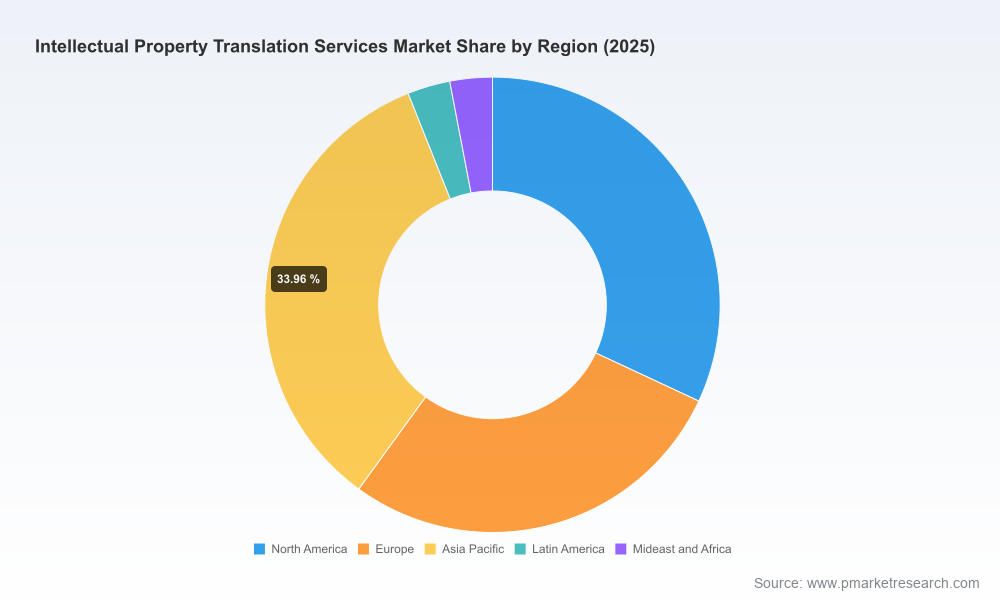

PW Consulting: Intellectual Property Translation Market Set to Reach USD 6.50 Billion by 2032 at 6.5% CAGR — Patent Translation Leads with USD 2.76 Billion in 2025

Other |

2026-07-02 06:30:22

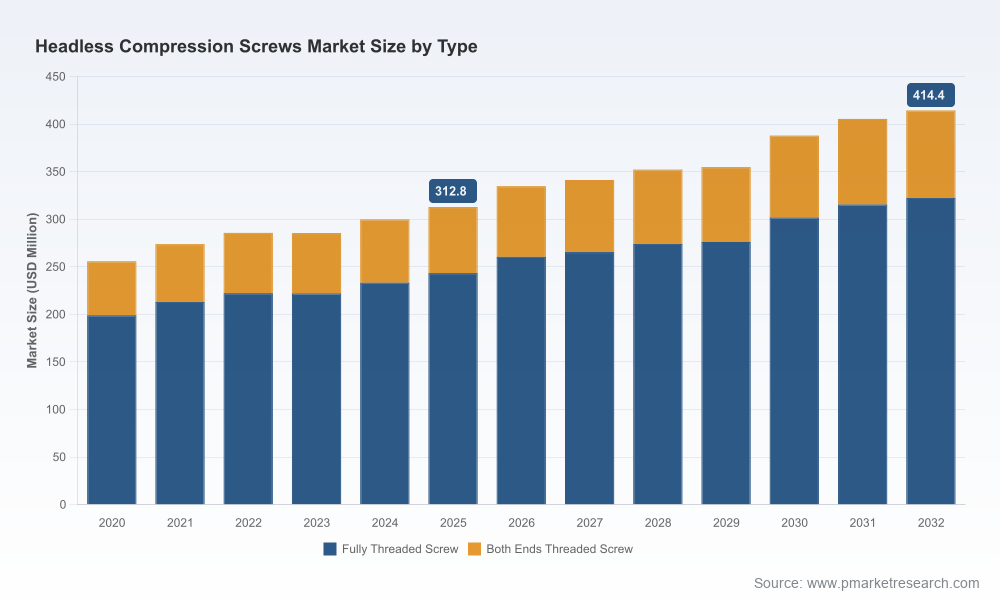

As ambulatory surgery trends, small-bone fracture fixation innovations, and supply-chain pressures converge, headless compression screws (HCS) are moving from niche consumable to strategic portfolio item for orthopedic device manufacturers, distributors and high-volume surgical centers. Our PW Consulting Headless Compression Screws Market study (base year 2025; historical 2020–2025; forecast 2026–2032) synthesizes market sizing, supplier economics, regulatory dynamics and tactical playbooks into a single operational roadmap. The market has demonstrated steady expansion through the mid-2020s and, under our central forecast, continues to grow at a compound annual growth rate of 4.1% across the 2026–2032 horizon — a profile that supports measured investment rather than speculative scale‑ups.

Headless Compression Screws Market

From 2020 through 2025 the market expanded steadily, reflecting rising procedure volumes in hand, wrist, foot and ankle specialties and continued adoption of headless constructs for intra-articular and small-bone work. Our baseline observations indicate the market crossed several tactical inflection points by 2025 — increasing SKU rationalization among OEMs, stronger distribution plays into ambulatory surgery centers (ASCs), and an elevated focus on instrumentation ergonomics. Under the central scenario, the total market continues to increase through 2032, with growth driven by modest volume gains, incremental price mix improvements, and the ongoing replacement cycle for instrumentation and disposables.

Headless Compression Screws Market

The HCS competitive landscape is meaningfully concentrated: a small set of global and regional firms command the bulk of institutional trust with surgeons and procurement teams. Our competitive concentration analysis shows that the top three players hold a clear majority of the market, and the top five expand that share materially — a structure that favors differentiated clinical evidence, channel depth, and responsive supply chains.

Headless Compression Screws Market

Implication for 2026 decisions: firms evaluating expansion should weigh the cost of entry against the time and investment required to build surgeon-level preference. For incumbents, the priority is protecting share through targeted clinical investment, channel lock-in with high-value ASCs and hospitals, and disciplined SKU rationalization to improve margins.

Raw material dynamics are a practical lever for margin and pricing strategy. Titanium — both commercially pure grades and aerospace‑grade Ti-6Al-4V — remains the central input, and its price volatility directly affects COGS for implants and instrument sets. Recent market observations in Q2 2026 show distinct spreads between commercially pure grades, alloyed titanium, and scrap streams. Suppliers and OEM pricing teams should run sensitivity scenarios against +/- ranges to understand EBITDA exposure and to design procurement hedges or long-term supplier contracts accordingly.

Regulatory events have immediate and asymmetric effects in this market. The ongoing Class 2 recall affecting a major supplier is a reminder that clinical surveillance, lot-tracking, and rapid response capabilities are strategic imperatives. Simultaneously, legacy standards and licensed uses — such as AO Foundation approvals for select sizes — continue to shape surgeon trust and hospital formularies. For 2026 planning, embedding regulatory readiness into go-to-market and supply contingencies is mission-critical.

The full PW Consulting report is designed as an operational playbook, not an academic exercise. Core deliverables include:

We recommend a three-track approach for C-suite and business-unit leaders crafting 2026 plans:

Given the market’s steady, mid-single-digit CAGR and concentration dynamics, inorganic strategies should be highly selective. Targets that bring differentiated clinical IP, unique distribution/access to high-growth ASCs, or manufacturing efficiencies (including ISO/FDA alignment) will deliver the best risk-adjusted returns. Acquirers should insist on complete traceability of supplier contracts and an audited assessment of recall history and post-market surveillance programs as part of due diligence.

Senior leaders can use the insights above to:

This preview is intended to orient executives and investment committees to the strategic levers in 2026. The comprehensive PW Consulting Headless Compression Screws Market report contains the full data tables, segment forecasts, buyer maps and downloadable Excel models necessary to operationalize these recommendations. For clients preparing 2026 budgets, procurement contracts, or M&A pipelines, accessing the complete dataset will materially shorten the path from insight to action.

To procure the full study and the accompanying decision-support templates, contact PW Consulting. Our team can also deliver a tailored briefing that aligns the market model to your P&L and go-to-market cadence.

For detailed analysis of this topic, please visit the official page:Headless Compression Screws Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com