U.A.E. Food Fibers Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-22 06:42:39

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present a targeted executive introduction to our new First Aid Kits Market study. This briefing synthesizes the market’s recent trajectory, near-term regulatory inflection points, competitive landscape, and the practical takeaways that should shape capital allocation, product strategy, and go-to-market planning in 2026.

First Aid Kits Market

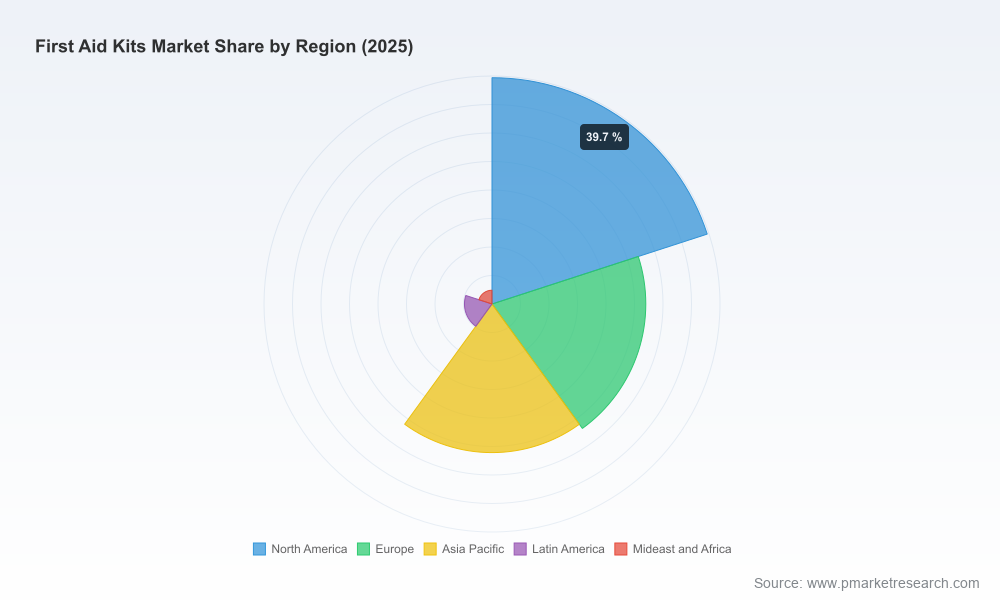

The first aid kits sector is no longer a simple consumables market; it is a regulated, quality-driven, service-enabled ecosystem that touches occupational safety programs, consumer health preparedness, trauma response, and industrial compliance. Our analysis — based on a 2020–2025 historical review and a 2026–2032 forecast window — shows a clearly positive but moderate growth profile. The addressable market grew from roughly USD 163 million in 2020 to around USD 215 million in 2025, and with a compound annual growth rate of 4.2% through the forecast period, it will expand further as buyers shift toward higher-specification products and bundled service models.

First Aid Kits Market

For executives making 2026 decisions, that growth signals two things: steady topline expansion across core categories, and meaningful pockets of strategic differentiation where smart investments can produce outsized returns. Our report is designed to identify those pockets — without publishing the proprietary segment-by-segment extracts here — and to provide the operational playbooks needed to win.

First Aid Kits Market

Regulatory re‑alignment raises the bar. The Quality Management System Regulation (QMSR), effective February 2026, aligns FDA device quality requirements with ISO 13485:2016. Simultaneously, state-level moves toward stricter kit specifications (e.g., proposed compliance with ANSI/ISEA Class A requirements) are increasing baseline quality and documentation expectations. These changes accelerate compliance costs for manufacturers that have not yet migrated to ISO-aligned QMS frameworks, and they favor suppliers with established medical-device-style quality systems.

Input cost volatility is real and persistent. Between 2023 and 2025, market participants saw near‑double‑digit increases in the cost of medical‑grade gloves, antiseptics, and trauma materials, driven by supply concentration in Asia and elevated freight. Cost pressure is an enduring constraint on margin models unless mitigated by procurement, localization, or value-added service pricing strategies.

Service differentiation is accelerating competitive shifts. Buyers are increasingly purchasing kits as part of replenishment services, managed rental programs, and private-label arrangements rather than as one-off product transactions. Lifecycle management (inventory rotation, restocking, expiry tracking) is now a discrimination factor in contract renewals and large employer accounts.

This research goes beyond market sizing. It is built for immediate use by strategy, procurement, product development, and corporate development teams considering actions in 2026. Highlights include:

The sector shows moderate concentration: the top three firms represent a material share of market revenue, and the top five control a clear majority. That concentration creates both entry barriers and predictable acquisition targets for scale players.

First Aid Only (Shelton, US) — Strength lies in cost-effective, OSHA-compliant workplace kits and refill systems. They are a benchmark for price‑competitive compliance offerings and quick-to-deploy corporate programs.

The American Red Cross (US) — Brand trust and widespread institutional presence make their ANSI/OSHA-compliant kits a go-to for organizations that prioritize recognized standards and institutional liability protection.

North American Rescue (US) — Focused on trauma care and public-access bleeding control, they are the reference supplier for high-acuity kits and tactical applications. Their portfolio signals the premium-trauma growth pathway.

Aero Healthcare (US) — A specialist in wholesale, private-label manufacturing, and managed rental/restocking systems. Aero is illustrative of the vertically integrated model that converts product revenue into predictable service margins.

My Medic & JumpMedic (US) — Both position to capture premium consumer and responder-selected segments with differentiated design and component quality. They demonstrate the willingness of end consumers and specialty buyers to pay a premium for perceived clinical credibility.

Cintas Corporation (US) — Leverages broad workplace services reach to bundle kits, cabinets, and replenishment — a competitive advantage in renewing long-term contracts with enterprise customers.

Collectively, these firms illustrate three viable strategic archetypes in 2026: compliance‑price leaders, premium/trauma specialists, and service-integrated providers. Successful new entrants or scale-up strategies should pick an archetype and align R&D, QMS investment, and channel approach accordingly.

We highlight a few market risks every 2026 board should track: continued input-cost inflation, tighter regulatory documentation requirements under QMSR, counterfeit/low-quality imports that compete on price, and shelf-life management complexity for large-scale replenishment contracts.

In keeping with PW Consulting’s client engagement model — and our “trailer” principle — this briefing demonstrates analytic depth while withholding certain proprietary segment-level splits and granular revenue-by-channel figures. Those detailed tables, micro-segmentation maps, and client-ready slide decks are included in the full report and the companion data workbook, which are available to subscribers and clients who seek transaction-grade intelligence.

Prioritize QMS alignment now. Firms that update their quality management systems to ISO-aligned standards will reduce regulatory friction, shorten approval timelines with institutional buyers, and be better positioned for cross-border contracts.

Convert product transactions into recurring services. Invest in inventory-management tech, expiry-tracking, and customer-facing dashboards to capture higher-margin replenishment revenue and deepen client stickiness.

Pursue vertical integration for critical consumables. For mid-sized manufacturers, partial upstream integration or secure long-term supply agreements can insulate margins from the supply shocks observed in 2023–2025.

Target niche trauma and premium segments for margin expansion. The trauma/public-access bleeding-control niche is structurally attractive and aligns with public-safety spending and community preparedness programs.

Use M&A selectively to buy QMS and service capability. Given the market concentration dynamics, bolt-on acquisitions that add ISO‑aligned quality systems, managed-services capability, or trauma expertise are the fastest way to scale into adjacent high‑margin segments.

For executives preparing budgets and M&A pipelines in 2026, this market represents stable growth with specific high-value opportunities where quality, service, and regulatory readiness matter most. PW Consulting’s full First Aid Kits Market report provides the proprietary segmentation, scenario models, and downloadable diligence materials required to convert these strategic recommendations into executable programs.

Contact PW Consulting for access to the complete report, the underlying data workbook, and an advisory session tailored to your organization’s positioning and 2026 priorities.

For detailed analysis of this topic, please visit the official page:First Aid Kits Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com