Golf Equipment Market Overview: Key Drivers and Challenges

Other |

2026-03-02 09:30:23

As public policy, urbanization and corporate decarbonization converge, district heating and cooling (DHC) is moving from niche infrastructure to mainstream urban energy strategy. Our new PW Consulting Market Research—anchored on a 2025 base year and a 2026–2032 forecast horizon—shows a market that has expanded materially since 2020 and is set to continue growing at a steady mid-single-digit pace (4.5% CAGR). For commercial and industrial decision‑makers planning investments, partnerships or market entry in 2026, this study is designed to be the practical strategic playbook: it highlights where value will concentrate, how regulatory tailwinds reshape economics, which technologies are crossing the commercialization threshold, and how incumbent and new‑entrant business models are adapting to capture the upside.

District Heating and Cooling Market

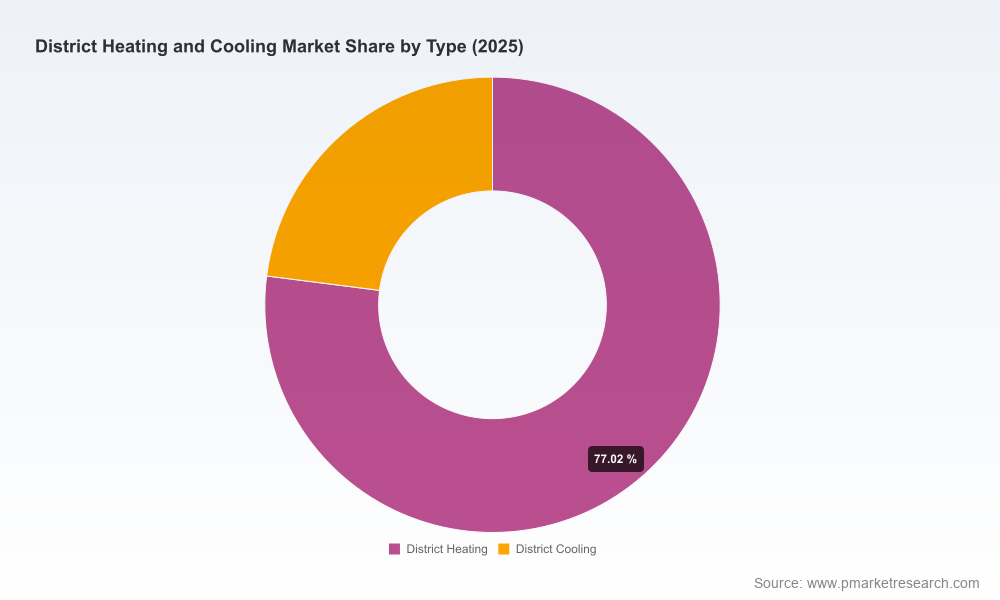

Scale and trajectory: After a clear acceleration during 2020–2025, the global DHC market in our analysis recorded a significant uplift by 2025 and is projected to extend that momentum through early 2030s. This trend reflects a combination of retrofit activity, new urban developments, and increased use of waste heat and renewables as inputs for urban thermal networks.

District Heating and Cooling Market

Policy-driven economics: Binding renewable energy targets, evolving accounting methodologies for renewable cooling, and dedicated funding windows (including competitive calls that subsidize network modernization up to high coverage levels) have materially improved project IRRs for many classes of DHC projects. Expect public procurement and concession frameworks to be central to deal structuring in 2026.

District Heating and Cooling Market

Decarbonization and corporate commitments: District networks act as enablers for rapid scope‑1 emission reductions at city and corporate campus scale. Leading operators already report measurable CO₂ avoidance attributable to network operations; for corporations seeking verifiable performance, DHC offers an operational pathway that is increasingly compatible with corporate net‑zero timetables.

Actionable market sizing and scenarios: We provide a calibrated historical series (2020–2025) and a scenario‑based forecast for 2026–2032 under alternative policy and fuel‑price assumptions. Those scenarios are designed to stress‑test investment cases, from conservative base cases to accelerated electrification/heat‑pump rollouts.

Investment and project-level modeling: The report includes modular financial models and CAPEX/OPEX benchmarks you can adapt to your geography or asset type, plus sensitivity matrices on fuel mix, carbon pricing and connection rates. These are intended to shorten diligence time and improve early‑stage decision confidence.

Procurement and contracting playbook: Practical templates and checklist‑based guidance cover concession tender design, performance‑linked payments, and mixed finance structures that combine public grants with commercial debt and project equity.

Technology and integration roadmap: From advanced substations and control valves to large heat pumps, waste‑heat capture from data centers and 5th‑generation low‑temperature networks—we map maturity, unit economics and interconnection risks, and identify technology pairings that unlock the most value in retrofit and greenfield contexts.

Policy and regulatory navigator: A concise matrix distills the most relevant regulatory levers (including pending regional strategies and funding instruments) and their likely impact on tariffs, allowable cost recovery and eligibility for renewables counting.

Competitive playbooks and M&A signal tracker: We analyze incumbent strategies, emerging fast followers, and likely M&A corridors—illustrating where horizontal consolidation, upstream equipment specialization and asset‑light operations are creating distinct opportunities.

The DHC ecosystem is characterized by a mix of equipment manufacturers, system integrators and network operators. Market concentration remains relatively low compared with other utility segments—our concentration metrics show that the top three and top five players account for modest shares—leaving ample room for regional champions and technology specialists.

Danfoss (Nordborg, Denmark) — A leading supplier of critical hardware: control valves, motorized units, heat exchangers and prefabricated substations. Danfoss plays a dual role as supplier to network operators and as an integrator in turnkey substation projects. For clients evaluating procurement, Danfoss’ strength is in component standardization that reduces on-site commissioning risk and accelerates modular deployment.

Veolia (Paris, France) — Operator and developer with deep experience across advanced generations of DHC. Veolia’s value proposition centers on scalability of operations, long-term O&M contracts and integrated decarbonization services (including geothermal and waste heat integration). In markets where public bodies prefer full-service partners, Veolia’s model often sets the bid benchmark.

Fortum (Helsinki, Finland) — Notable for industrial partnerships and waste‑heat monetization (notably data center heat recovery). Fortum also publishes clear decarbonization targets and has operationalized large heat pump plants—examples of how operators can leverage strategic anchor customers to derisk early‑stage heat recovery projects.

ENGIE (Paris, France) — A global operator with a diverse asset base and a focus on green concessions. ENGIE’s recent concession wins and partnership expansions illustrate a playbook centered on long‑duration concessions, biomass and recovered energy feedstocks, and strategic alliances with real estate and education campus owners.

Emicool (Dubai, UAE) — A regionally focused district cooling specialist that demonstrates how scale and plant‑level efficiency in hot climates can create replicable models for other fast‑growing urban markets. Emicool’s operations highlight the value of integrated plant optimization and tariff design in cooling‑dominated load profiles.

Concession and partnership deals are accelerating. A multi‑year concession award for a green district heating network that expanded distribution length and household reach signals that municipalities continue to favor long‑term private‑public partnerships to de‑risk capital expenditure and expedite decarbonization.

Strategic partnerships for campus cooling demonstrate demand aggregation’s power: operators expanding district cooling to service multiple institutional buildings at a single campus reveals a replicable pipeline approach for anchor‑tenant led expansion.

Large plant inaugurations and heat pump operations—particularly those sourcing data center waste heat—confirm a transition in feedstock economics: where access to low‑cost waste heat exists, operators can materially improve network load factors and reduce marginal carbon intensity.

Targeted grant funding and EU program windows are materially changing project bankability in eligible markets. For developers, aligning tender timelines with major grant rounds will be a near‑term differentiator.

Prioritize anchor‑tenant aggregation. Seek partnerships with data centers, hospital campuses and large multi‑building education complexes to secure high‑utilization of thermal assets from day one. Structured offtake contracts with staged connection commitments reduce ramp risk.

Design procurement around performance. Move from capex‑focused procurement to performance‑based contracting (thermal availability, seasonal COP, leak rates). This aligns suppliers’ incentives with network efficiency and simplifies public sector procurement trade‑offs.

Layer public finance and grants early in the deal. Funding mechanisms that cover high‑upfront distribution or enable partial grants for integration of renewables materially improve financial metrics—position projects to capture program windows.

Invest in modularization and standardization. Modular substations and tested skid solutions shorten construction schedules and reduce interface risk with building systems, lowering total installed cost and making project delivery more predictable.

Build regulatory intelligence as an asset. Anticipate changes from regional heating and cooling strategies and prepare tariff methodologies and carbon accounting approaches to align with evolving renewable cooling counting rules and national targets.

Balance portfolio diversification. A mix of concessioned long‑term networks, measured retrofit projects and pilot heat‑recovery deals offers a risk‑adjusted growth path—allowing operators to retain optionality as technology and policy evolve.

PW Consulting’s Market Research combines a rigorous macro forecast (historical 2020–2025 series and a 2026–2032 projection), proprietary financial models and a deal‑level tracker of recent transactions and grant awards. We combine high‑level scenario analysis with practical deliverables—tender templates, CAPEX/OPEX benchmarks, and a supplier vs operator decision matrix—so executives can move from strategy to execution without a lengthy rework of baseline assumptions.

We deliberately refrain from disclosing granular segmentation tables in this overview—our approach follows the “trailer” principle: provide depth and actionable insight on structure and strategy while reserving the full, granular datasets, regional and application splits, and downloadable models for the full report. Those datasets are what operational teams use to build financial models and to size pipelines in specific territories.

District heating and cooling is no longer a peripheral environmental program; it is an infrastructure class that will shape urban energy systems and corporate decarbonization roadmaps over the next decade. With a predictable mid‑single digit compound growth profile and multiple levers—policy support, grant windows, technology advances in heat pumps and waste heat integration—organizations that move early to adjust procurement practices, secure anchor off‑takers and standardize technical delivery will realize disproportionate first‑mover advantages.

For practitioners preparing budgets, tenders, or portfolio strategies in 2026, our full report provides the datasets, models and operational templates required to translate strategic intent into investable projects. Accessing the complete analysis will materially reduce cycle time from strategy to sanctioned project, and it will reveal the granular segmentation and asset‑level analytics necessary to prioritize capital deployment.

For detailed analysis of this topic, please visit the official page:District Heating and Cooling Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com