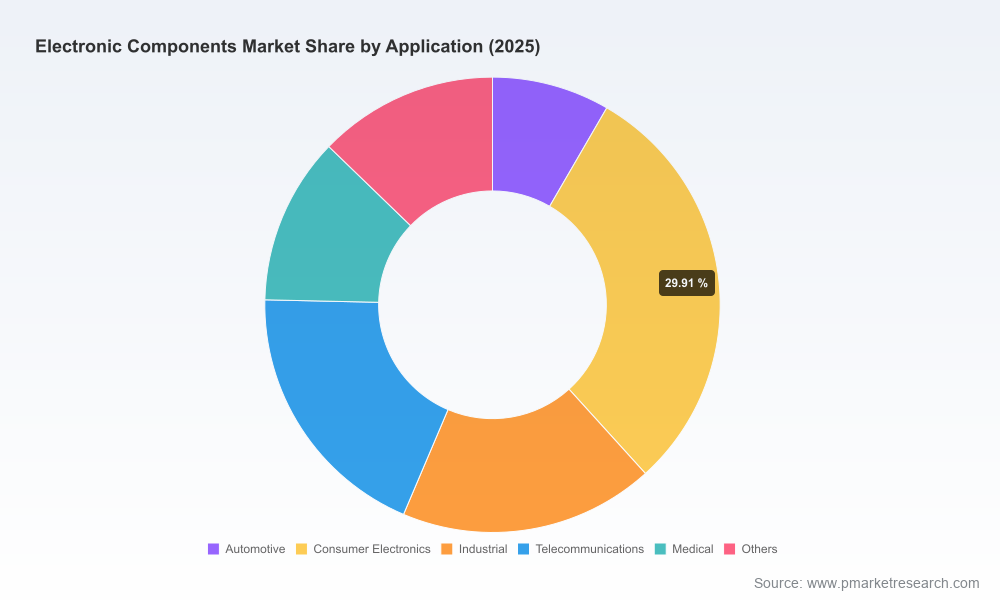

Aggregate expansion at a mid-single-digit to high-single-digit CAGR signals sustained demand across automotive electrification, industrial digitization, 5G and edge computing, and a resurgent consumer-electronics cycle. However, headline growth masks structural shifts—supplier specialization, pockets of concentration, and episodic supply stress—that will determine winners and losers in the next 18–24 months.

Electronic Components Market

- Scale and concentration: the market exhibits a mix of global leaders and a long tail of specialized suppliers; the top three firms account for a meaningful minority of industry revenue and the top five extend that share, highlighting both the importance of scale and the opportunities for niche players.

- Capital intensity and capacity: power semiconductors, wide-bandgap materials and advanced packaging are driving capital investment decisions—and where capacity is added, strategic partnerships and site selection will control access to supply.

- Supply chain friction: lead-time volatility, memory tightness, and regional capability imbalances are already influencing sourcing and design-for-supply decisions.

Why This Report Matters for 2026 Decision-Making

Executives using this research in 2026 will be able to convert market signals into concrete actions across four decision horizons:

Electronic Components Market

- Near-term procurement and inventory (0–6 months): prioritize capacity commitments, re-evaluate safety stock using supplier-specific lead-time scenarios, and deploy targeted hedges on critical raw materials and components.

- Product roadmaps (6–18 months): accelerate design wins where supplier roadmaps align with your product needs (e.g., SiC/GaN power devices, secure MCUs), and defer or redesign features that depend on fragile supply positions.

- Strategic sourcing and partnerships (12–36 months): identify candidate partners for co-investment or strategic long-term contracts to lock in capacity and preferential supply terms.

- M&A and investment (18+ months): use our value-at-risk and upside casework to prioritize M&A targets and inorganic options that shore up weaknesses in power, connectivity or distribution coverage.

What the Report Delivers (Practical, Executable Content)

PW Consulting’s study is designed for operators and strategists, not just market watchers. Key deliverables include:

- Top-line and bottom-up forecasts anchored to component families and demand drivers, reconciled across historical 2020–2025 data and 2026–2032 scenarios.

- Three scenario pathways (base, upside, stress) that quantify the impact of supply disruptions, raw material inflation and rapid technology adoption on revenues, margins and time-to-market.

- Supplier scorecards—covering capacity, lead times, technology roadmap, financial strength and ESG exposure—that enable prioritized supplier engagement.

- Supply-chain stress tests and playbooks for alternative sourcing, qualification timelines and accelerated validation for critical components.

- Regulatory and cost-intelligence modules, including CBAM exposure mapping and carbon-cost sensitivities for production footprints in 2026–2028.

- M&A screening filters, integration checklists and valuation sensitivity tables tailored to component subsectors and distributor models.

- Board-ready one-page summaries and an executive workshop kit to convert insights into a 90-day action plan.

Competitive Landscape — Strategic Profiles and Implications

The market is populated by diversified semiconductor leaders, specialized component manufacturers, and global distributors. Rather than a static ranking, our analysis assesses strategic positioning, margin levers and vulnerability to the dynamics above. Highlights:

- Analog and mixed-signal leaders (e.g., Texas Instruments, Analog Devices, Microchip) retain strong position power through broad product portfolios and entrenched design wins. Their scale gives negotiating leverage on capacity and materials, but they must continuously innovate to defend industrial and automotive design-ins.

- Power and automotive specialists (e.g., Infineon, STMicroelectronics, NXP, Renesas, ON Semiconductor) are benefiting from EV and industrial electrification demand. Investments in SiC/GaN and new fabs are a core strategic axis; recent plant openings and event participation signal accelerated capacity plays and ecosystem partnerships.

- Passive and discrete incumbents (e.g., Murata, TDK, Vishay, Panasonic) are tightening margins through vertical integration and material sourcing strategies. Their stability in consumer and industrial BOMs makes them natural partners in cross-supply agreements for customers looking to minimize qualification churn.

- Interconnect and protection specialists (e.g., Amphenol, TE Connectivity, Littelfuse) are playing to higher-system-value roles as functional integration increases in automotive and industrial systems.

- Distribution and supply-chain service leaders (e.g., Mouser, Arrow, Digi-Key, Avnet, Future Electronics and regional distributors) are evolving beyond logistics into product-introduction and design-support services. Their expanding catalogs and digital capabilities reduce friction for OEMs but also shift margin pools.

Market concentration metrics in the study show meaningful scale at the top, yet enough fragmentation to make strategic M&A, targeted partnerships and supply exclusives compelling levers for near-term advantage.

Recent Developments Illustrating 2026 Momentum

- Strategic partnerships and capacity moves—examples include new manufacturing alliances and plant openings that alter access to power-device capacity and regional supply stability.

- Catalog and distribution expansion—major distributors added thousands of new parts early in 2026, expanding design choices but also increasing complexity for qualification and inventory management.

- Industry events and product announcements—leading suppliers are showcasing advanced security and power solutions that influence platform design choices and supplier selection in 2026 RFPs.

Market Dynamics and Risk Factors

Several cross-cutting dynamics will influence strategic choices next year:

- Raw material and capacity mismatch: memory production and other upstream materials continue to show supply-demand imbalances, influencing pricing and lead times across assemblies.

- Lead-time volatility: certain automotive-grade MCUs and specialty parts are exhibiting extended lead times that can exceed typical program buffers—necessitating proactive qualification and multi-sourcing strategies.

- Regulatory pressure: carbon pricing mechanisms and border-adjustment regimes are adding a new cost dimension to footprint decisions; manufacturing location choices now carry measurable cashflow implications.

- Geopolitical concentration: critical advanced semiconductor manufacturing remains regionally concentrated, making localization strategies and risk diversification central to resilient planning.

How to Use This Research in Your 2026 Planning Cycle

Translate insights into action with a short implementation checklist:

- Rebaseline your 2026 demand plan using the report’s scenario outputs and supplier-specific lead-time profiles.

- Prioritize supplier engagements: use our scorecards to select partners for capacity commitments, dual-sourcing trials, or co-investments.

- Run a rapid design-for-supply audit to identify features most exposed to single-supplier or long-lead components and produce mitigation roadmaps.

- Embed regulatory cost projections into your product-cost models and capital plans—include carbon-cost pass-through scenarios where relevant.

- Use the M&A filters to identify bolt-on acquisitions that accelerate capability in power, connectivity, or distribution reach.

Final Note — The Research as a Decision Catalyst

PW Consulting’s Electronic Components Market study is built to be operational: it converts macro growth (from about USD 300 billion in 2020 to roughly USD 438.5 billion in 2025 and a modeled path to approximately USD 717.6 billion by 2032 at a 7.36% CAGR) into supplier-level actions, risk mitigations and value-capture initiatives for 2026. We intentionally keep certain segment-level detail reserved for the full report to preserve the strategic advantage of subscribers; the summary here demonstrates our analytical depth while inviting the targeted, hands-on tools and datasets needed to implement the recommendations.

Next Steps

To convert the insights above into a tailored 90-day plan—complete with supplier-target lists, capex scenarios and inventory optimization models—access the full report and accompanying workshop materials. For decision teams preparing 2026 budgets, product roadmaps and sourcing strategies, the time to act is now: the market trajectory is clear, but the levers that capture value are specific, and they are actionable today.

For detailed analysis of this topic, please visit the official page:Electronic Components Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com