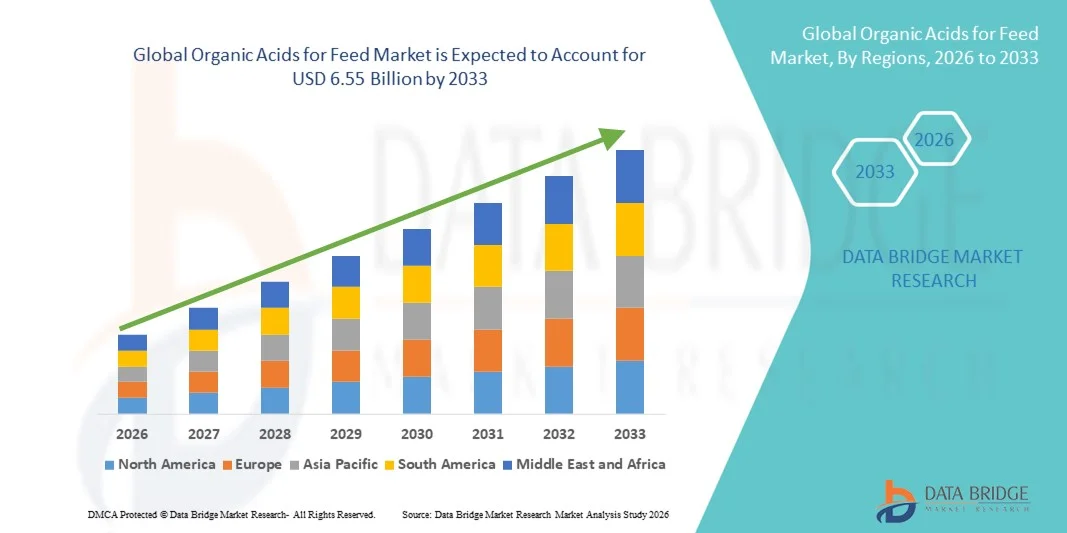

Organic Acids for Feed Market Share, Driving Trends, and Industry Forecast by 2033

Other |

2026-07-08 10:57:30

The lithium‑ion battery market has entered a new phase of accelerated expansion and structural change. After rising from a historical base in 2020, the market reached an estimated USD 325.77 Million in 2025 and is forecast to grow at a compound annual growth rate (CAGR) of 17.52% through the 2026–2032 projection window, reaching an anticipated USD 663.71 Million by 2032. These headline dynamics reflect a confluence of demand acceleration across transport and stationary storage, persistent raw‑material volatility, and a wave of capacity and technology investments from incumbent and emerging manufacturers.

Lithium Ion Battery Market

For executive teams making near‑term capital allocation, sourcing, product‑portfolio, or M&A decisions, 2026 is a pivot year: supply chains and regulatory frameworks are being rewritten while technology inflection points (notably high‑energy chemistries and solid‑state roadmaps) move from lab to pilot scale. This study translates macro momentum into actionable decision levers by combining a robust historical baseline (2020–2025) with detailed forecasts across the 2026–2032 horizon. The result is a pragmatic resource that helps leaders test strategic hypotheses under realistic market scenarios rather than rely on optimistic headlines or fragmented public disclosures.

Lithium Ion Battery Market

Demand momentum and scale-up: The market’s multi‑year rebound and the high mid‑teens CAGR through 2032 imply aggressive capacity expansions and faster technology conversion cycles. Companies planning plant builds, JV investments, or long‑term offtakes must align project timelines to avoid common mismatches between cell availability and OEM integration windows.

Lithium Ion Battery Market

Raw‑material pressure and sourcing risk: Lithium supply grew materially in 2025, with global production rising substantially and battery‑grade lithium carbonate experiencing upward price movement over the year. That combination creates a dual challenge—securing feedstock on commercial terms and designing chemistry strategies that reduce exposure to the most volatile inputs.

Regulatory and transport constraints: New operational constraints for lithium‑ion battery transport (including lower allowed state of charge for air freight effective from 1 January 2026) increase lead‑time risk for cross‑border supply chains and raise the effective landed cost of fast‑reaction inventory. At the same time, national standards (for example, formalized solid‑state battery development standards adopted in China in 2026) are accelerating the path to commercialization for next‑gen chemistries—creating both opportunity and competitive pressure.

Market structure and concentration: The competitive landscape remains moderately concentrated; the top three and top five manufacturers together account for a significant share of industry capacity. That concentration accelerates the importance of strategic partnerships and makes supplier selection a core source of competitive advantage or vulnerability.

Leaders need to translate macro forecasts into specific actions. Below are five high‑impact strategic moves that the research supports with data‑driven scenarios and tactical playbooks.

Prioritize upstream engagement: Hedge raw‑material exposure through direct sourcing, long‑dated offtakes, or vertical integration where unit economics and scale justify investment. Our modelling shows the sensitivity of project IRRs to lithium feedstock price swings and identifies the thresholds at which integration becomes value‑accretive.

Match capacity timing to OEM cadences: Build flexible capacity plans (module‑level or hybrid cell assembly) rather than rigid cell factories. The report includes scenario timelines mapping cell output to EV platform launch calendars so you can avoid inventory shortfalls or excesses.

Design for chemistry optionality: Invest in modular production lines that can accommodate multiple chemistries and form factors. With standardization forces and new solid‑state standards emerging, chemistry flexibility reduces stranded‑asset risk.

Use M&A and partnerships to fill capability gaps: Given the market concentration and recent transaction activity, targeted acquisitions or strategic JVs can accelerate access to proprietary cell formats, battery management systems, and local manufacturing footprints.

Embed regulatory compliance into logistics strategy: Air transport limitations on charged cells and evolving safety standards necessitate contingency plans for long‑lead or high‑value shipments. The report models the cost and lead‑time impact of alternative transport modes and inventory buffers.

Our competitive assessment synthesizes corporate profiles, capacity trajectories, product roadmaps, and recent public developments to create a forward‑looking picture of rivals and potential partners. Key incumbents remain diversified and vertically integrated, while several regional players are aggressively scaling to capture auto and stationary storage volumes.

CATL (Ningde, China): A dominant, vertically integrated producer with scope across materials, cells, and systems. Their scale and upstream positioning make them a pivotal price setter and a key partner/competitor depending on your strategic stance.

BYD (Shenzhen, China): Notable for its Blade LFP format and integration into its broader mobility portfolio. BYD’s emphasis on safety and lifecycle economics has reshaped demand for certain LFP variants.

LG Energy Solution and Samsung SDI (Korea): Global suppliers with strong OEM relationships and diversified cell formats. Recent contract and partnership activity demonstrates their push into system‑level BESS projects and next‑gen pack technologies.

Panasonic Energy (Japan/US): Strategic expansion in North America to serve regional automotive demand, with new factory starts influencing regional supply balances and logistics footprints.

Specialists and challengers (e.g., Envision AESC, EVE Energy, Gotion High‑Tech, SK On): Concentrated bets on prismatic or LFP formats and on tailored energy‑storage products. Several have launched large‑format BESS products and modular systems in 2026, signaling competition at both cell and system levels.

Recent illustrative developments that shape competitive dynamics include strategic BESS contracts, new product introductions, partnerships on cell and pack technologies, and announced capacity expansions. These discrete events matter because they alter local supply availability and accelerate product roadmaps—both central to win/loss outcomes in customer tenders and OEM supplier selections.

The full research package is built for practitioners and includes:

To honor the “trailer” principle—to demonstrate methodological rigor while reserving the proprietary sub‑segment tables, regional splits and detailed application forecasts for the full report—we have deliberately withheld the granular regional and application breakdowns in this introduction. Those detailed tables and downloadable data appendices are available in the complete report.

Board and investor briefings: Use the headline forecasts and scenario envelopes to stress test capital plans and to set realistic ramp milestones for any new cell or pack investments.

Procurement and contract strategy: Recalibrate supplier scorecards to reward flexibility and off‑takers with secure upstream access; consider hybrid contracts that mix spot exposure with fixed offtake volumes.

R&D and product roadmaps: Prioritize chemistry development workstreams that reduce reliance on the most volatile feedstocks while aligning with emerging standards for safety and density.

M&A diligence: Apply our concentrated competitive metrics and downside scenarios to price targets and integration plans, focusing on technology fit and footprint synergies rather than headline capacity.

2026 will be a year of tactical urgency and strategic repositioning. The market’s strong growth trajectory and ongoing structural shifts demand that senior teams move beyond intuition to data‑backed scenario planning. Our research provides the forecast framework, supplier and competitor intelligence, and executional toolkits to convert growth into durable value. For the granular regional, chemistry‑level, and application split tables that drive procurement decisions and capital sizing, consult the full report where those proprietary datasets and interactive models are published.

For detailed analysis of this topic, please visit the official page:Lithium Ion Battery Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com