Intelligent Emergency Warning Lights Systems Creating New Growth Opportunities Worldwide

Other |

2026-05-15 11:29:00

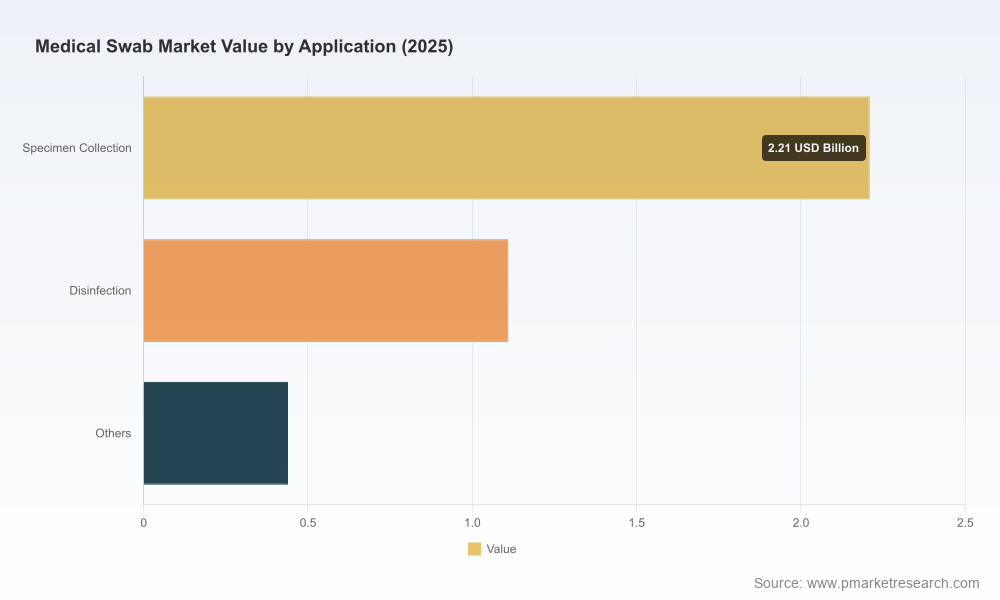

The medical swab market has moved from pandemic-era volatility into a maturation phase characterized by steady, demand-driven growth and rising regulatory scrutiny. Our PW Consulting market model shows the global market expanding from USD 2.15 Billion in 2020 to USD 3.76 Billion in the base year 2025, with continued growth anticipated into the next decade—reaching an estimated USD 6.17 Billion by 2032. Across the 2026–2032 forecast window the market is expected to grow at a compound annual growth rate (CAGR) of 6.98% (USD, Billion basis). For corporate leaders planning capital allocation, manufacturing footprint, or M&A activity in 2026, these macro dynamics shape a pragmatic but opportunity-rich strategic landscape.

Medical Swab Market

A stabilized market trajectory: Post-2024 normalization has given way to reliable expansion rather than episodic spikes. That predictability allows organizations to move from crisis-mode contingency to disciplined capacity investments—if they align with validated demand scenarios and regulatory pathways.

Medical Swab Market

Regulatory regimes are reshaping product and manufacturing requirements. Recent FDA activity—from recall enforcement to evolving oversight of laboratory-developed tests and at‑home diagnostic authorizations—means product-spec, validation, and quality-system investments are no longer optional. The firms that operationalize compliance early will avoid costly recalls, protect brand equity, and secure preferred vendor positions with large buyers.

Medical Swab Market

Margin and concentration dynamics are nuanced: market concentration metrics show mid-level consolidation, producing pockets of scale advantage for established players while creating niches for specialized manufacturers and regional suppliers. This creates distinct pathways to value capture through premiumization, service bundling (e.g., validated transport systems), or cost leadership.

Quality and regulatory proof points as competitive currency. The market is no longer won solely on price. FDA clearances, ISO 13485 certification, validated compatibility with high-throughput diagnostic platforms, and demonstrated contamination-control processes increasingly determine preferred-supplier lists for hospitals, labs, and consumer OTC channels.

Product-system thinking over commoditized SKU management. Suppliers who pair swabs with validated transport media, rapid inactivation technology, or packaged workflows for at‑home collection can command higher margins and deeper commercial relationships. Recent product launches that emphasize integrated collection and preservation have already shifted procurement conversations.

Supply-chain resilience and raw-material visibility. Cotton, non-woven substrates, and sterile manufacturing capacity are established inputs with historic exposure to surge-driven shortages. Buyers and manufacturers who secure diversified upstream sources, invest in inventory buffers, or near‑shore critical steps reduce service-risk premiums and win long-term contracts with health systems and government purchasers.

Channel evolution: clinical labs, hospitals, and growing OTC/home-testing segments require distinct commercialization approaches—ranging from direct technical support and validation services for labs to retail packaging, usability validation, and consumer education for OTC products.

Our competitive review synthesizes capabilities across established multinationals, specialized manufacturers, and regional producers. Notable profiles include manufacturers with deep sterile‑goods portfolios and diagnostic integrations (e.g., Puritan Medical Products, Copan Diagnostics, BD) as well as diversified healthcare suppliers and regional producers who serve wound care and clinical consumables channels. Market concentration indicators reveal a field where leading firms capture meaningful share but where nearly half of the market remains accessible to smaller or niche players who execute on quality, speed, and validated partnerships.

Puritan Medical Products: Strengths lie in vertically integrated sterile manufacturing and recent innovation in collection/transport systems that emphasize rapid inactivation and preservation—differentiators for diagnostic OEMs and government procurement.

Copan Diagnostics: Known for flocked-swab technologies with strong validation narratives, positioning it as a go‑to partner for microbiology and molecular diagnostics platforms.

BD and other global diagnostics players: Provide complementary scale, platform validation breadth, and established procurement relationships—critical for contract wins with large laboratory networks and health systems.

Regional and emerging manufacturers: Offer cost advantages and local supply redundancy, but must invest in quality systems and regulatory documentation to expand into higher-value diagnostic supply chains.

Elevated recall sensitivity: Recent FDA recall actions linked to contamination risks underscore the operational and reputational impact of lapses in sterile control. For manufacturers this raises the priority of microbial monitoring, batch traceability, and post-market surveillance investments.

LDT oversight and diagnostic authorization shifts: Proposed regulatory changes affecting laboratory-developed tests and the authorization processes for at‑home diagnostics materially change customers’ procurement requirements; suppliers must demonstrate equivalence or gain explicit approvals for use in those workflows.

At‑home testing channel requirements: OTC product approvals now commonly stipulate approved swab types or validated equivalents, driving demand for co‑development agreements between swab manufacturers and diagnostics firms.

This market brief is accompanied by a full PW Consulting report built for executives who need executable insights rather than academic summaries. Deliverables include:

A demand model spanning 2020–2032 with scenario runs (base, conservative, upside) that translate epidemiological possibilities, diagnostic adoption curves, and at‑home testing penetration into procurement volumes and revenue outlooks.

A supplier capability map and maturity assessment across quality systems, regulatory approvals, manufacturing footprint, and product-system offerings—designed to inform sourcing decisions and M&A screening.

A regulatory action playbook aligned to current FDA trends, outlining step‑by‑step actions to secure clearances, maintain market access for LDT-linked channels, and to reduce recall risk through targeted investments.

Commercial-play templates for three buyer segments (clinical lab networks, hospital systems, and OTC/retail), including pricing levers, validation support packages, and account penetration tactics.

A 12–24 month operational checklist for suppliers—from raw-material sourcing and redundancy planning to traceability upgrades and bioburden control measures—that maps to cost and timeline estimates for capital and process changes.

For manufacturers with scale: accelerate development of integrated collection/transport systems and pursue platform-level validations with diagnostic OEMs. This protects margins and creates sticky commercial relationships in a market where product differentiation matters.

For regional and cost‑focused players: prioritize ISO 13485 upgrades, third‑party validations, and targeted capacity investments that can be quickly certified. These moves unlock access to higher-margin diagnostic channels without requiring transformational R&D budgets.

For distributors and hospital procurement leads: rebuild multi‑sourced supply ladders with explicit redundancy clauses and quality KPIs. Expect premium pricing for guaranteed, validated supply in contracting cycles through 2027.

For private equity and corporate development teams: identify roll-up targets that combine manufacturing assets with regulatory‑validation capabilities. Market concentration metrics point to consolidation potential where buy-and-build can create national or platform-scale suppliers.

With the market forecast exhibiting a 6.98% CAGR through 2032 and predictable year-on-year growth from a USD 3.76 Billion base in 2025, organizations should integrate three levers into 2026 planning: timing of capacity expansion (phased to demand scenarios), prioritization of quality/regulatory spend (front-loaded to prevent interruption), and portfolio differentiation (systems and validation over SKU volume). Combining these levers produces defensible revenue growth while managing downside recall and regulatory risks.

This introduction outlines the high-level trajectories, competitive contours, and regulatory forces that will shape medical swab markets in 2026. The full PW Consulting report provides the granular, actionable intelligence—validated demand curves by use-case, a verified supplier capability index, and deal-ready M&A screens—required to convert these strategic imperatives into executed initiatives. In short: we show not only what is changing, but exactly how to act in procurement, manufacturing, regulation, and commercial strategy to capture growth while minimizing risk. For decision-makers preparing budgets and bids in 2026, that operational specificity is the difference between following the market and leading it.

For detailed analysis of this topic, please visit the official page:Medical Swab Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com