CA Practice Management Software Market Forecast 2031: US Maintains the Largest Share

Other |

2026-04-13 12:12:48

As enterprise and cloud architectures evolve to support generative AI, real‑time analytics, and distributed edge services, the physical layer underpinning digital transformation—data center construction—has entered a new era of scale, specialization, and regulatory scrutiny. PW Consulting’s forthcoming Data Center Construction Market study (base year 2025; historical 2020–2025; forecast 2026–2032) synthesizes the macro trajectory and the practical, executable intelligence that executives and capital allocators need to act confidently in 2026. This preview outlines the strategic value of the full report while intentionally reserving segmented tables and granular benchmarks to the full publication.

Data Center Construction Market

The data center construction market has expanded rapidly over the past half‑decade, roughly doubling from the start of the period to a substantially larger base in 2025. Our forward view projects continued expansion through 2032, with the market approaching the mid‑hundreds of billions (USD) by the end of the forecast period and a compound annual growth rate (CAGR) of approximately 6.4% across the forecast horizon. This trajectory reflects not only hyperscale consumption but also intensifying investment by colocations, cloud providers, and enterprise digitalization programs.

Data Center Construction Market

Policy and permitting shifts are accelerating project cadence. Recent executive actions at the federal level have shortened environmental review timelines for very large loads and introduced incentives that materially change the economics and speed of development for qualifying projects. These dynamics are rapidly altering site selection calculus and permitting risk models.

Data Center Construction Market

Energy and ratepayer dynamics are becoming a first‑order risk for developers. A cross‑sector pledge by major developers to fully internalize the costs of new generation capacity introduces new contractual and financing structures; at the same time, regional capacity market behavior has produced extreme price volatility that can translate into multi‑year cost exposure for new projects.

Cost inflation is structural, not transitory. Upstream producer price pressures—particularly in chemical and materials inputs—combined with trade policy on steel, aluminum and copper, have added visible premiums to core construction inputs. Contractors and owners must adopt more sophisticated hedging, procurement timing, and design modularity to control delivered costs.

The PW Consulting study is designed as an operator’s manual for 2026 decision cycles. It moves beyond descriptive market commentary to offer actionable tools and templates that investment committees, development teams, and construction executives can deploy immediately. Key deliverables include:

Robust market sizing and trend analysis: a repeatable framework that reconciles historical activity (2020–2025) with scenario‑based forecasts to 2032, enabling sensitivity testing of demand shocks and policy changes.

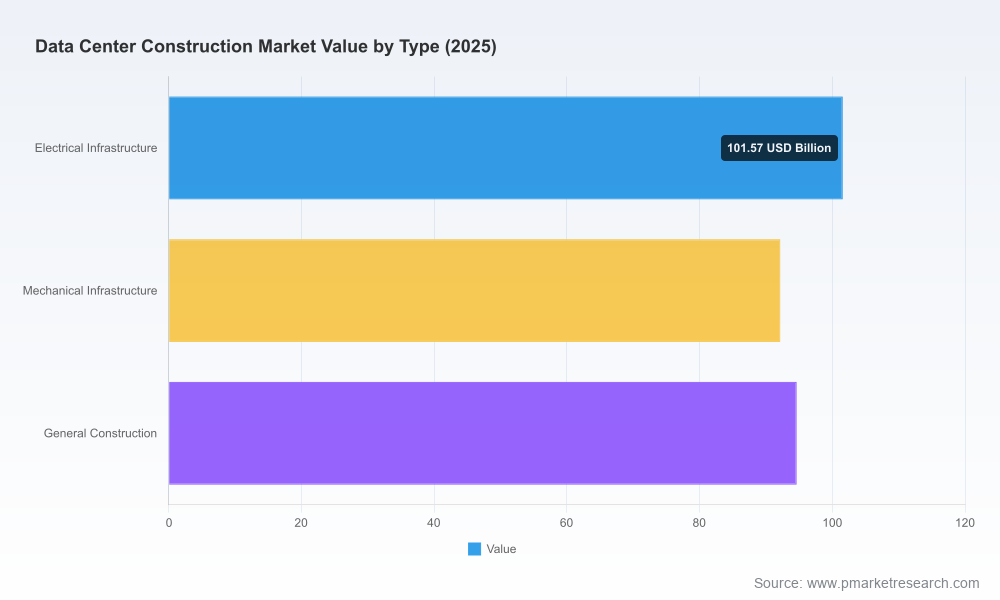

CapEx and build‑cost model: a configurable cost model that captures drivers across electrical, mechanical, and general construction domains; users can adapt inputs for local material premium, labor availability, and modular factory‑built options.

Supply‑chain risk map: vendor tiers, single‑source exposures, and lead‑time heatmaps for critical components (switchgear, chillers, power transformers, prefabricated modules), paired with mitigation playbooks.

Permitting and regulatory playbook: a decision tree informed by recent federal and state policy shifts, enabling teams to estimate permitting duration, conditional incentives, and compliance costs under alternative project structures.

Procurement and contracting templates: shifting contracting strategies (e.g., GMP vs. target cost with shared savings) matched to capital availability and developer risk appetite, including clauses for material inflation and energy‑infrastructure obligations.

Site selection and interconnection checklist: an integrated scoring tool combining grid access, capacity market exposure, resilience, and local workforce considerations that can be used during 30–60–90 day go/no‑go cycles.

Scenario playbooks for AI‑driven demand: modularization strategies, high‑density cooling alternatives, and staged campus build plans designed to preserve optionality while minimizing stranded capacity risk.

Performance benchmarking and contractor scorecards: practical KPIs and evaluation criteria for selecting construction partners and monitoring delivery against schedule, cost, and commissioning targets.

The market’s contractor ecosystem is increasingly mature and bifurcated. A group of global engineering and construction firms, alongside specialized mission‑critical builders, now account for a meaningful share of large projects while a broader base of national and regional firms competes for mid‑market and enterprise builds. Market concentration metrics indicate that the top three contractors capture a substantial share of project value, with the top five further increasing concentration—creating both risks and opportunities for owners.

Full‑service global EPCs (examples among market leaders): these firms bring integrated capabilities for hyperscale campus projects, global supply‑chain reach, and end‑to‑end delivery. Their scale supports rapid mobilization and complex financial packaging, but owners must weigh premium pricing and potential capacity constraints during peak demand cycles.

Specialist mission‑critical builders: these contractors focus on high‑density, AI‑ready facilities and advanced mechanical/electrical systems. They often excel in preconstruction value engineering and systems integration—critical skills as cooling and power designs tighten under new efficiency standards.

Modular and hybrid builders: firms with modular fabrication capabilities can compress timelines and reduce on‑site labor exposure. For owners pursuing staged expansion and lower up‑front capex, these partners deliver differentiated value.

PW Consulting’s vendor profiles synthesize firm capabilities, delivery models, regional reach, and procurement considerations—helping buyers map which partner archetype best aligns with their risk tolerance, timing needs, and capital structure.

Permitting and incentives: Recent federal directives that accelerate environmental reviews for very large loads materially reduce schedule uncertainty for qualifying projects. At the state level, a growing slate of laws now shifts some energy expansion costs onto developers, reshaping pro forma assumptions for any project with new grid interconnection needs.

Material and labor cost pressure: Industrial producer price indices and tariffs on key commodities have elevated input costs. Contractors and owners must adopt layered procurement strategies (forward purchases, index‑linked contracts, and supplier diversification) to protect margins.

Grid economics and capacity markets: In some regional markets, capacity prices have spiked due to hyperscale concentration, creating episodic cost exposures that can overwhelm previously conservative energy budgets. Developers should model regional capacity market scenarios as a standard sensitivity in any site evaluation.

Efficiency standards and decarbonization: New building energy efficiency mandates and corporate ESG commitments are accelerating investment in advanced cooling, waste‑heat recovery, and onsite/offsite low‑carbon procurement. These investments alter total cost of ownership and can unlock tax, incentive, or regulatory benefits when designed into the earliest project phases.

Reassess site and grid exposure now. With policy windows narrowing and grid costs volatile, teams should re‑prioritize site due diligence on interconnection timing and capacity market exposure during 2026 planning rounds.

Lock procurement strategies to calendar milestones. Given elevated material premiums, structured buyouts and early supplier agreements will increasingly determine delivered unit cost and schedule adherence.

Adopt modularity selectively. Modular construction reduces schedule risk and on‑site labor needs but can constrain late‑stage design flexibility. Use modular builds for predictable, repeatable deployments and bespoke builds where integration or density is a competitive differentiator.

Integrate energy‑infrastructure obligations into financial models. The recent industry pledge around generation funding and the proliferation of state rules that require developer‑borne infrastructure costs mean that power delivery risk must be baked into CapEx and financing structures.

Calibrate contractor selection to delivery priorities. Global EPCs can accelerate hyperscale campus timelines; mission‑critical specialists de‑risk commissioning for high‑density loads; hybrid models can optimize cost and speed. Use the report’s scorecards to align partner selection to project KPIs.

This study is engineered to shorten the path from strategy to execution. By combining forward‑looking market sizing, a configurable cost engine, regulatory scenario analysis, and contractor performance benchmarking, the report empowers leaders to:

Make defendable site and partner choices within compressed board cycles;

Negotiate procurement terms that reflect current material inflation and policy obligations;

Quantify upside/downside across energy and capacity market scenarios; and

Structure deals that preserve expansion optionality while protecting against stranded capacity risk.

This preview is intentionally focused on the strategic takeaways executives must consider in 2026. PW Consulting’s full Data Center Construction Market study contains the granular regional and application splits, contractor benchmarks, downloadable cost models, and the comprehensive appendices that procurement and project teams will use through bid and build phases. For teams preparing 2026 CapEx packages, site selection memoranda, or contractor RFPs, the full report provides the empirical detail and executable templates required to move from hypothesis to commitment.

PW Consulting’s analysts remain available to walk project teams through customized scenario runs, contractor selection workshops, and board‑level briefings to convert these market insights into prioritized, financed action plans.

For detailed analysis of this topic, please visit the official page:Data Center Construction Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com