NAPLAN Test Papers: A Valuable Resource for Academic Success

Other |

2026-06-04 15:09:19

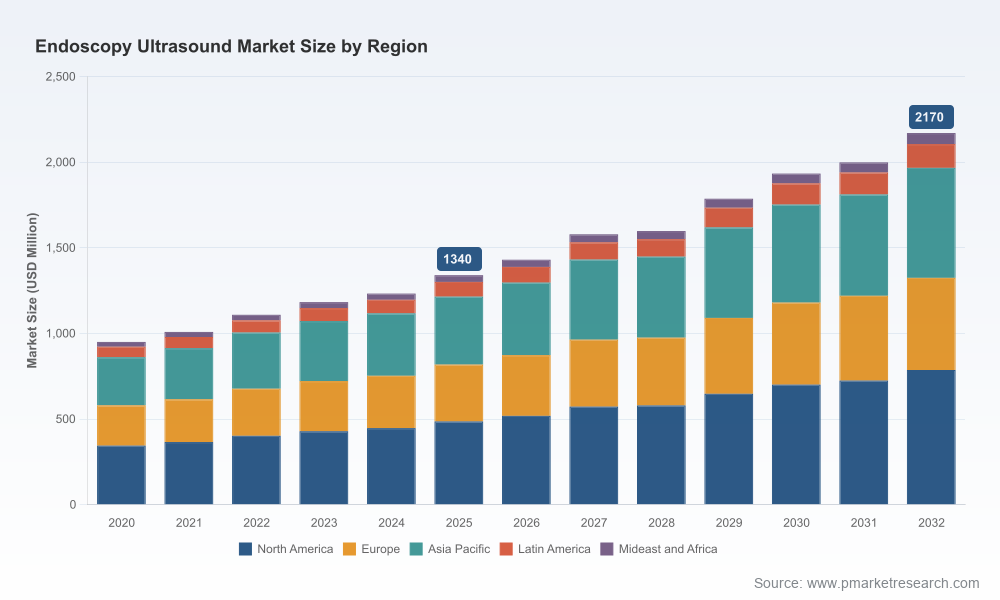

As healthcare systems shift toward minimally invasive diagnostics and targeted therapeutics, endoscopy ultrasound (EUS) has moved from a niche procedural adjunct to a strategic platform for gastrointestinal and oncologic care. PW Consulting’s new market study, with a 2025 base year and a 2026–2032 forecast horizon, quantifies this transition: the global EUS market expanded from roughly USD 950 million in 2020 to about USD 1.34 billion in 2025, and our model projects continued expansion at a compounded annual growth rate of approximately 7.1% through the forecast window, approaching the low‑to‑mid USD 2 billion range by 2032. For executives planning investments, commercial launches, or M&A in 2026, these macro dynamics create both urgency and opportunity.

Endoscopy Ultrasound Market

Timing of investment: With the market on a multi‑year growth trajectory, decisions made in 2026 determine whether a firm captures high‑growth share in the next product cycle or lags behind platform incumbents.

Endoscopy Ultrasound Market

Portfolio prioritization: EUS sits at the intersection of capital equipment, disposables (needles, probes), software (image processors, AI), and recurring service revenue (reprocessing, maintenance). Our study helps quantify where to prioritize R&D and commercial resources.

Endoscopy Ultrasound Market

Regulatory and reimbursement alignment: FDA 510(k) clearance paths and outpatient CPT reimbursement variability materially affect time‑to‑market and pricing strategy. The report maps these levers for prioritized geographies and device classes.

M&A and partnership scouting: As platform and consumable economics diverge, targeted acquisitions (to secure needle technology, ultrasound processors, or sterilization capabilities) can deliver outsized returns in a consolidating landscape.

Proprietary market model (2020–2032): scenario‑based top‑down and bottom‑up sizing with sensitivity to adoption curves, reimbursement shifts, and pricing dynamics. The model is delivered as a downloadable workbook so teams can run their own scenarios.

Demand‑driver deep dive: clinical guidelines, population health trends, oncology and GI procedural volumes, and the economics of diagnostic vs therapeutic EUS use cases.

Go‑to‑market playbooks: commercialization sequencing, distributor vs direct strategies, bundling of capital and consumables, and clinical evidence roadmaps to accelerate adoption.

Regulatory & reimbursement pathway maps: device classification, typical 510(k) timelines, coding permutations, and payer negotiation templates for outpatient and inpatient settings.

Cost & margin models: bill‑of‑materials drivers (including critical inputs such as medical‑grade nitinol for needles), manufacturing scale levers, and service economics for reprocessing and sterilization.

Competitive intelligence packs: discreet profiles and strategic assessments of the leading incumbents, challenger technologies, and fast‑emerging players in China and other growth markets.

M&A heatmaps & screening tool: compatibility scoring by technology, geography, regulatory posture, and commercial fit to prioritize targets.

Risk register and mitigation playbook: supply chain vulnerabilities, pricing pressure, regulatory delays, and clinical trial execution risks with recommended mitigations.

Note: the public preview intentionally omits the granular segment breakouts and region-by‑region revenue tables that appear in the full report—these are preserved for subscribers and purchasers to protect actionable intelligence and to support direct commercial planning.

The EUS ecosystem is populated by a mix of large platform providers, specialists in disposables, and innovative challengers that convert existing endoscope installed bases into full EUS capability. Market concentration metrics indicate a meaningful incumbent presence at the top, with a mid‑range level of consolidation among the leaders. This structural mix shapes strategic options for entrants and incumbents alike.

Olympus Corporation — platform leader: Olympus maintains a vertically integrated EUS portfolio spanning processors, echoendoscopes, needles, and advanced imaging systems. Recent product introductions and trade show activity in 2026 emphasize imaging upgrades and clinical workflow. Strategic imperative: protect installed base while accelerating attach rate for consumables and services.

FUJIFILM — imaging differentiation: Fujifilm’s recent processor and linear scope launches signal a move to high‑resolution imaging as a key competitive differentiator. Strategic imperative: leverage image quality to win diagnostic share and build clinical evidence.

Boston Scientific & Medtronic — interventional focus: Both players emphasize EUS‑guided biopsy systems and interventional toolkits, targeting therapeutic adoption beyond diagnostic use. Strategic imperative: convert diagnostic procedures into higher‑value interventional workflows.

Pentax Medical, ConMed, Cook Medical — specialist device players: These firms supply scopes, needles, stents, and accessories with strong ties to proceduralists. Strategic imperative: deepen clinician relationships and focus on single‑use vs reusable economics that align with hospital procurement priorities.

EndoSound and regional OEMs (e.g., SonoScape, HUACO) — disruption and access plays: Startups offering retrofit systems or lower‑cost platforms can accelerate adoption in cost‑sensitive markets and create new competitive pressure. Strategic imperative: incumbents must balance ASP protection with share defense in fast‑growing geographies.

Steris and service providers — aftercare & compliance: Reprocessing, sterilization validation, and infection‑prevention services represent a recurring revenue pool and a compliance differentiator. Strategic imperative: bundle services to increase switching costs.

Attach economics: Consumables and service revenue materially expand lifetime value per installed platform. Firms that optimize disposable design and lock in service contracts can improve gross margins and predictability.

Reimbursement and regulatory friction: Differences in outpatient coding and Medicare payment levels create meaningful variability in procedure economics. Additionally, new device introductions follow 510(k) pathways that require documented equivalence or new clinical evidence—affecting launch sequencing and OPEX spend.

Material and labor input costs: Medical‑grade materials (e.g., nitinol for biopsy needles) and the need for certified clinical application specialists to drive on‑site adoption can create cost and capacity constraints; these should be modeled into go‑to‑market timelines.

Consolidation risk and strategic clustering: Our concentration analysis shows a market where a handful of players control a majority of volume, while a second tier competes on price or niche innovation—this shapes M&A valuation dynamics and required scale to compete.

Set a platform‑first strategy: Decide whether to compete on imaging/processor leadership, disposable economics, or integrated service models and align R&D and commercial incentives accordingly.

Accelerate clinical evidence generation: Focus on comparative studies and health‑economic models that demonstrate diagnostic yield, procedure time savings, and downstream care pathway benefits to secure payer support.

De‑risk supply chains: Secure long‑lead components (e.g., ultrasonic transducer elements and nitinol supply), and build dual sourcing or near‑shoring options to prevent launch delays.

Monetize services: Expand sterilization, reprocessing validation, and application‑specialist programs to build recurring revenue and increase switching costs.

Pursue targeted M&A: Use our screening tool to identify bolt‑on acquisitions that accelerate access to consumables, regional distribution networks, or disruptive retrofit technologies.

Localize reimbursement strategies: Tailor payer engagement plans by market segment to manage price realization and optimize procedure coding adoption.

Subscribe to the full report to obtain the granular segmentations, regional demand layer, unit economics by device class, and the interactive model that executives and corporate development teams use for bid‑decisioning and post‑merger integration planning. The complete package contains slide decks, the financial model, competitive intelligence dossiers, and a prioritized list of commercial pilot sites that will be critical for executing a 2026 market‑entry or scale strategy.

In an environment where imaging quality, interventional capability, and consumable economics are converging, firms that build coherent platform strategies and use data‑driven scenario planning will be best positioned to convert market growth into durable competitive advantage. PW Consulting’s EUS study provides the strategic foundation to make those choices with confidence.

For detailed analysis of this topic, please visit the official page:Endoscopy Ultrasound Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com