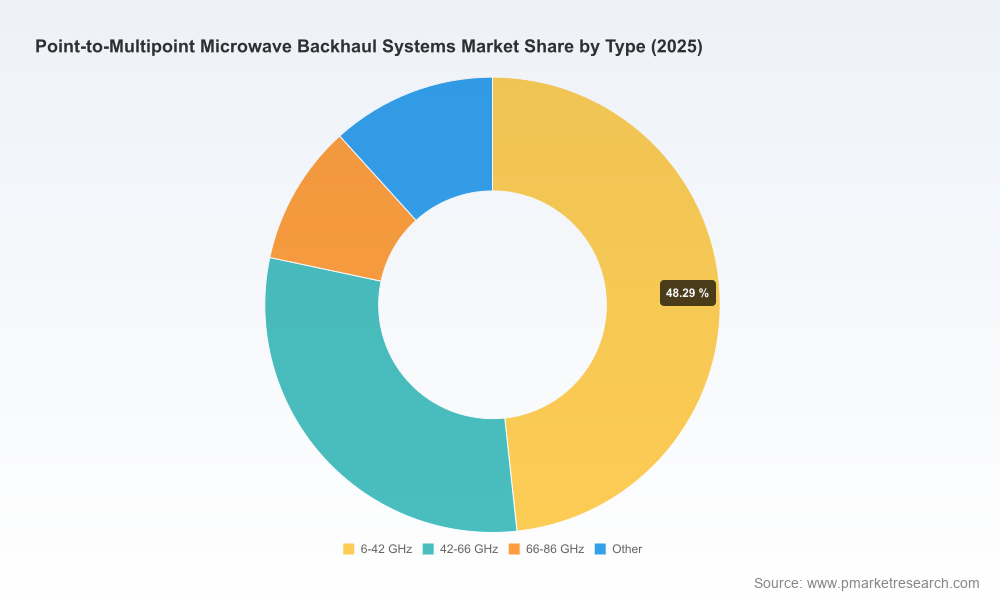

Point-to-Multipoint Microwave Backhaul Systems Market — Strategic Preview for 2026 Decision-Makers

PW Consulting presents a strategic primer on the Point-to-Multipoint (PtMP) Microwave Backhaul Systems market designed to orient executive decision-making in 2026. This preview synthesizes the macro trajectory, competitive dynamics, regulatory inflection points and actionable implications for network architects, procurement leads and corporate strategists. It demonstrates the analytic depth and operational relevance of our full market study while withholding the granular subsegment matrices that remain available in the comprehensive report.

Point-to-Multipoint Microwave Backhaul Systems Market

Why this market matters in 2026

PtMP microwave backhaul has re-emerged as a core enabler for both carrier 5G densification and enterprise fixed-wireless access strategies. After a measured recovery and modernization cycle between 2020 and 2025, the addressable global market expanded from USD 143.0 Million in 2020 to USD 187.0 Million in 2025 (base year). The market enters the 2026–2032 forecast window with momentum: our scenario-driven projection anticipates growth to approximately USD 277.0 Million by 2032, reflecting a compound annual growth rate (CAGR) of 5.8% over the forecast period.

Point-to-Multipoint Microwave Backhaul Systems Market

These headline figures understate the structural importance of PtMP architectures. They are cost-efficient for multi-site aggregation, uniquely suited for small-cell and suburban densification, and increasingly tactical for enterprises seeking resilient campus and municipal connectivity. In short, PtMP is a tactical lever for operators and large enterprise network owners to manage capex and accelerate time-to-service while maintaining reasonable spectral efficiency.

Point-to-Multipoint Microwave Backhaul Systems Market

Market structure and competitive concentration

The ecosystem blends global telecom OEMs with specialist PtMP vendors and fixed-wireless system integrators. Market concentration is material: the top three vendors account for a significant share of industry revenues, and the top five command an even larger portion, reflecting scale advantages in product portfolios, installation ecosystem and global support capabilities. This concentration creates a dual opportunity — incumbents can protect margin through integrated hardware/software suites while challengers can carve niches by optimizing cost, speed of deployment, or spectrum-specific solutions.

- CR3: Strong concentration among the few largest suppliers (indicative of scale-led purchasing patterns).

- CR5: A higher cumulative share that underscores the value of differentiated channel and service models for smaller vendors.

Technology, regulation and demand drivers

Three converging forces push PtMP adoption in 2026:

- 5G densification and mmWave economics — Small cells and urban densification require aggregation solutions that are cheaper and faster to install than fiber in many scenarios. MmWave and E‑band radios provide multi-gigabit capacity where fiber is constrained.

- Regulatory enablement — Recent regulatory moves in key markets have clarified spectrum availability and licensing pathways for PtMP deployments. Notable examples include national recommendations to prioritize microwave backhaul in specific licensed bands and international standards bodies enabling dynamic spectrum access. These developments materially reduce deployment regulatory risk and open new regional markets to PtMP solutions.

- Enterprise digitization — Municipal, utility and industrial campuses increasingly demand resilient last-mile and middle-mile alternatives. PtMP systems are attractive for rapid rollouts, disaster recovery planning and hybrid fiber-wireless architectures.

Competitive landscape — what to watch

The supplier universe can be read as a set of strategic plays rather than a list of products. Our full report contains vendor scorecards, capability heatmaps and go-to-market diagnostics. Highlights from our high-level competitive assessment:

- Cambium Networks (United States) — Positioned to win on flexible PtMP platforms that scale across licensed and unlicensed bands. Their strategy favors rapid deployment and cost-efficiency for both urban small-cell and rural aggregation.

- Ceragon Networks / Siklu (Israel) — Focused on mmWave PtMP for dense urban 5G backhaul; strong in scenarios requiring high spectral reuse and compact antenna form-factors.

- Huawei Technologies (China) — Introduces multi-band simultaneous transmission from hub-site antennas, targeting high-aggregation sites and dense backhaul topologies.

- Ericsson and Nokia (Sweden / Finland) — Legacy microwave portfolios adapted for 5G: high-capacity licensed PtMP solutions with enterprise-grade management and integration into existing RAN/core portfolios.

- ZTE, Radwin, Airspan, Proxim, Mimosa, DragonWave‑X, Trango and Exalt — A mix of focused and diversified players offering differentiated propositions around price-performance, packet microwave features, and service/installation models.

Recent vendor moves reinforce strategic patterns: Huawei’s 2025 multi-band PtMP launch targets hub-site consolidation; Cambium’s mid‑2025 multi-gigabit platform is aimed at reducing TCO for mixed urban/rural rollouts; and Ericsson’s partnership activity shows operators prioritizing capacity upgrades across emerging markets.

Key commercial and technical trade-offs for 2026 procurement

Decision makers must navigate five core trade-offs when evaluating PtMP options:

- Spectrum strategy vs equipment cost — Licensed bands offer reliability and predictable interference profiles; unlicensed bands reduce recurring fees but can require more engineering effort. Regulatory clarity (and the emergence of dynamic access frameworks) is steadily lowering uncertainty but does not remove the trade-off.

- Centralized hub vs distributed aggregation — Hub-centric PtMP can lower per-subscriber cost; distributed models improve resilience and offer graceful degradation strategies.

- Hardware vs software-defined features — Investment in platforms that support packet microwave, edge routing and virtualized functions can increase upfront cost but reduce lifecycle OPEX.

- Vendor lock-in vs integration agility — Large OEMs provide bundled services and global support; specialists often offer faster deployments and attractive pricing for targeted use cases.

- Capex vs time-to-market — The most attractive PtMP propositions in 2026 are those that balance modest capex with rapid deployment and predictable operations costs.

Practical playbook — immediate actions for 2026

For operators and enterprise IT leaders preparing procurement decisions this year, our research recommends a focused, staged approach:

- Prioritize pilots that validate spectrum, antenna geometry and throughput in representative urban and suburban cells. Use short-term trials to stress vendor integration and lifecycle tooling.

- Develop a spectrum access strategy that layers licensed, lightly licensed and E‑band allocations, anticipating regulatory moves supporting dynamic spectrum access.

- Create an objective vendor selection rubric that weights total cost of ownership, integration with existing transport (MPLS/IP, timing synchronization requirements) and field-service footprint.

- Insist on measurable SLAs and a clear upgrade path to multi-gigabit capacity as network usage evolves. Verify vendor roadmaps against expected 5G small-cell densification timelines.

- Use scenario-based financial models (included in the full report) to stress-test payback under differing fiber availability, capex discount rates and subscription growth.

Risks and mitigants

Three risk clusters merit attention in 2026:

- Regulatory shifts — While many regulators now enable PtMP-friendly spectrum policies, fragmented regional rules can complicate cross-border rollouts. Mitigation: adopt a modular equipment spec and regulatory playbook per jurisdiction.

- Interference and capacity planning — Rising unlicensed usage can impact performance if not proactively engineered. Mitigation: combine spectrum monitoring with adaptive modulation and active interference avoidance.

- Vendor concentration and supply risk — The market’s concentration creates single‑supplier exposure for large projects. Mitigation: build multi-vendor testbeds and negotiate robust service and spares provisions.

What the full PW Consulting report delivers

This executive preview is a gateway to a comprehensive toolkit that supports 2026 strategic decisions. The full Point-to-Multipoint Microwave Backhaul Systems Market report (base year 2025; historical window 2020–2025; forecast 2026–2032) contains:

- Detailed market-sizing and multi-scenario forecasts for the forecast period, including revenue curves, CAGR sensitivities and upside/downside scenarios.

- Granular segmentation by geography, frequency bands and end‑use applications (note: this preview intentionally omits those line-item figures to preserve actionable exclusivity).

- Vendor scorecards, pricing trend models, and procurement negotiation templates.

- Regulatory matrix and regional deployment playbooks aligned with ETSI/FCC/TRAI developments.

- Implementation and operational checklists: rollout sequencing, RF planning templates, and O&M staffing models.

- Scenario-based TCO and ROI models you can adapt to project-level inputs.

How to use this intelligence

Use the insights in this primer to align executive sponsorship, prioritize pilots, and structure RFPs for late‑2026 procurement cycles. The macro numbers — market growth from USD 143.0 Million in 2020 to USD 187.0 Million in 2025, with a projected rise toward USD 277.0 Million by 2032 at a 5.8% CAGR for 2026–2032 — frame the commercial opportunity. However, profitable execution depends on the granular choices: spectrum mix, vendor selection, integration architecture and regulatory compliance. Those details, and the decision-support assets required to operationalize them, are compiled in the full PW Consulting study.

Next steps

Clients seeking to convert this strategic context into procurement-ready decisions should engage PW Consulting for a tailored workshop. We will overlay your network footprint, service priorities and regulatory jurisdictions on our market model and deliver prioritized vendor shortlists, pilot designs and financial casebooks calibrated to your tolerance for capex and timeline for service activation.

For access to the full dataset, vendor scorecards and deployment playbooks referenced in this briefing, request the complete report and supporting annexes from PW Consulting. Our research is structured to be immediately actionable for 2026 rollouts while supporting multi-year strategic planning through 2032.

For detailed analysis of this topic, please visit the official page:Point-to-Multipoint Microwave Backhaul Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com