Pharmaceutical CRO Market Growth in Genomics-Based Research Services

Other |

2026-05-04 06:17:08

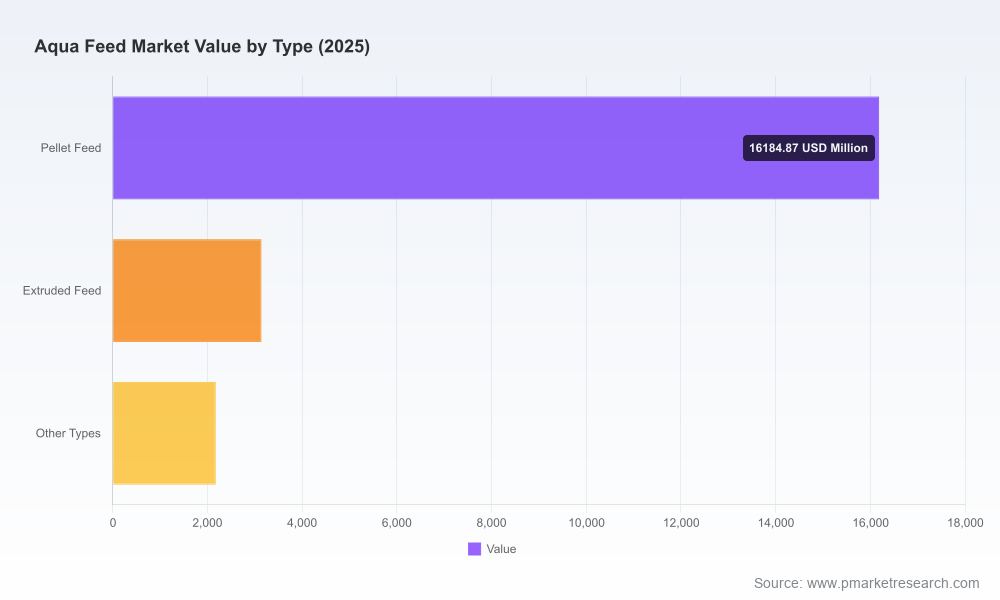

Between 2020 and 2025 the global aqua feed market moved from roughly USD 16.3 billion to USD 21.5 billion, reflecting accelerating commercialisation and shifting supply chains across aquaculture value chains. Our projection framework—built on a 6.98% compound annual growth rate—shows continued expansion through the 2026–2032 forecast window, with clear inflection points driven by regulation, ingredient volatility, and targeted capacity additions. For senior executives and investment committees planning actions in 2026, this study is designed to convert macro momentum into concrete strategic options while flagging the tactical traps that commonly undermine growth plans.

Aqua Feed Market

Regulatory timing is now business‑critical. New standards and country rules that became effective in late 2025 and early 2026 are already reshaping sourcing, labelling and supplier qualification requirements. Companies without rapid compliance pathways face market exclusion or costly reformulations.

Aqua Feed Market

Input cost volatility has migrated from episodic to structural. A short supply shock in 2025 pushed key protein inputs sharply higher; manufacturers that react with formula agility, contractual hedges, and ingredient innovation will preserve margins.

Aqua Feed Market

Capacity additions are not evenly distributed. New mills and brown‑field expansions are concentrating where local demand and policy support intersect—creating both price pressure in some corridors and opportunity gaps in others.

Product differentiation is accelerating. Leading companies pair nutrition science with sustainability credentials and digital traceability as minimum entry criteria for premium channels.

Demand and supply scenario models (2026–2032) with species‑level drivers, sensitivity to feed conversion improvements, and upside/downside scenarios keyed to ingredient price paths.

Ingredient cost‑build templates you can drop into your financial models—covering fishmeal, soy, alternative proteins, oils and enzyme/premix costs—updated to include 2025 shocks and 2026 rule changes.

Regulatory risk matrix mapping major certification and national requirements, compliance pathways, expected timelines and cost buckets for feed mills and formulators.

Competitive playbook: positioning maps, capability scorecards and likely strategic trajectories for the top industrial players and fast‑growing regional champions—useful for benchmarking and M&A screening.

Go‑to‑market blueprints for premium and cost‑leadership approaches, including channel economics, co‑op models with integrators, and strategic procurement checklists.

Transaction support tools: target shortlists by capability and geography, valuation multiples bench‑marked to feed asset peers, and integration risk checklists for bolt‑on acquisitions.

Standards as a market gatekeeper. The roll‑out of tightened feed standards late in 2025 has moved from guidance to enforcement in early 2026. Certified feed mills with documented sustainable sourcing and traceability now access premium channels and certain tender pipelines. For players that depend on untreated commodity supply chains, certification timelines are now a near‑term investment question rather than a nice‑to‑have.

Ingredient scarcity and substitution pressure. The 2025 fishmeal supply squeeze pushed spot prices higher and renewed focus on alternative proteins, enzyme use, and formula reformulation. Producers that already invested in phytase and enhanced digestibility strategies are better positioned to protect margin and meet low‑phosphorus limits where those are regulated.

Selective capacity growth. Several strategic expansions and new plants opened across emerging aquaculture geographies in 2024–2025. These facilities are lowering logistics costs for local farmers and shifting competitive dynamics—creating pressure on imports into those regions while opening acquisition opportunities for players seeking local scale.

Product innovation as a frontline battleground. Manufacturers are launching functional feeds that combine health, resilience and growth optimisation with sustainability claims. These new SKUs command premium pricing only when backed by demonstrable field performance and credible third‑party validation.

Consolidation vs. fragmentation. The market shows low to moderate concentration: large multi‑national producers remain influential, but a long tail of regional and national players retains pricing power in local markets. This creates both buy and build pathways for scale‑seeking strategists.

Global integrators and branded feed houses. Major multinational players combine scale manufacturing, R&D and branded product portfolios to win institutional and export business. Their strengths include broad species coverage, integrated supply chains and the ability to fund multi‑year product development. For partners and challengers, competing on scale requires either a narrow, hard‑to‑replicate niche or superior cost position.

Premium specialists. Several firms have carved high‑value positions with species‑specific formulations and strong customer relationships in intensive production systems. These companies command premium margins, but their growth depends on demonstrating return‑on‑biological‑performance and expanding feed mill reach.

Volume incumbents in large domestic markets. Players with massive domestic volumes and low unit costs are resilient in price cycles. Their strategic moves—capacity expansion, raw material backward integration, and distribution reach—shape local market entry economics for new entrants.

Ingredient and technology providers. Suppliers of premixes, enzymes and processing equipment occupy an influential position. Partnerships between feed producers and technical suppliers are now the fastest route to low‑phosphorus, high‑digestibility formulations required by regulators and farmers alike.

New mandatory feed standards introduced at the end of 2025 require certified mills to demonstrate sustainable sourcing and traceability within tight implementation windows—an immediate procurement and compliance priority.

Product launches and R&D investments during 2024–2025 indicate an industry pivot toward functional feeds that address disease resilience and growth optimisation; successful launches include solutions oriented at shrimp and Mediterranean species.

Several large capacity additions were brought online in 2024–2025, and new plants opened in emerging aquaculture economies, changing local supply dynamics and lowering import dependencies in those corridors.

Industry partnerships focused on sustainable species feed are emerging as avenues to create farmable value chains for species previously marginal from an economic standpoint.

Embed certification timelines into commercial contracts and product roadmaps now. Treat feed‑standard compliance as a market entry requirement for premium channels.

Re‑engineer formulations to reduce exposure to the most volatile ingredients and accelerate adoption of enzymes and digestibility enhancers to meet low‑phosphorus and sustainability targets.

Pursue selective capacity tie‑ups—tolling, minority stakes or offtake agreements—in regions where local production is expanding to secure logistics and margin advantages.

Segment your product portfolio between cost‑competitive base feeds and premium, certified functional feeds; ensure commercial KPIs and sales incentives differentiate these routes.

Run near‑term M&A and partnership screens against capability gaps: R&D in functional nutrition, premix/reagent supply, and certified traceability platforms—these are high‑value targets with quick synergy paths.

Adopt dynamic pricing and procurement models that link feed pricing to a transparent basket of raw materials and certification premiums to preserve margin in volatile markets.

Our full Aqua Feed Market report contains the granular modules you need to act: downloadable cost‑build models, species‑level demand forecasts, country and mill‑level capacity maps, supplier scorecards and a deal pipeline of high‑priority acquisition targets with approximate valuations. We intentionally withhold the detailed segmentation tables and country‑level stacks in this preview so that clients access the complete, actionable datasets through the formal report channel—ensuring confidentiality and controlled distribution of high‑value commercial intelligence.

For strategy teams, procurement heads and investors, the 2026 decision window is short. Whether you are defending margin, pursuing premiumisation, extending into new geographies or preparing for consolidation, the core choices are the same: secure compliant supply, reduce input volatility, and align product portfolios with verifiable sustainability outcomes. Our report gives you the scenarios, the numbers and the implementation checklists to move from strategic intent to market capture within the next 12–24 months.

To access the full dataset, scenario models and company scorecards that power these recommendations, please consult the PW Consulting Aqua Feed Market report—built for executives who must translate industry momentum into measurable business outcomes in 2026.

For detailed analysis of this topic, please visit the official page:Aqua Feed Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com