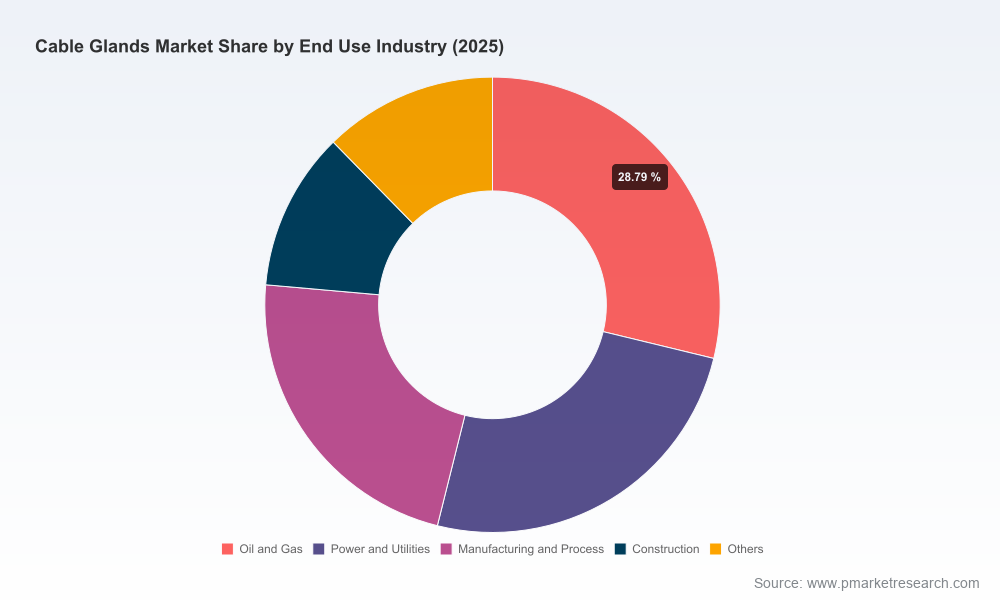

Cable Glands Market — Strategic Preview for 2026 Decision Makers

As PW Consulting’s senior strategy team, we present a high-level, decision-focused preview of our full Cable Glands Market study (base year 2025; forecast 2026–2032). This preview is written to inform board- and C-suite-level decisions you will make in 2026: capital allocation, go-to-market priorities, certification investments, and M&A screening. It shows the analytical depth that underpins our full report while intentionally withholding the granular segment tables and company share matrices that are reserved for report subscribers.

Cable Glands Market

High-level market trajectory you must internalize

The cable glands sector is recovering and re‑rating as industrial, utility and infrastructure programs reaccelerate. On a macro basis, the global market expanded from roughly USD 1,500 Million in 2020 to USD 1,800 Million in 2025 (base year). Under current structural drivers and subject to the scenarios outlined below, our central forecast sees the market continuing to grow at a steady compound annual growth rate of 6.5% through 2032, reaching approximately USD 2,782 Million by the end of the horizon. The first forecast year (2026) begins at roughly USD 1,914.6 Million.

Cable Glands Market

This steady expansion masks important inflection points — regulatory tightening around hazardous-location approvals, accelerating electrification and infrastructure refresh cycles, and raw material price volatility — all of which change the economics for manufacturers, distributors and end users. Understanding these dynamics is essential for 2026 strategy setting.

Cable Glands Market

Why this matters for 2026 strategic decisions

- Portfolio investment and certification timing: Certification windows for ATEX/IECEx, UL/CSA and national approvals are multi-quarter projects that materially affect time-to-revenue. Firms that front-load certification programs in 2026 will capture premium, higher-margin projects in hazardous and regulated sectors.

- Supply-chain positioning: Brass, nickel-plating feedstocks, stainless alloys and engineered polymers dominate input costs. Fluctuating raw-material prices and trade-policy uncertainty mean 2026 is the year to operationalize hedging, dual-sourcing and regional buffer strategies.

- Channel and aftermarket monetization: As competition compresses product margins, service, testing, spare-parts, and extended-warranty offerings become meaningful margin levers. 2026 commercial models should shift from pure product sales to product-plus-service bundles.

- M&A and consolidation playbook: The market is moderately concentrated (CR3 ≈ 45%; CR5 ≈ 60%) — suggesting room for strategic acquisitions that can materially raise scale and fill product/certification gaps faster than organic investment alone.

Practical contents of the full PW Consulting report

Our full study is built to be operationally actionable. Key deliverables include:

- Comprehensive historical dataset (2020–2025) and an auditable forecast (2026–2032) with scenario variants for macroeconomic slowdown and accelerated infrastructure spend.

- Regulatory-impact model showing revenue sensitivity to certification delays and new standard adoption (e.g., CAN/CSA-C22.2 No. 60079-series and recent CSA compliance updates).

- Raw-material cost model linking brass, nickel, stainless and engineered polymer pricing to product-level gross margins.

- Go-to-market playbooks tailored for OEMs, distributors and private-label manufacturers — including channel economics, pricing levers, and aftermarket upsell mechanics.

- M&A screening tool: a ranked short-list of acquisition targets by strategic fit, integration complexity, and likely price bands (confidential annex).

- Operational playbook: recommended CapEx, test-lab investments, quality traceability, and supplier qualification procedures to reduce time-to-certification and warranty exposure.

- Commercial KPIs and dashboard templates suitable for executive review — order backlog, certification lead times, SKU-level margin, and exposure to raw-material supply shocks.

Competitive landscape — who to watch and why

The ecosystem includes multinational electrics and specialist manufacturers with differentiated technical and geographic strengths. Leading players such as Hawke International, HELUKABEL, ABB, Phoenix Contact, Lapp Group, Cembre and regional specialists (e.g., AerosUSA, CGS Cable Glands, CMP Products, Shanghai Weyer / Weyer Electric) form the competitive spine of the industry. Each brings different strategic assets:

- Hawke International (UK): recognized for Exd/Exe certified solutions for hazardous locations — a leader in product certification depth and hazardous‑area engineering.

- HELUKABEL (Germany): strong in both plastic and metal glands with focus on sealing and strain relief — a player to watch on product innovation and channel reach.

- ABB (Switzerland): global scale and cross‑portfolio integration; benefits from system-level contracting and global approvals footprint.

- AerosUSA (USA): niche supplier specializing in advanced polyamide technologies and lamellar solutions — representative of new material-led differentiation.

- Cembre & Phoenix Contact (Italy/Germany): known for premium metal glands and EMC solutions, serving demanding industrial segments.

- Lapp Group: global reach with SKINTOP® family; strong distribution and OEM relationships.

- Regional manufacturers (China, India, South Africa): cost-competitive producers with growing capability in higher-spec products and expanding export footprints.

Recent activity (June 2026) — trade-show visibility from AerosUSA, HELUKABEL and Lapp Group — underlines continued investment in product launch and channel engagement, with trade events serving as de facto product-testbeds for OEM and distributor partnerships.

Regulatory and standards developments shaping 2026 decisions

Regulation is a strategic variable, not just compliance cost. Key changes to monitor include national certifications for explosive atmospheres and updated compliance guidance (e.g., the CSA Certificate of Compliance for external connections in Zone 1/Div 2 from October 2025 and ongoing references to CAN/CSA-C22.2 No. 60079-series). Market leaders are those that internalize regulation as a product-development input — aligning R&D, test-lab investment, and certification roadmaps to new standards well ahead of procurement cycles.

Strategic moves with highest ROI in 2026

- Prioritize hazardous-area certifications: Implement a staged plan to secure ATEX/IECEx and national approvals for high-potential product families. The marginal revenue uplift for certified SKUs in regulated tenders is material.

- Product-to-service transition: Develop modular aftermarket offerings (testing, recertification, replacement kits) and embed them into distributor contracts to stabilize margins.

- Supply-chain hedging: Negotiate multi-year supply agreements for brass and nickel inputs with price‑escrow mechanisms or indexation clauses; qualify alternate polymer suppliers and regionalize critical components.

- Selective consolidation: Pursue tuck-in acquisitions to accelerate certification, add EMC- or hazardous-capable product lines, or secure local market access — faster and less risky than greenfield launches.

- Manufacturing modernization: Invest in test automation and digital traceability to compress time-to-certification and reduce recall risk from assembly defects.

- Channel analytics: Use distributor-level margin maps and demand forecasting to rationalize SKUs and reduce inventory carrying costs without sacrificing fill rates.

Risk map and scenario planning

Key downside risks for 2026 strategy:

- Raw-material shocks: Sudden spikes in brass or nickel prices can erode margins unless contracts include pass-through mechanisms.

- Delayed certifications: Postponed approvals create inventory obsolescence and lost bid opportunities with long sales cycles.

- Trade-policy disruptions: Tariff or export restrictions on specific alloys can re-route supply chains and increase landed costs.

Our report includes scenario worksheets that quantify P&L sensitivity across these risk vectors and prescribes mitigations that protect EBITDA at key breakpoints.

What we recommend executives do in Q1–Q2 2026

- Authorize a 6–12 month certification acceleration program for priority SKUs tied to specific revenue targets.

- Set up a raw-material procurement task force to renegotiate supplier terms with hedging and dual-sourcing targets.

- Run a 90‑day commercial pilot that bundles extended-service contracts with selected distributors to validate aftermarket willingness-to-pay.

- Shortlist acquisition targets that close capability gaps (e.g., EMC expertise, hazardous-area approvals, local manufacturing) and begin confidential outreach.

- Adopt a dashboard emphasizing order backlog by certification status, SKU-level margin, and supplier concentration to inform weekly executive reviews.

Closing — the strategic value of this study for 2026

For leaders planning resource allocation in 2026, this industry is predictable at the macro level — steady compound growth toward ~USD 2.78 Billion by 2032 — but deeply nuanced at the segment and compliance level. The difference between winning and losing will be execution: being first to certify priority SKUs, shoring up supply lines for key metals and polymers, and monetizing aftermarket services.

PW Consulting’s full Cable Glands Market report supplies the granular segment data, regional breakdowns, price-point matrices, and company share tables required to operationalize these strategic moves. If you require the modeled datasets, M&A target dossiers, and the certification‑timing playbook that underlie the recommendations above, please consult the full report for subscription access.

For detailed analysis of this topic, please visit the official page:Cable Glands Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com