How Artificial Intelligence Is Transforming Modern Recruitment Processes Worldwide

Other |

2026-02-04 08:27:50

As companies position for performance and resilience in 2026, hexagonal boron nitride (h-BN) is no longer a niche ceramic intermediate — it is an enabling material for thermal management, advanced coatings, and high‑temperature lubrication across electronics, automotive electrification, and industrial processing. PW Consulting’s latest market study (base year 2025, historical 2020–2025, forecast 2026–2032) synthesizes primary research, proprietary modelling, and on-the-ground interviews to translate this technical material market into executive-grade, actionable intelligence. The study projects a compounded expansion through the forecast window at a 4.71% CAGR, reflecting steady demand growth together with episodic market dynamics that will shape supplier strategies and investment timing.

Hexagonal BN Market

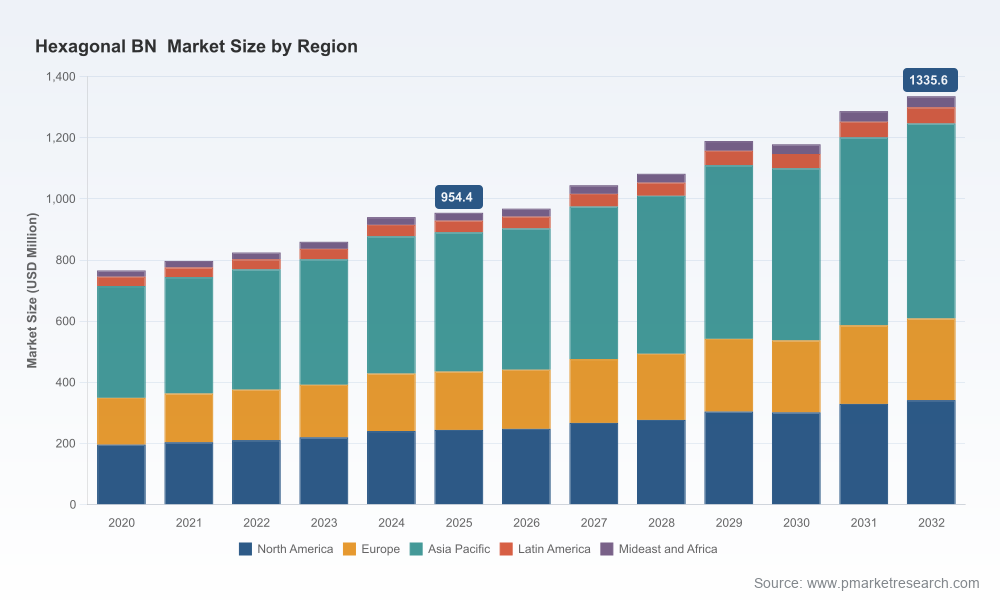

A maturing market scale: h-BN’s market value has expanded meaningfully over the past half-decade — rising from under USD 800 Million in 2020 to just under USD 1 Billion by 2025 — and is forecast to continue increasing through 2032. That trajectory converts technical trends (e.g., power electronics cooling, LED reliability, advanced coatings) into financial planning inputs for procurement, R&D budget allocation, and capacity investment.

Hexagonal BN Market

Policy and feedstock dynamics are shifting supply economics. In late 2025, boron was added to the United States’ list of critical minerals, accelerating incentives for onshore production and supply-chain resilience. Concurrently, US import unit values for boron showed downward movement in 2025, providing near-term feedstock relief for manufacturers. The combination of strategic support and lower feedstock friction alters payback calculations for domestic fabrication and vertical integration.

Hexagonal BN Market

Supplier concentration is material: the market exhibits a clear leader cluster—our concentration metrics show the top three players account for a majority share of the market, with the top five holding nearly two‑thirds. That structure creates a delicate balance between price-setting ability at the incumbent level and attractive consolidation or niche-play opportunities for challengers.

Forecast nuance that matters to planners: while growth through the 2026–2032 window is positive on average, the PW forecast embeds non-linearities and short cycles driven by technology adoption waves and inventory adjustments in adjacent industries. Treat headline CAGR as directional; use scenario outputs in the full report for capex phasing and contract negotiation timing.

Robust market sizing and demand modelling: build budgets and sales targets with a verified market base (2020–2025) and high‑granularity demand drivers through 2032. Our models allow you to toggle end‑market penetration assumptions (e.g., EV power modules, LED packaging, specialty coatings) to test upside and downside cases.

Price and cost-stack scenarios: assess margin resilience with feedstock price sensitivity runs that reflect recent boron import dynamics and potential policy incentives for domestic production. These scenarios let procurement and finance teams stress-test supplier bids and internalizing strategies.

Supply‑chain heatmaps and risk scoring: granular supplier mapping, logistics choke‑point diagnostics, and a ranked list of mitigations (dual‑sourcing, near‑shoring, inventory buffers, strategic contracts) prioritized by cost-to-implement and risk-reduction potential.

Commercial playbooks for growth and defense: go-to-market templates tuned to customer archetypes (e.g., consumer electronics OEMs, industrial adhesives formulators, metalworking tool makers) including differentiated value-prop messaging and tiered pricing approaches.

M&A and partnership scanner: target lists and valuation heuristics for inorganic plays, including vintage EBITDA multiples observed in relevant specialty materials transactions and quick diagnostics to identify bolt-on versus transformative acquisitions.

Regulatory and incentives dossier: country‑level policy tracking and incentive maps that quantify the potential grant/tax benefits from critical mineral designations and domestic manufacturing support — input directly usable in investment NPV models.

The market is anchored by established chemical and materials companies, specialist powder producers, and coatings experts. Key industry participants include large diversified materials firms with global manufacturing footprints, regional powder specialists, and innovative suppliers of 2D films and monolayers. Each class of player brings distinct strategic implications:

Large diversified players (incumbent chemical majors and industrial conglomerates) offer scale, integrated supply chains, and multi-channel distribution. Their strength is negotiating leverage and rapid global delivery, which can limit price volatility for high-volume OEMs.

Specialist powder and coating firms provide technical depth and product customization for high-performance applications — an area where formulation partnerships and co-development agreements can accelerate product adoption in premium segments.

Technology-oriented entrants (e.g., 2D film and CVD specialists) are the most likely catalysts for disruptive application growth, particularly in semiconductor and next‑gen electronics packaging where monolayer quality and consistency matter.

PW’s company dossiers include profiles, capability maps, and strategic posture assessments for each major supplier — enabling buyers and potential investors to align supplier selection with seven defined archetypes (e.g., scale leader, boutique innovator, regional champion). The study also quantifies market concentration: the three largest suppliers account for a material majority of market share, and the five largest approach two‑thirds market share—facts that shape negotiations, competitive response, and consolidation strategies.

Procurement: negotiate multi-year supply contracts with indexed price collars combined with volume flexibility clauses. With boron supply dynamics improving and policy incentives emerging, flexible long-term deals that include feedstock pass-through mechanics will mitigate price risk while preserving upside for suppliers.

Manufacturing footprint: evaluate near‑shoring or regional micro‑plants for high-value, time‑sensitive applications. The combination of critical mineral status and supply‑chain geopolitics makes localized capacity economically rational for firms with high service-level requirements.

Product strategy: prioritize R&D investment where h-BN delivers differentiated system-level performance (e.g., high-power density thermal interfaces, high-temperature non-stick coatings). Complement product innovation with IP protection and co-development partnerships to expedite adoption.

M&A and partnerships: pursue bolt-on acquisitions to secure feedstock processing, or technology licensing deals with CVD/2D specialists to access semiconductor adjacencies. Consolidation opportunities are present where regional specialists supply fragmented end-markets.

Risk management: adopt a layered approach that combines alternate feedstock sourcing, modest strategic inventory, and supplier development programs to reduce single‑source exposure. The PW playbook supplies a prioritized implementation timeline calibrated to cost and risk reduction.

The study’s base year is 2025, and our historical window spans 2020–2025. Forecasting covers 2026–2032 and was built on a hybrid approach: bottom‑up demand modeling per end‑use, supplier capacity mapping, and top‑down macro alignment. Inputs include company financials, customs and trade data, end‑market technology adoption rates, supplier interviews, and policy trackers. Price and cost models incorporate recent boron import price movements and refined borax volume stability, as reported by public agencies. We stress‑test every scenario with sensitivity runs to feedstock, production utilization, and application penetration rates, producing a range of outcomes rather than a single deterministic path.

This article is a strategic preview: it demonstrates PW Consulting’s proprietary modeling and market judgment but intentionally omits the granular sub‑segment tables, regional share matrices, and downloadable price-model spreadsheets that corporate teams need to execute. Clients and subscribers can access the full dataset, interactive forecast model, and supplier scorecards on the report landing page. For teams preparing budgets, negotiating supply contracts, or evaluating M&A through 2026, the full report provides the numerical fidelity and scenario analytics required to move from strategy to execution with confidence.

Contact PW Consulting for an executive briefing and model walkthrough: we will align the study’s scenarios to your product mix, margin targets, and operational constraints — helping you to convert material science momentum into measurable commercial advantage in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Hexagonal BN Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com