Floriculture Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-07-01 08:42:47

The global laminator market has moved from niche equipment to a strategically relevant component of packaging, printing, and finishing supply chains. Our base-year review (2025) captures a market that has expanded materially since 2020 and, under a medium-growth scenario, is set to continue growing through the 2026–2032 forecast window at a compounded annual growth rate of approximately 7.25%. By 2032 the industry is projected to approach roughly USD 800 million in annual revenue—enough scale to change how capital, innovation and regulation intersect across the value chain.

Laminator Market

Growth with operational friction: The combination of mid-single-digit CAGR and concentrated pockets of technology adoption creates opportunities for companies that can scale production with improved unit economics. For equipment OEMs and converters, timing investments in automation, safety redesigns, and digital services will determine which players capture disproportionate share as demand expands.

Laminator Market

Regulatory and safety as commercial levers: High-profile safety events and recalls have raised buyer expectations for compliance and traceability. Firms that embed safety certification and transparent failure-mode data into their value proposition can convert regulatory compliance into a marketable differentiation in 2026.

Laminator Market

Supply exposure and input volatility: Raw material cost swings—particularly for films, adhesives and oil-derived inputs—create margin pressure and unpredictable lead times. Strategic procurement, alternative-material roadmaps, and co-innovation with resin and adhesive suppliers will be essential to protect margins as volumes ramp.

Fragmented vendor landscape: Market concentration metrics indicate a fragmented ecosystem (top-three and top-five shares remain modest). This fragmentation favors well-executed consolidation plays, channel partnerships, or geographic specialization strategies for companies seeking to scale quickly in 2026.

Market sizing and multi-scenario forecasts — rigorous top-down and bottoms-up models spanning 2020–2032, with sensitivities linked to raw-material price trajectories and regulatory shock events.

Capital-expenditure playbooks — quantified ROIs for automation, hybrid UV/UV-LED retrofits, and energy-efficiency upgrades calibrated to 2026 input-cost assumptions.

Go-to-market and commercial models — segment-specific pricing strategies, service attach-rate benchmarks, and channel partner scoring to prioritize high-conversion routes.

Supply-chain exposure heatmaps — supplier risk scoring for films, adhesives and key mechanical components, plus mitigation scenarios including dual-sourcing and strategic inventory policies.

M&A and partnership targets — a ranked list of acquisition and JV candidates selected for strategic fit across technology, geography and customer base, accompanied by target valuation frameworks and integration checklists.

Regulatory & safety playbook — practical checklists, certification pathways and product redesign templates informed by recent recall events and global safety standards to accelerate market re-entry post-incident.

Executive dashboards and model access — interactive spreadsheets and scenario toggles to surface upside and downside outcomes for board-level decision-making.

Advisory-ready appendices — supplier scorecards, buyer negotiation scripts, and pilot implementation roadmaps for 90–180 day action plans.

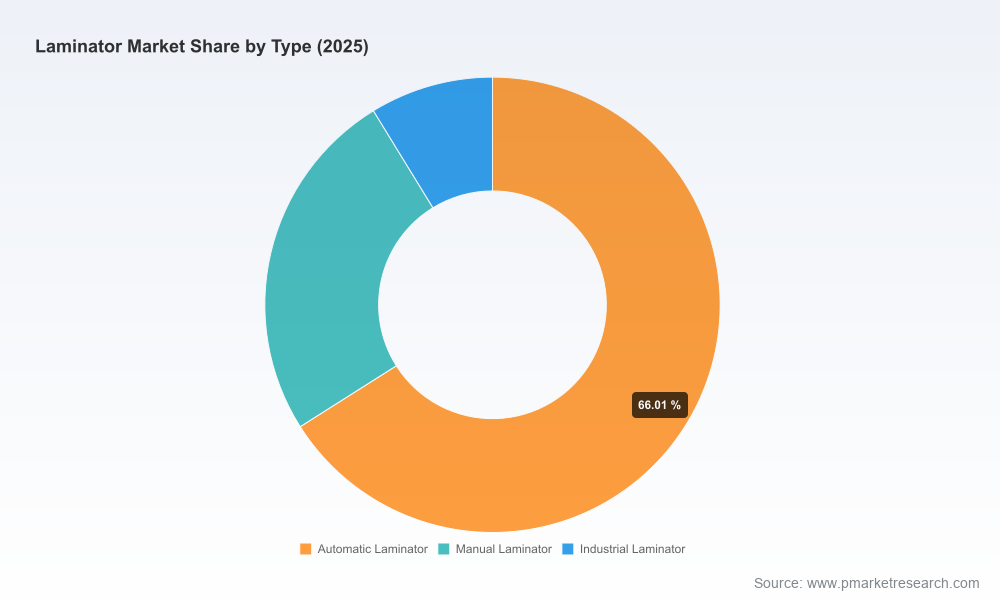

The industry combines globally recognized OEMs, regional specialists and vertically integrated packaging equipment suppliers. The competitive terrain is characterized by differentiated technology stacks (solventless, thermal, multi-technology coaters), niche product portfolios (sheet vs. roll, automatic vs. manual), and diverse go-to-market models.

GBC (United States) — well-positioned in office and light commercial thermal laminators; product lines that emphasize ease-of-use and education/SMB channels. Their brand reach in institutional channels remains a durable advantage for entry-level and replacement demand.

Autobond (United Kingdom) — focused on print-enhancement lamination and encapsulation for commercial graphics. Their reel-to-sheet and reel-to-reel systems are a play for higher-value print finishing and protective coatings.

Cellcoat Systems (United Kingdom) — specialist in thermal coating and bespoke roll-to-roll systems, serving packaging and graphic arts segments that require customization and tight process control.

Uteco Converting S.p.a. (Italy) — offers multi-technology coaters and solventless laminators for flexible packaging, often chosen for food and pharma where contamination control and regulatory traceability are critical.

Sunkia Machinery (China) — high-volume automatic thermal and roll-to-roll systems with international certifications; their patentled multi-function platforms support rapid deployment in international lines where certifications matter.

Lamina System AB (Sweden) — niche in sheet-to-sheet laminating and gluing machines, targeting printing, corrugated and folding carton customers where registration and accuracy are primary purchasing criteria.

Wenzhou Guowei & Wenzhou Feihua (China) — integrated solutions players providing gravure printing + laminating + slitting lines and automatic laminators with UV options; appeal to converters wanting end-to-end packaging lines.

Chongqing Sinstar (China) — solventless laminators for flexible packaging with upgraded SUPLOCK features; a regional contender for converters focused on solventless, food-safe laminations.

Safety and compliance shocks: A notable thermal-laminator recall late in 2025 has already prompted procurement and testing cycles among major institutional buyers. Expect accelerated vendor audits and higher specifications around thermal management and electrical safety in 2026 RFPs.

Product innovation: New industrial laminators with UV/UV-LED curing and multi-substrate capabilities are entering the market—enablers for converters expanding into foam, gasket and high-value specialty applications.

Trade show productization: Live demonstrations at trade shows in early 2026 highlight vendor strategies that prioritize modularity and cross-functionality—features buyers increasingly demand to future-proof capex investments.

Standards and certification: Vendors with international certifications (ISO, CE) are winning quicker adoption in regulated markets where compliance reduces buyer switching friction.

Embed safety and certification into product roadmaps — redesign critical thermal management components, publish safety test data, and proactively certify to reduce procurement friction after recent recalls.

Secure raw-material optionality — establish supplier partnerships for film and adhesive alternatives, index contracts to reduce spot volatility, and pilot bio-based or lower-oil-content adhesives where feasible.

Prioritize retrofit and service revenue — convert installed-base relationships into annuity streams through uptime guarantees, remote diagnostics, and consumable lock-ins; service can become the highest-margin growth channel in the near term.

Assess consolidation and bolt-ons — given the fragmented vendor landscape, targeted M&A to acquire technology gaps, broaden distribution, or secure regional manufacturing can be value accretive if integration is disciplined.

Accelerate digital sales tools — provide buyers with configurators, TCO calculators, and safety/maintenance playbooks to shorten sales cycles and improve conversion rates for higher-ticket industrial equipment.

For executives planning capital allocation and commercial strategy in 2026, the critical choices are not whether the market will grow—the macro trajectory is clear—but where to place bets: upgrade installed bases with safety- and energy-focused retrofits, lock in alternative-material supply routes to reduce margin volatility, and build service-led go-to-market engines that monetize installed equipment over lifecycle horizons. Companies that act across these fronts will be best positioned to capture disproportionate gains as the laminator market progresses toward the projected 2032 scale.

This brief communicates strategic highlights and operational implications; the full PW Consulting Laminator Market report contains the detailed segment-level time series, interactive scenario models, supplier tabs, and the vendor scorecards referenced above. Access to the complete dataset and a tailored executive briefing is available through our report portal or by contacting PW Consulting advisory services for a customized 90-day implementation plan.

For detailed analysis of this topic, please visit the official page:Laminator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com