Sell Your Diamond Ring for the Best Price in the UK – Fast Online Valuation

Shopping |

2026-06-09 11:09:21

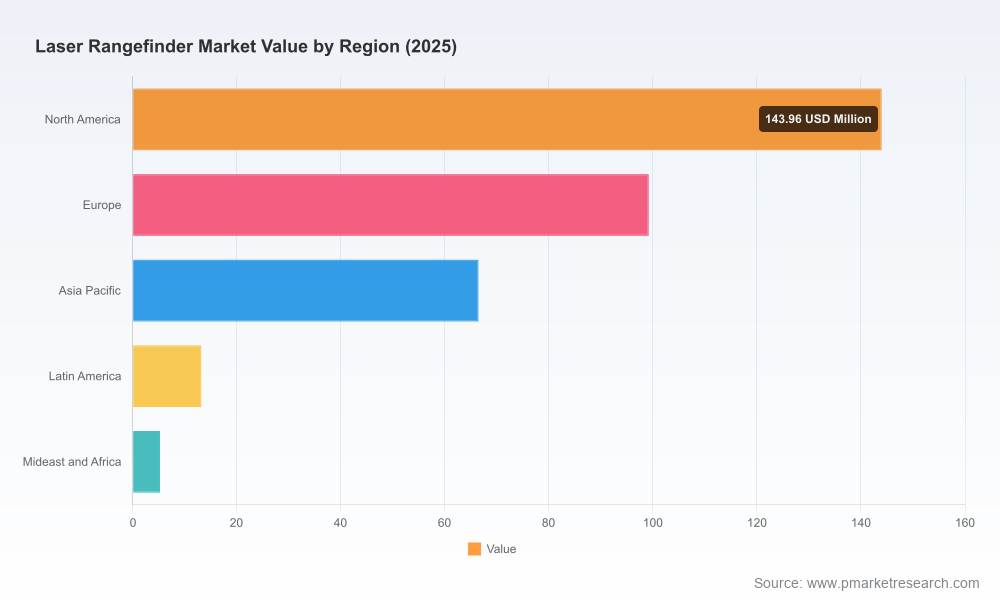

As organizations plan capital allocation, product roadmaps, and M&A strategies for 2026, a clear, data-driven line of sight into the laser rangefinder market is table stakes. PW Consulting’s latest market study—grounded in a 2020–2025 historical base and projecting through 2026–2032—translates raw market motion into executable strategic options. The market has expanded from a historical base of USD 218.0 Million in 2020 to USD 328.0 Million in 2025 (base year), and is forecast to reach USD 580.0 Million by 2032, growing at a compound annual growth rate (CAGR) of 8.85% over the 2026–2032 forecast window. This briefing highlights the study’s strategic value for 2026 planning while intentionally preserving the granular segmentation tables and line-item forecasts for subscribers of the full report.

Laser Rangefinder Market

Timing and scale: The post-2025 rebound and the near‑double‑digit CAGR through 2032 transform tactical procurement choices into multi‑year platform bets. Knowing whether to prioritize module integration, sensor fusion, or aftermarket services can materially affect 2026 capex and product prioritization.

Laser Rangefinder Market

Cross‑sector inflection points: Convergence between defense modernization, UAV autonomy, and precision civil applications (surveying, construction, forestry) creates adjacent revenue opportunities. Strategic clarity on which nodes of the value chain to own is essential for 2026 positioning.

Laser Rangefinder Market

Risk‑adjusted investment: Supply‑chain bottlenecks (opto‑electronics, semiconductors), export control regimes, and evolving standards require scenario planning. The report builds modular sensitivity analyses that allow CFOs and strategy teams to stress‑test 2026 investments under alternate supply and demand shocks.

Validated market sizing and growth scenarios: A transparent methodology anchored to the 2020–2025 historicals and three forward scenarios through 2032—useful for budgeting and investor presentation decks.

Technology and product roadmaps: Comparative analysis of laser type (eye‑safe vs. standard), microLiDAR modules, diode‑pumped vs. solid‑state designs, and miniaturized receiver/processor components—each mapped to typical system architectures and cost implications.

Commercial playbooks: Go‑to‑market options tailored to OEMs, integrators, and service providers—covering direct defense sales, commercial channel strategies, partner ecosystems for drone/autonomy play, and aftermarket service monetization.

Vendor scorecards and procurement frameworks: A repeatable RFP scoring model that synthesizes performance, reliability, SWaP (size, weight, and power), certification readiness, and supply risk into a single decision matrix.

Deal and partnership opportunities: Identification of tuck‑in or capability acquisitions, joint development options, and white‑label integration scenarios—ranked by time‑to‑value and technical risk.

Regulatory and export impact assessment: Practical guidance for compliance planning, including export control choke points that affect defense‑oriented modules and cross‑border supply relationships.

The market remains moderately fragmented with meaningful room for consolidation and strategic alliances. A cluster of established European and North American engineering leaders competes alongside nimble specialized suppliers and a growing number of Asia‑based manufacturers addressing civilian and recreational demand. Competitive dynamics vary markedly by product tier: high‑end defense modules are dominated by firms with deep systems integration experience and defense contracts, while the commercial drone, surveying, and recreation tiers are more contestable and innovation‑led.

JENOPTIK AG (Germany) — https://www.jenoptik.com: Engineering depth in compact solid‑state and diode‑pumped modules positions Jenoptik for vehicle and fire‑control integration. Strengths: proven module architectures suitable for militarized platforms; Risk: higher cost structures versus commodity vendors.

Safran Electronics & Defense (France) — https://www.safran-group.com: Offers integrated modules and full systems for aerospace and defense. Strategic advantage lies in systems‑level integration and long procurement cycles with armed forces; 2025–26 product updates indicate focus on drone tracking and multi‑sensor applications.

Laser Technology, Inc. (US) — https://www.lasertech.com: Known for reflectorless, professional rangefinders tailored to surveying and forestry. Their customer intimacy in civil geospatial markets is a defensible moat for service and software up‑sell.

LightWare LiDAR (Denmark) — https://lightwarelidar.com: Specializes in ultralight microLiDAR and gimbal‑optimized modules for drones and robotics. Recent product launches extending gimbal ranges signal a push into autonomy and inspection markets.

Lumibird (France) — https://www.lumibird.com: Strong defense integration footprint with recent contract awards for air‑defense and naval platforms. Their portfolio implies both product breadth and scale in deliveries for multi‑year defense programs.

Shenzhen Laser Explore Tech. (China) — https://laserexplore.goldsupplier.com: Cost‑competitive eye‑safe and recreational optics appeal to consumer segments (hunting, golf), representing volume plays rather than defense systems dominance.

Analog Modules, Inc. (US) — https://analogmodules.com: Provider of miniaturized receivers and processors—critical components for high‑performance tactical and moving‑target applications. Product miniaturization is a clear enabler for UAV and handheld platform integrations.

ERDI TECH LTD (China) — https://erdicn.com: Focused on eye‑safe modules suited to construction and surveying integration, representing an accessible entry point for system integrators seeking compliance and safety certification.

Attollo Engineering (US) — https://attolloengineering.com: Low‑SWaP WASP™ series addresses defense UAVs and handheld use cases. Their positioning is attractive for integrators prioritizing endurance and weight constraints.

JIOPTICS (China) — https://www.jioptics.com: Supplies longer‑range commercial and military units; suitable for applications requiring extended standoff capability.

Contract awards to established defense suppliers highlight persistent defense demand and program stickiness—evidence that large platform integrations will continue to underwrite a substantial share of high‑end module demand through 2028.

Product launches in 2024–2025—particularly in microLiDAR and miniaturized receivers—signal a commercial tipping point where autonomy and drone inspection use cases are transitioning from pilots to scaled deployments.

Vendor diversification: simultaneous presence of European incumbents, US miniaturization specialists, and Chinese volume players suggests differentiated competitive battlegrounds by application tier rather than a single global leader set.

Prioritize modular investments that enable multi‑market reuse. Design choices that allow the same sensor core to be certified for defense, commercial UAV, and industrial inspection dramatically improve time‑to‑market and margin levers.

Build supply risk hedges now. Semiconductor and specialized optic suppliers will be bottle‑necks in higher growth scenarios. Establish dual‑sourcing, early vendor qualification, and inventory strategies tied to scenario triggers in the report.

Expand aftersales and software services. As sensor commoditization progresses in civil tiers, revenue differentiation will move to analytics, calibration services, and integrated mapping platforms.

Assess targeted M&A and JV plays. Small, technology‑rich suppliers (miniaturized receivers, microLiDAR) are high‑value acquisition targets for system OEMs seeking quick capability fills; our deal pipeline matrix identifies priority targets by technical fit and valuation bands.

Mitigate regulatory exposure. For defense‑oriented strategies, evaluate ITAR, national export controls, and third‑party supplier country of origin risks. The full report provides an actionable compliance checklist.

Integrated demand mapping: We translate defense program schedules, drone commercialization timelines, and civil infrastructure investment into synchronized demand trajectories—usable for procurement, manufacturing ramp plans, and investor returns modeling.

Practical vendor playbooks: Beyond rank ordering, we provide negotiation levers, testing and acceptance templates, and long‑lead item trackers that procurement teams can implement during 2026 contracting cycles.

Transaction readiness: For corporate development teams, the report includes a short list of accretive target archetypes and a guided valuation framework attuned to the market’s growth profile and consolidation dynamics.

The macro trajectory—from USD 328.0 Million in 2025 to USD 580.0 Million by 2032 at an 8.85% CAGR—confirms a market with persistent defense underpinning and accelerating commercial adoption. For executives preparing 2026 capital and product decisions, the full PW Consulting Laser Rangefinder Market report provides the segment‑level insights, supplier scores, and scenario tools necessary to convert that trajectory into defensible, high‑impact strategic moves. Visit our research portal to access the comprehensive datasets, segmentation dashboards, and executable annexes that we have intentionally reserved for subscribers.

For detailed analysis of this topic, please visit the official page:Laser Rangefinder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com