Process Automation Market Expands with Increasing Adoption of SCADA, DCS, and PLC Solutions

Other |

2026-02-23 14:11:56

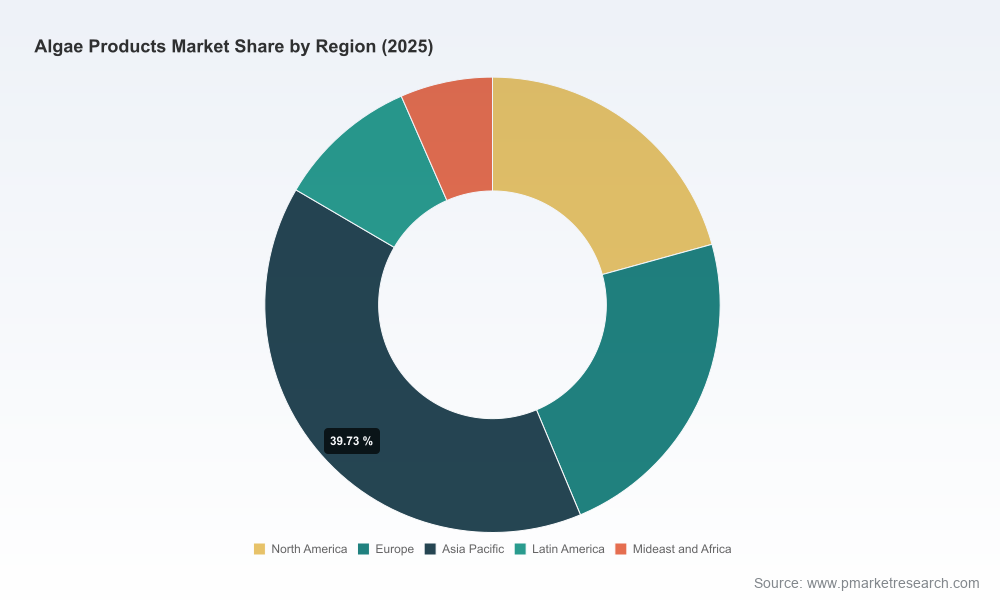

Between 2020 and 2025 the global algae products market moved from a niche, innovation-led space to a commercially material industry. Our analysis shows the market expanding from roughly USD 9,400 Million in 2020 to about USD 15,151 Million in 2025, and we project continued acceleration through the 2026–2032 forecast horizon. At a compound annual growth rate of 8.2% the market is set to exceed USD 26,300 Million by 2032. For executives planning capital allocation, product launches, or M&A in 2026, these macro trajectories are the baseline constraint and opportunity map: growth is substantial, durable, and sector-wide—but the winners will be determined by choices made this year.

Algae Products Market

Several converging forces make 2026 a watershed for companies operating across the algae value chain. First, regulatory clarity around algae-derived ingredients has advanced materially: additional chlorella and spirulina strains received GRAS recognition in the U.S. in 2025, while EFSA progressed novel-food approvals for algal omega-3 oils and phycocyanin colorants. At the same time, both EFSA and the United States Pharmacopeia tightened contaminant thresholds—raising the technical and compliance bar for producers and processors.

Algae Products Market

Second, technology and scale-up events have moved from pilot to commercial. Examples in the field include new high-throughput Spirulina cultivation facilities deploying AI, SCADA, robotics and zero-discharge systems; fermentation-derived culinary oils; and next-generation photobioreactor and heterotrophic processes for specialty lipids and pigments. Those advances compress the time to market for differentiated, cost-competitive products.

Algae Products Market

Finally, the demand-side momentum is robust. Health- and sustainability-conscious consumers increasingly prefer plant-based omega-3s, natural colorants, and protein alternatives; industrial buyers are re-evaluating supply chains to secure traceable, lower-risk sources; and aquaculture, nutraceuticals and food & beverage brands are all expanding their algae-derived product lines. The net result: demand is broadening across end markets while quality and regulatory traceability have become non-negotiable.

Each of the above elements is built to support a specific 2026 decision: whether to invest in capacity, launch an algal ingredient, enter a partnership, or reposition an existing portfolio. The report is organized around decisions—not datasets—and includes templates and KPIs for Board-ready investment cases.

The industry is moderately concentrated at the top: the three largest firms capture a substantial share of market revenue and the five largest account for a dominant portion. This concentration creates both barriers and opportunities: established players set quality standards and channel relationships, while mid-tier and emerging specialists create differentiation through niche products and process innovations.

Recent industry moves underscore two strategic themes: (1) regulatory progress and approvals are unlocking new commercial windows (e.g., approvals and partnerships in China for algae-based omega-3s; EFSA novel-food sign-offs), and (2) scale and automation investments (robotics-enabled Spirulina farms; fermentation-derived food oils) are shifting cost curves in favor of producers who can industrialize without compromising compliance and traceability.

Our Algae Products Market report is expressly structured to support three decision types common to 2026 planning cycles: (1) invest/greenfield decisions (full-capex models and scenario stress tests), (2) commercial development (product prioritization and route-to-market plans), and (3) M&A and partnership diligence (valuation comparators and strategic fit matrices). For each decision type we provide templates—financial, technical, and regulatory—so executives can translate market insights into executable initiatives without needing to rebuild the underlying models.

In keeping with the “trailer” approach to this market insight, this article highlights our methodological confidence and the strategic contours of opportunity and risk—but intentionally omits the granular, segment-level revenue schedules and regional splits that are needed to finalize financial commitments. Those detailed tables, sensitivities, and playbooks are included in the full report and model pack and are available through PW Consulting’s report portal.

The algae products market is no longer an experimental niche—it is an investable sector with clear growth pathways and defined technical barriers. The macro picture is compelling: from a USD 15.15 Billion base in 2025 to a projected USD 26.30 Billion by 2032 at an 8.2% CAGR. But success in 2026 will not be won on topline optimism alone. It will require disciplined regulatory strategy, selective scale-up investments, and commercial arrangements that bridge the technical supply base to large, risk-averse buyers.

For executives preparing capital allocation and commercial plans this year, the choice is straightforward: adopt an evidence-led approach that aligns product, process, and compliance, or cede early advantages to better-prepared incumbents. PW Consulting’s full Algae Products Market report delivers the granular inputs and decision templates needed to act with confidence in 2026.

For detailed analysis of this topic, please visit the official page:Algae Products Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com