Contact Image Sensor (CIS) Market 2026: Strategic Primer for Decision-Makers

As enterprises build roadmaps for 2026, the Contact Image Sensor (CIS) market presents a mix of steady expansion, concentrated competitive dynamics, and technology-regulatory friction that together demand calibrated strategies. This preview synthesizes the strategic signal from our full PW Consulting market study (base year 2025, historical 2020–2025, forecast 2026–2032) to help executives prioritize investments, partnerships, and product bets. It shows why CIS is no longer a niche component market: it is a predictable growth segment with specific inflection points that will shape procurement, R&D, and M&A choices over the next three years.

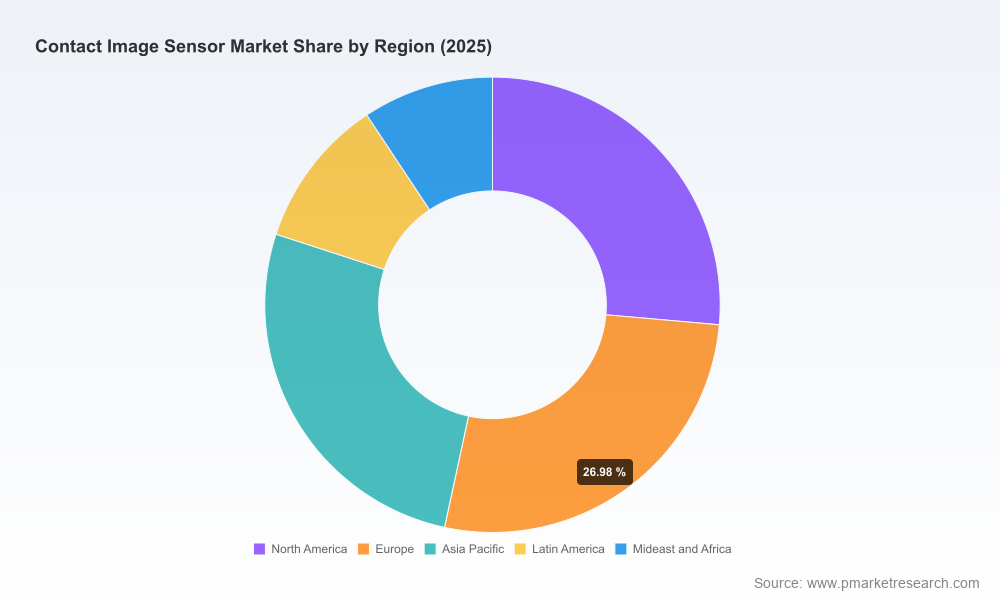

Contact Image Sensor Market

Macro trajectory: predictable growth, actionable timing

The CIS market has demonstrated steady expansion through the first half of the decade, growing from approximately USD 1,094.66 Million in 2020 to about USD 1,549.72 Million in 2025. Our forecast model — built on device adoption curves, OEM build plans, supply-chain visibility, and end-market demand scenarios — projects a compound annual growth rate (CAGR) of 7.2% for the 2026–2032 period, reaching roughly USD 2,521.25 Million by 2032. That combination of depth (long horizon) and predictability (mid-single-digit-plus CAGR) creates a clear window for investment discipline: capacity and product bets made in 2026 are likely to be cash-flow-relevant throughout the next decade.

Contact Image Sensor Market

Why 2026 is a strategic inflection year

- Capital deployment windows: The mid-decade growth profile creates opportunities to expand production lines or acquire niche technology without sacrificing near-term profitability. Our scenario work shows that incremental capacity added in 2026 benefits from multi-year demand tailwinds.

- Product differentiation becomes durable: As CIS features (e.g., higher DPI, HDR line rates, integrated CMOS ICs, and application-specific optics/illumination) become table stakes, differentiation will shift to integration, system-level calibration, and software-enabled inspection intelligence. Companies that finalize platform-level investments in 2026 can harvest prolonged IP and channel advantages.

- Regulatory and trade risk crystallization: Evolving export controls and standards (notably recent updates affecting high-precision sensors) require companies to bake compliance and alternative sourcing into 2026 supply-chain plans. Decisions made in 2026 on supplier qualification and geographic sourcing will determine exposure to export constraints over the following years.

What the PW Consulting report delivers (practical deliverables)

Our full study is designed as an operational playbook for executives who need to convert market insight into go/no-go actions. Key deliverables include:

Contact Image Sensor Market

- Market model and demand scenarios (2020–2032) with sensitivity to macro cycles, semiconductor capacity constraints, and end-market dynamics for scanning, machine vision, banking instruments, and document imaging.

- Down-to-component supply-chain mapping and vendor scorecards covering wafer sourcing, CMOS IC suppliers, optics/illumination partners, and contract manufacturing risk factors.

- Competitor benchmarking with product roadmaps, channel footprints, and margin proxy analysis to inform pricing and product bundling strategies.

- Deal playbook for M&A and partnerships: valuation heuristics, integration risk checklists, and prioritized targets by capability gap (e.g., high-DPI monochrome line sensors vs. color CIS modules with custom ICs).

- Commercial go-to-market templates: tiered customer segmentation, OEM value-propositions, sample-to-production timelines, and configuration-driven pricing models.

- Regulatory impact matrix and mitigation pathways, including dual-sourcing plans and relocation triggers tailored to recent export-control updates affecting precision measurement sensors.

The report emphasizes actionable outputs — not just charts — including templates, decision trees, and a short list of prioritized experiments that procurement, product, and corporate development teams can execute in 90–180 day sprints.

Competitive landscape: concentrated yet dynamic

The CIS market exhibits significant concentration at the top: the leading trio of providers accounts for a substantial share of industry revenues, and the top five capture an even larger majority. High concentration signals that incumbents have scale advantages in manufacturing, customer relationships, and system integration — but it also creates opportunities for focused challengers to win through narrow, high-value differentiation.

- Mitsubishi Electric Corporation (Japan) — Known for high-performance CIS modules paired with original CMOS sensor ICs and illumination suites, Mitsubishi has positioned its offering for surface inspection, copy machines, and banknote readers. The company’s announced transfer of CIS business to an affiliated entity with a planned production relocation (notice issued in April 2026) is a strategic move to optimize manufacturing footprint and customer continuity. For partners and competitors, this signals both potential supply-chain reconfiguration and a stable customer-supply commitment through the transition window.

- Teledyne DALSA (Canada) — With an AxCIS family focused on high-speed, high-resolution line-scan solutions, Teledyne continues to push technical performance at the intersection of machine vision and high-resolution scanning. A May 2026 product expansion introducing 1,800 dpi and extended-length models with higher line rates and HDR capabilities illustrates a clear push into applications that value throughput and resolution — such as semiconductor wafer inspection and battery manufacturing lines.

- CMOS Sensor Inc (United States) — A niche player specializing in custom-designed CIS modules, CMOS Sensor Inc serves use cases that need color imaging and application-tailored sensor customization. Its differentiation is in agility and bespoke engineering, making it a logical partner for OEMs requiring integration flexibility.

- FRAMOS GmbH (Germany) — FRAMOS integrates high-quality CIS modules into compact scanners and machine-vision systems, emphasizing electrical and optical compatibility for OEM embedded use. Its value lies in shortening OEM time-to-market through modular integration and specification support.

- ColorTrac (United Kingdom) — Focused on CIS-based large-format scanners, ColorTrac competes on system-level engineering and channel relationships in wide-format printing and document handling markets. Their route-to-market highlights the commercial importance of end-user serviceability and calibration support.

From an M&A perspective, the market structure suggests two viable approaches for potential acquirers: (1) tuck-ins to strengthen system-integration and software capabilities, and (2) larger strategic acquisitions to consolidate scale in high-margin segments. Both approaches require rigorous supply-chain and regulatory diligence.

Regulation and supply-chain risks — immediate considerations for 2026

Regulatory updates in major jurisdictions have begun to touch sensor technologies that can measure surfaces at sub-micron repeatability or provide specific levels of precision. For example, recent export-control updates include sensor categories that could influence where advanced CIS modules are manufactured and sold. Practically, CIS suppliers and buyers must:

- Map product features to export-control criteria and maintain a watchlist of feature changes that could trigger new controls.

- Implement supplier qualification that includes export-compliance clauses and alternative second-sourcing for critical components.

- Evaluate localized assembly or contract manufacturing options to preserve commercial access to sensitive markets while minimizing cost impact.

Supply-chain fragility is not theoretical. High-capex wafer supply, specialized optics, and narrowly qualified CMOS IC partners create single points of failure. Our report delivers a risk heat map and specific mitigations (e.g., inventory hedges, multi-year supply contracts, capacity options) that are immediately actionable for procurement teams during 2026 negotiations.

Practical strategic implications by player type

- OEMs and system integrators: Lock in platform roadmaps now. Prioritize supplier agreements that include co-development clauses and volume options to secure favorable pricing as the market grows through 2026–2028.

- Component suppliers and foundries: Consider targeted capacity expansions for CMOS ICs serving CIS applications, but structure expansion with demand triggers and off-take agreements to avoid overexposure.

- Private equity and corporate development teams: Look for tuck-ins that bring inspection software, AI-enabled defect detection, or optical module assembly capabilities. Valuation discipline is paramount given the concentrated incumbent landscape.

- Service and aftermarket providers: Invest in calibration and field-service capabilities; as systems move into high-precision inspection contexts, service contracts become a differentiated revenue stream.

How to use this preview

This article highlights the strategic contours you need to consider as 2026 planning cycles accelerate: a steady market CAGR (7.2% through our forecast horizon), a clear path to USD 2.5+ billion scale by 2032, concentrated competitors with distinct positioning, and regulatory/supply-chain vectors that can materially alter competitive advantage. The full PW Consulting report contains the granular models, scenario outputs, and playbooks referenced here — including supplier scorecards, pricing ladders, and an M&A target short-list designed to convert insight into near-term action.

Executives preparing budgets, product roadmaps, or M&A mandates for 2026 will find the detailed quantitative back-up and executable templates essential. Use the preview to align internal stakeholders on timing and risk tolerance; use the full report to lock in contracts, finalize capex plans, and prioritize integration targets.

Next steps

- For procurement and product teams: request the supply-chain heat map and vendor scorecards to commence supplier negotiations.

- For corporate development: review the M&A playbook and the prioritized capability gaps to refine acquisition criteria.

- For R&D and product strategy: examine the feature-to-compliance mapping and the product-roadmap templates to ensure future releases do not inadvertently trigger export restrictions.

PW Consulting’s full Contact Image Sensor Market study provides the datasets, models, and tactical deliverables you need to convert this strategic primer into executed plans. Access to the complete segmentation, forecasts per application and region, and the operational playbooks will enable precise 2026 decision-making. Contact our team to obtain the comprehensive report and the customized briefing tailored to your organization's role in the CIS value chain.

For detailed analysis of this topic, please visit the official page:Contact Image Sensor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com