What Is a Meta Ads Automation Tool and Why Every Marketer Needs One in 2026

Other |

2026-07-07 10:18:03

By PW Consulting — Senior Strategy & Industry Analysis

Air Ambulance Market

This briefing is a strategic preview of our full Air Ambulance Market study (base year 2025, forecast 2026–2032). It synthesizes the market forces, regulatory inflection points and competitive dynamics that will determine value creation in 2026 and beyond. The intent is to demonstrate the analytical depth and practical orientation of the report while preserving the proprietary, segment-level detail that corporate decision makers require — details that are available in the full report on our website.

Air Ambulance Market

The air ambulance market has moved from a niche emergency service into a growth sector with clear commercial expansion drivers. Measured on a global revenue basis, the market expanded steadily through 2020–2025 and is expected to continue that trajectory into the next planning cycle. PW Consulting’s topline projection shows the market crossing the high teens in the immediate post‑base year and approaching the low thirties in the 2032 horizon, reflecting a compounded annual growth rate of 8.5% across the forecast period (2026–2032). This combination of resilient demand and favourable structural tailwinds makes 2026 an important decision year for operators, investors and health-system partners.

Air Ambulance Market

Regulatory and reimbursement convergence. Policy interventions enacted since 2022 — most notably balance-billing restrictions and enhanced reporting obligations — have materially changed pricing risk for operators. In 2025, finalised reimbursement schedules from major payors introduced a higher degree of payment certainty. Together, these shifts compress regulatory uncertainty while creating a new set of performance metrics operators must meet to protect margin.

Safety and certification pressures. Aviation safety and clinical-accreditation expectations continue to rise, with regulators mandating standardized data collection and operational standards. These requirements increase baseline operating costs but also raise barriers to entry for new, under-capitalised entrants.

Unit economics under strain and scrutiny. Labour and clinical staffing remain the single largest recurring cost category — specialised clinicians, 24/7 readiness, and crew training place significant pressure on per‑transport economics. Typical single-transport cost profiles sit in the tens of thousands of USD, making reimbursement stability and utilization critical to operator viability.

Technology and models of care unlocking new demand. Improved dispatch algorithms, predictive positioning, telemedicine-enabled pre-flight stabilization, and tighter hospital integration are expanding the practical service envelope for air transfer — from time-critical trauma to inter-facility critical-care relocation. These service extensions create both revenue opportunities and integration challenges for incumbents and new entrants alike.

Our full report is designed for executives and deal teams who need actionable evidence, not just descriptive analysis. Key deliverables include:

Robust market sizing and scenario projections — top-down and bottom-up reconciliations that cover base case, downside and accelerated-growth scenarios for 2026–2032 (we deliberately preserve segment granularity for subscribers).

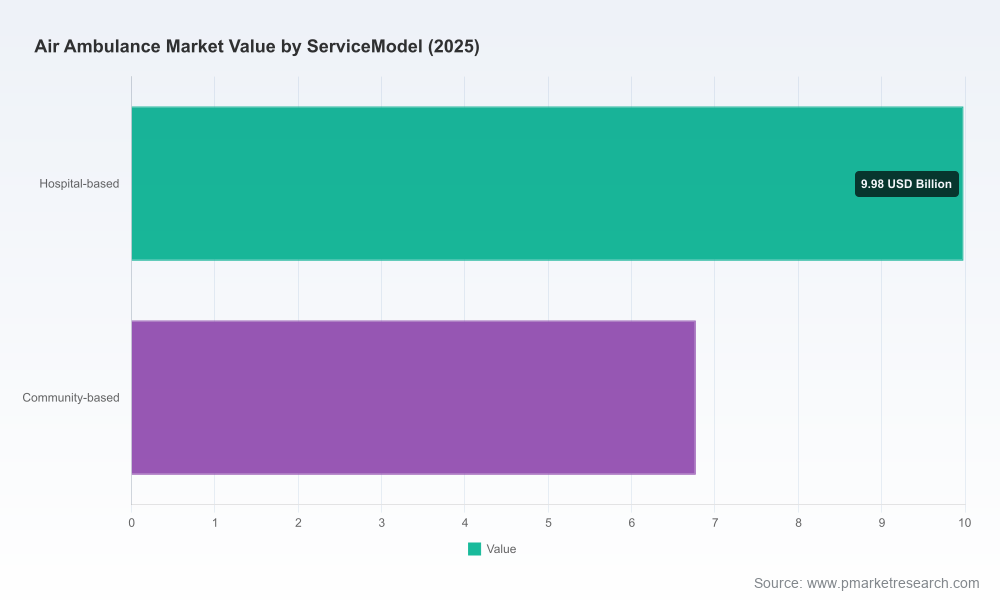

Service-model playbooks — operational benchmarks and unit-cost decompositions for hospital-based, community-based and membership-driven models, along with best-practice checklists for fleet utilization and base network planning.

Regulatory and reimbursement stress tests — scenario models that translate policy changes and payor rate shifts into P&L and cash-flow impacts under multiple contract structures.

Commercial diligence templates — market-entry and M&A scorecards, revenue-synergy matrices, and a due-diligence questionnaire tailored to air medical operators and health-system partners.

M&A and partnership playbook — valuation frameworks, integration risks, and three archetypal roll-up strategies with expected IRR ranges under conservative and aggressive assumptions.

Technology and workforce roadmap — investment priorities for digital dispatch, tele-ICU integration, and clinical staffing models that reduce cost-per-flight while maintaining quality and compliance.

The market exhibits a modest-to-moderate level of concentration at the national level, with the top three players accounting for just over half of the market by revenue and the top five commanding approximately two-thirds. This structure produces a dynamic environment where national operators, regional providers and franchised membership networks each pursue distinct strategies to secure volume and margin.

Air Methods — A large national operator with a mixed helicopter and fixed-wing footprint focused on trauma, cardiac and paediatric critical-care transfers. Recent publicly observable moves include expanding partnership agreements with health systems and stepping up fleet additions to increase nationwide availability.

Global Medical Response (GMR) — An integrated emergency services provider combining ground and air capabilities. Their value proposition is operational integration: blended dispatch, shared clinical protocols and cross-modal capacity that reduce handoff friction for inter‑facility moves.

PHI Air Medical — A rotor-centric national player emphasising round-the-clock critical-care services and membership propositions designed to provide out‑of‑pocket protection for patients. Their base and fleet strategy seeks to maximise short‑response coverage in major catchment areas.

REVA Air Ambulance — A leading fixed‑wing ICU-level operator focusing on long-distance, bedside-to-bedside transfers. Their service specialization is attractive for hospital systems looking to de-risk cross-border and long-haul critical transfers.

Acadian Companies — A regionally strong operator combining helicopter and fixed‑wing services with deep local health-system relationships — a model that underlines the importance of local clinical networks and community trust.

AirMedCare Network — The membership network business model provides a financial-protection layer and a channel for demand aggregation, aligning incentives between patients, hospitals and operators while smoothing revenue volatility for partners.

Recent industry moves underscore two competing strategies: scale through national footprint expansion and differentiation through specialised fixed-wing ICU services or membership/insurance hybrids. Operators that can credibly combine a dense short-range rotor network with specialist long-range fixed-wing capacity will be best positioned to capture mixed-demand flows without sacrificing utilisation.

Prioritise revenue resilience: Lock in diversified revenue streams — hospital contracts, payor arrangements and membership programs — to reduce reliance on spot emergency transports and to protect against reimbursement volatility.

Invest in utilization-first fleet strategy: Use predictive-positioning analytics and hub-and-spoke base planning to raise mission rates per airframe. Fleet additions should be tied to utilisation thresholds backed by route-level demand modeling.

Integrate clinical protocols with hospital partners: Deep clinical integration reduces handoff times and clinical escalation costs. Formalised interop and joint governance with health systems create stickiness and justify higher bundled rates.

Make workforce planning a competitive moat: Upskilling programs, retention incentives and flexible staffing pools lower marginal staffing costs and reduce the operational risk associated with 24/7 readiness.

Use M&A selectively to fill capability gaps: Acquisitions should target either geographic density to improve rotor utilisation or capability (e.g., fixed-wing ICU) that expands average revenue per mission — not simply revenue for revenue’s sake.

Stress-test contracts against policy shifts: Given the prominence of regulatory oversight, commercial teams must model downside payor outcomes and include contractual protections such as escalators, performance gates and shared-savings constructs.

Commission a targeted commercial diligence focused on your priority geographies and service models — including scenario-driven P&L under alternative reimbursement and utilization outcomes.

Run a fleet-capacity stress test: identify which assets to ground, upgrade or acquire to optimise utilisation at the margin.

Pilot a hospital partnership for integrated dispatch and shared clinical governance; measure time-to-transfer, cancellations and revenue uplift over a six‑month window.

Lock in membership and payer pilots to stabilise payer mix and reduce patient-balance risk.

2026 is a decision year: operators need to reconcile higher compliance costs and staffing pressures with accelerating demand and clearer reimbursement signals. PW Consulting’s Air Ambulance Market report provides the granular segmentations, rate-card sensitivity analyses, base-by-base utilisation models and integration playbooks that enable disciplined capital allocation and realistic valuation. This preview outlines the strategic contours — the full report contains the proprietary tables, regional models and transaction frameworks your team will use to make investment and operating decisions with confidence.

To access the full analysis, including detailed segment breakdowns, base-level models and our M&A scorecards, please visit the PW Consulting research portal or contact our advisory team to arrange a tailored briefing.

For detailed analysis of this topic, please visit the official page:Air Ambulance Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com