Form in Place (FIP) Gaskets Market: Strategic Guide for 2026 Decision‑Makers

Executive overview

As companies allocate capital and refine supply-chain strategies for 2026, the Form in Place (FIP) gaskets market is no longer a niche manufacturing line item — it is a strategic lever. PW Consulting’s new study, anchored on a 2025 base year and extending through a 2026–2032 forecast window, synthesizes five years of historical performance (2020–2025) and delivers the scenario-driven intelligence leaders need to choose partners, prioritize automation investments, and protect margin in an environment of raw-material volatility.

Form in Place (FIP) Gaskets Market

At the market level, FIP gaskets have demonstrated resilient growth through the early 2020s, with total industry revenue expanding from roughly USD 1,410 Million in 2020 to approximately USD 2,025 Million in 2025. The research forecasts continued expansion through the 2026–2032 period, targeting roughly USD 2,181 Million in 2026 and projecting a longer‑term trajectory to approximately USD 3,247 Million by 2032 — an implied compound annual growth rate (CAGR) of about 6.98% over the forecast horizon. The market exhibits a moderate concentration profile (CR3 ~42%; CR5 ~51%), indicating meaningful leader activity but with space for disruptive entrants and specialist suppliers.

Form in Place (FIP) Gaskets Market

Why this study matters for 2026 decisions

- Procurement and sourcing strategy: Raw‑material shocks and supplier price moves in early 2026 materially change cost curves for silicone‑based systems. Companies that lock in supply or diversify elastomer sources ahead of peak demand will preserve margin and secure delivery windows.

- Automation ROI: Rapidly maturing dispense and in‑line curing technologies shift where capital delivers the best payback — from throughput gains to quality consistency and reduced scrap in high‑mix electronics and precision sealing applications.

- M&A and partnerships: With the top five players controlling just over half the market, selective acquisitions and contract alliances are being used to access proprietary chemistries, specialized dispensing capabilities, or regulated‑market compliance.

What this report delivers — practical, actionable content

This is not a high‑level summary; it is a handbook for operators and strategists. The report combines rigorous market sizing with operational modules you can act on in 2026:

Form in Place (FIP) Gaskets Market

- Transparent market-sizing methodology, including unit economics for FIP dispensing and curing, and sensitivity testing to raw‑material price vectors.

- Demand‑driver analysis mapped to end‑market adoption cycles (e.g., semiconductor, electronics enclosures, automotive, oil & gas) and the operational levers that accelerate replacement of preformed seals.

- Supply‑chain heatmaps that identify single‑point risks, alternative material suppliers, and viable hedging strategies for silicone feedstocks.

- Technology maturity matrices for dispensing (robotic vs. manual), curing (1K RTV, UV/LED, heat), and conductive vs. non‑conductive formulations — including comparative throughput, capital intensity, and qualification timelines.

- Commercial playbooks: go‑to‑market options for incumbent manufacturers and specialists, pricing models for value‑added services, and channel strategies for Tier‑1 OEMs.

- Granular competitor dossiers and capability benchmarking, with acquisition targets prioritized by strategic fit and integration risk.

- Scenario models and stress tests that quantify EBITDA sensitivity to raw‑material shocks, price pass‑through timelines, and lead‑time elongation.

Competitive landscape — who to watch in 2026

The FIP gasket competitive map blends global chemical incumbents, specialized applicators, and precision‑engineering houses. Our profiles synthesize public disclosures, product roadmaps, and observable channel behaviours to show where capability rivalry will be fiercest.

- Parker Hannifin Corporation (Cleveland, OH) — a leader with both conductive and non‑conductive FIP series. Its recent launches expanded high‑temperature elastomer options for offshore and heavy‑industry sealing, signalling an intent to deepen penetration in energy and industrial markets.

- Laird Technologies (St. Louis, MO) — focused on automated dispensing of conductive elastomer gaskets for enclosure‑level EMI shielding. Laird’s play is scale through automation and integration with electronics manufacturers pursuing miniaturization and higher shielding requirements.

- Nolato Group (Markaryd, Sweden) — advancing conductive silicone rubber formulations and dispensing systems under established product series. Nolato emphasizes integrated EMC shielding solutions and high‑precision applicator partnerships.

- Dymax Corporation (Torrington, CT) — a disruptive technology player with UV/LED‑curable FIP formulations that cure in seconds, dramatically shortening cycle times and enabling in‑line production flows.

- Henkel AG & Co. KGaA (Düsseldorf, Germany) — deploying 1K RTV and assembly‑line dispensing chemistries aimed at high‑volume, in‑line curing use cases where throughput and reliability are paramount.

- Specialist applicators and fabricators — firms such as Sealing Devices Inc., H&S Manufacturing, Central Coating Technologies, KraFAB and Vactec combine custom fabrication, certified dispensing services, and compliance (ISO/ITAR) to serve regulated and complex geometries. These specialists are pivotal for OEMs that choose outsourcing over verticalization.

CR metrics underscore that while established names command scale, there is meaningful runway for technology‑focused entrants to capture share through speed, specificity, and service differentiation.

Supply‑side shocks and regulatory signals you cannot ignore

2025–mid‑2026 market dynamics present a clear lesson: raw‑material exposure equals operational risk. Silicone prices, for example, rose in the first half of 2026 (North American indices about US$6.18/kg and European indices near US$7.98/kg in May 2026), while dimethyldichlorosilane — a critical precursor — surged roughly 28% year‑over‑year in Q1 2026 due to production outages in China. These events extended lead times for key inputs from typical four weeks to as long as twelve weeks by late 2025.

On the supplier side, public price actions matter: a notable silicone price adjustment announced in April 2026 by a major producer materially shifted procurement conversations for many OEMs. Corollary impacts include stretched qualification timelines for alternative chemistries and tightened spot availability for specialized fillers (e.g., conductive powders and fumed silica).

Implications for product engineering and operations

- Design for supply flexibility: Specify alternative base chemistries and qualify two supply chains for critical formulations. Where substitution is non‑trivial, parallel qualification at reduced volumes preserves production continuity.

- Push automation where it reduces total cost of ownership: UV/LED curable systems and advanced dispensing eliminate cure ovens and reduce inventory buffer needs; however, technology switch requires an update to validation protocols and capital planning.

- Shorten time to qualify: Modular test rigs and pre‑approved supplier libraries accelerate qualification cycles — a decisive advantage when lead times are volatile.

- Commercial levers: Consider blended pricing models that bundle material supply with application services, turning a commodity purchase into a higher‑margin partnership.

Recommended strategic actions for 2026

PW Consulting recommends a calibrated roadmap for companies making resource allocation decisions this year:

- Immediate (0–6 months): Run a supply‑risk heatmap, renegotiate terms to include inventory buffer clauses, and start dual‑sourcing critical silicone chemistries. Evaluate short‑term hedges on feedstock exposure and seek caps or floors in long‑term contracts.

- Near term (6–18 months): Pilot advanced dispensing and in‑line curing technologies in constrained product lines to quantify yield and cycle‑time improvements. Lock in strategic partnerships with specialist applicators to manage complex geometries and regulated BOMs.

- Medium term (18–36 months): Decide on vertical integration where capture economics justify capex (e.g., captive dispensing centers for high‑volume modules) versus service partnerships for low‑volume, high‑complexity assemblies.

- M&A playbook: Use CR3/CR5 insights to prioritize targets that fill capability gaps (e.g., UV/LED curing chemistries, precision dispensing automation, or regionally strategic applicator footprints). Ensure integration plans preserve customer continuity and regulatory compliance.

How to use the report as your 2026 playbook

Think of this PW Consulting study as a three‑part toolkit: (1) a fact base that quantifies market trajectory and concentration; (2) an operational manual with supplier maps, technology evaluations, and cost sensitivity models; and (3) a board‑level briefing pack (scenario slides and M&A screens) that converts technical detail into investment decisions.

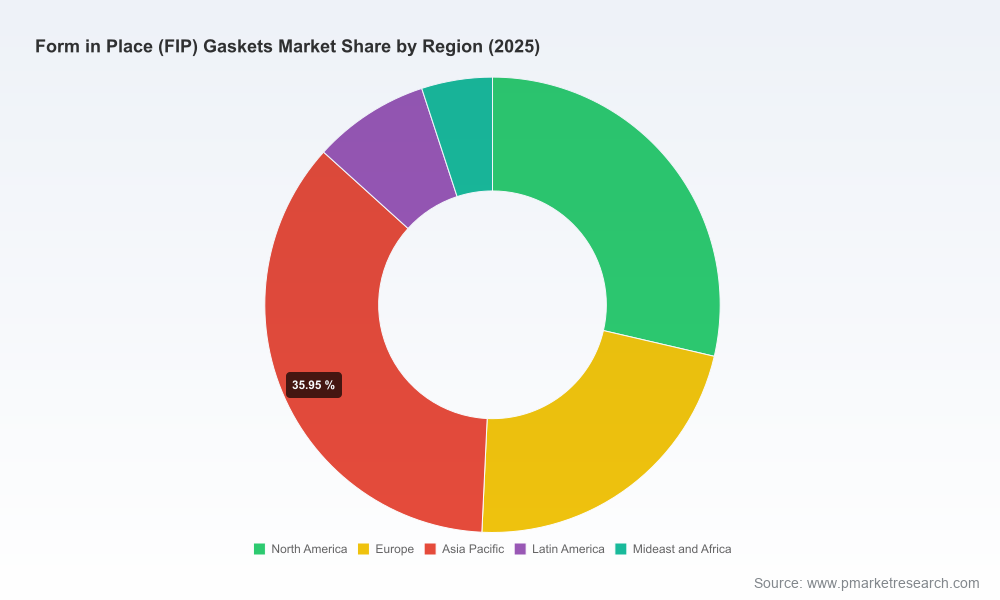

To respect commercial discretion and enable one‑to‑one advisory, granular segmentation tables (regional/application percentage splits, product‑level revenue stacks, and customer‑level contracts) are reserved for report purchasers. Those datasets are the inputs to the scenario matrices you will need to finalize sourcing, capex, and M&A decisions in 2026.

Closing — why engage now

2026 is shaping up to be a pivotal year for FIP gaskets: growth momentum, supplier price realignments, curing‑technology maturation, and concentrated but contestable competition are converging. Firms that combine disciplined procurement hedging, prioritized automation pilots, and targeted partnerships will convert near‑term turbulence into durable advantage.

PW Consulting’s full report operationalizes this insight into step‑by‑step programs, quantitative models, and competitor playbooks tailored for executive committees, procurement teams, and engineering leaders preparing decisions in 2026. For organizations that need to move from awareness to action, the report is designed to be the working document you consult at the negotiation table, the capex committee, and during integration planning.

For detailed analysis of this topic, please visit the official page:Form in Place (FIP) Gaskets Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com