Asia-Pacific E-Sim Market New Industry Opportunities

Other |

2026-06-22 16:11:19

As companies plan product launches, channel expansions, and M&A activity for 2026, a clear-eyed view of the global massage chair market’s trajectory is essential. PW Consulting’s latest study, anchored on a 2025 base year, synthesizes historical performance (2020–2025) and a robust forecast for 2026–2032. The market moved from an identifiable base in 2020 to roughly USD 215.0 Million in 2025 and, under our central scenario, is projected to expand at a compound annual growth rate (CAGR) of approximately 6.98% through 2032 — reaching an expected market size of about USD 345 Million by the end of the forecast horizon. This preview explains how those macro dynamics translate into actionable strategic choices for executives in 2026, while preserving the proprietary sub‑segment detail that we reserve for our full report.

Massage Chair Market

Timing investments: With mid‑single‑digit to high‑single‑digit growth across the forecast window, 2026 is a pivotal year for firms seeking scale before the market reaches broader maturity. The growth profile supports accelerated investment in product differentiation and premiumization for select markets, while also validating cost optimization initiatives for mass channels.

Massage Chair Market

Balancing R&D vs. go‑to‑market spend: Advances in AI-driven health features, 4D/5D mechanical systems, and integrated wellness platforms are lifting buyer willingness to pay in premium segments. Companies must decide whether to allocate marginal dollars to engineering higher performance or to distribution and experiential retail that accelerate adoption.

Massage Chair Market

Managing supply‑chain and tariff risk: Import controls and tariff regimes are creating transient price elasticity in some supply routes. The optimal 2026 strategy often blends near‑term sourcing adjustments with medium‑term localization and supplier diversification to protect gross margins without eroding competitive positioning.

Product strategy — prioritize modular innovation. The market’s growth allows premium vendors to lead with differentiated mechanics (e.g., 4D/5D tracks, walking‑leg systems, advanced airbags) and health integration (AI body‑scan, biometric feedback). At the same time, mass‑market players benefit from modular architectures that enable tiered feature sets without full platform redesigns.

Channel strategy — optimize experiential and digital blend. Buyers of higher‑end wellness furniture increasingly expect demonstration environments and data‑led aftercare. Combining boutique in‑store demos with high‑quality online content and flexible trial policies will shorten conversion cycles in 2026.

Pricing & promotions — move beyond discounting. Tax-advantaged reimbursement pathways (HSA/FSA) and therapeutic positioning can support value‑based pricing for qualifying products. Sellers should align product certification and marketing with these channels to capture higher LTV buyers.

M&A and partnerships — focus on capability gaps. Given the market’s trajectory, acquisitive buyers should prioritize targets that accelerate digital services (telehealth integration), proprietary motion technologies, or established experiential retail footprints rather than betting solely on volumetric scale.

Operations — nearshoring and automation. Tariff pressure and labor cost differentials make selective nearshoring an economically rational choice. Simultaneously, investing in assembly automation yields resilience and margin stability as volumes increase through the forecast period.

The contemporary market combines legacy wellness brands, engineering‑led manufacturers, and newer entrants that fuse robotics and AI. Leaders differentiate across two dimensions: mechanical and software IP (motion systems, patented rollers, thermal and spinal therapies) and user experience (zero‑gravity ergonomics, body scan, personalized programs). The following exemplars illustrate prevailing strategies:

Human Touch — Long Beach, California: Positions as a wellness‑tech innovator with whole‑body robotic chairs and ergonomic designs. Their emphasis on patented circulation and flexible frame technologies supports premium, health‑forward messaging and HSA/FSA qualification pathways.

Osaki — Japan: Focused on high‑precision mechanical systems (4D/5D tracks, SL flex tracks) and embedded AI for body scanning. Their engineering posture and premium feature sets drive a “best‑in‑class” perception in markets that value technical leadership.

OSIM — Singapore: Integrates traditional therapeutic techniques (e.g., shiatsu analogs) with mass adoption levers. A broad patent portfolio and endorsements from professional bodies underpin its repositioning toward clinically credible wellness solutions.

Body Friend — South Korea: Combines advanced mechanical innovations (walking‑leg tech, comprehensive air and heat systems) with AI health features; recently showcased next‑generation models at CES, signaling an aggressive product cadence.

Family Inada — Osaka, Japan: Heritage in shiatsu therapy and high‑performance clinical chairs; their deep practice roots enable premium therapeutic claims and differentiated aftercare propositions.

Ceragem — South Korea: Leverages spinal therapy positioning and dual‑engine mechanics to target buyers seeking a fusion of medical and lifestyle benefits.

Ogawa — Switzerland: Crafts luxury wellness solutions for home and professional contexts, emphasizing premium materials, ergonomics, and an elevated ownership experience.

Recent trade‑show activity in early 2026 — including CES product reveals and Las Vegas furniture market showcases — underscores ongoing R&D intensity. Firms used these venues to launch or preview 4D/AI‑enabled models and new ergonomic enclosures that make in‑home use more seamless and appealing. These events also signal accelerating product cycles and intensifying differentiation on software and sensor stacks, not just raw mechanical capability.

Regulation and safety: Compliance with CPSC safety rules and truthful FTC advertising is non‑negotiable in North America; manufacturers must integrate compliance reviews early in product development to avoid time‑to‑market delays and reputational risk.

Trade and tariffs: Import controls and varying tariff rates on certain origins are materially influencing landed costs. Effective strategies include diversified sourcing, tariff engineering (component reclassification), and strategic inventory hedging.

Labor and margin pressure: Established engineering hubs (notably in Japan) sustain premium positioning through patent control and specialized labor; but higher cost bases necessitate premium pricing or productivity investments to preserve margins.

Reimbursement and clinical pathways: Select models that meet documentation and performance thresholds can access HSA/FSA and similar reimbursement mechanisms. This creates a meaningful route to higher‑value customers when supported by clinical evidence and correct product classification.

Market modeling: Transparent model architecture with historical calibration (2020–2025) and scenario‑based forecasts through 2032, including upside/downside paths tied to adoption of AI and regulatory shifts.

Segment playbooks: Tactical roadmaps for premium, mainstream, and professional channels covering product specs, price bands, recommended feature mixes, and three prioritized go‑to‑market strategies per segment.

Competitive benchmarking: Side‑by‑side comparison of product portfolios, IP positions, patent mapping, distribution footprints, and digital capabilities for the market’s leading players.

Supply‑chain risk matrix: Vendor dependency analysis, tariff exposure mapping, and recommended nearshoring/dual‑sourcing architectures to protect margin and continuity.

M&A and partnership targets: Curated shortlist of acquisition candidates and strategic partners that accelerate capability gaps in AI, telehealth, or experiential retail — with initial valuation heuristics and integration risks.

Commercial instruments: Promotional playbooks, channel incentive designs, and trial/return policies tailored to shorten conversion cycles and reduce churn.

Executive brief: Use the macro contours here to validate investment pacing. If your board requires justification for near‑term capital allocation, the demonstrated CAGR and forecast horizon support prioritized spend on product differentiation and supply rationalization.

Product & engineering: Map your roadmap against the competitive features highlighted here — prioritize modular platforms that enable rapid feature add‑ons and certification pathways for reimbursement.

Commercial teams: Rework channel economics to test experiential retail pilot programs in high‑affinity markets where buyers show willingness to pay for demonstrable therapeutic benefits.

M&A scouts: Use our recommended target profiles to fast‑track diligence on assets that provide immediate capability lift (AI stacks, sensor IP, or deep clinical validation).

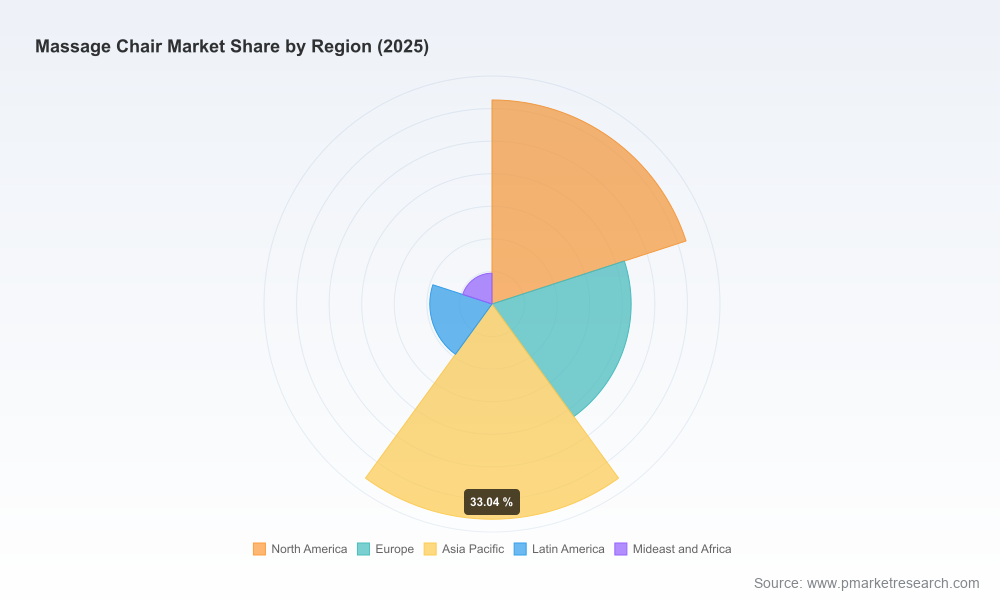

Note: This preview intentionally focuses on strategic implications and high‑level macro metrics to illustrate the study’s value. We do not disclose the report’s protected sub‑segment tables or granular regional/application breakdowns in this summary. For complete data tables, segment‑level forecasts, and the full set of tactical playbooks, consult the PW Consulting Massage Chair Market report or contact our advisory desk for a tailored executive briefing.

For detailed analysis of this topic, please visit the official page:Massage Chair Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com