Chilled Meat Market Growth Analysis

Food |

2026-06-10 15:24:53

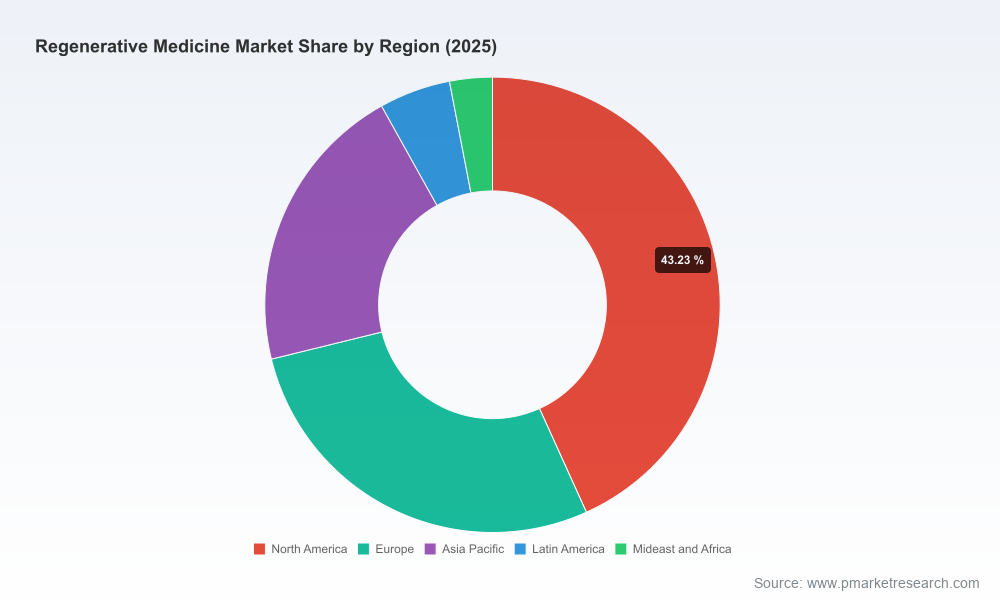

The regenerative medicine sector has moved beyond promise into sustained commercial scale. Our new market study synthesizes five years of historical performance and a seven‑year forecast to deliver a rigorous, investment‑grade view of value creation through 2032. The headline: the global regenerative medicine market expanded from about USD 12.5 Billion in 2020 to USD 30.0 Billion in 2025 and is projected to accelerate to roughly USD 125.0 Billion by 2032 — a compound annual growth rate of approximately 22.5%. For 2026, our base‑case projection sees the market breaking past the USD 35–40 Billion threshold, reaffirming that companies must decide now whether to double down, pivot, or selectively partner to capture outsized returns.

Regenerative Medicine Market

Timing is critical: with regulatory accelerators and a string of landmark approvals in 2025–2026, firms that align clinical, CMC and commercial strategies in 2026 will secure first‑mover advantages in durable, high‑margin indications.

Regenerative Medicine Market

Risk‑reward clarity: our forecast quantifies the pace of commercialization and the capital intensity of scale‑up, enabling boardrooms to compare the returns on manufacturing investment, licensing, or M&A alternatives against a common set of assumptions.

Regenerative Medicine Market

Operational readiness: the shift from bespoke, patient‑specific workflows toward hybrid platforms (where feasible) creates windows to compress time‑to‑revenue — but only for organizations that act on supplier, talent and regulatory levers now.

Market sizing and scenario forecasts (base, upside, downside) covering 2026–2032 with sensitivity to pricing, reimbursement uptake, and manufacturing scale economics.

Competitive dashboards that chart strategic positioning, late‑stage pipelines, and commercial footprints for the leading firms in the space.

Regulatory pathway maps and playbooks: accelerated program eligibility, CMC expectations, and comparator strategies for pivotal filings.

Manufacturing cost models and unit economics: batch cost drivers, capital intensity, and break‑even analyses for autologous versus allogeneic approaches.

Reimbursement and commercial launch frameworks: HTA evidence packages, payer negotiation strategies, and value‑based contracting templates.

Supply‑chain risk matrices and sourcing playbooks addressing import dependencies, cold‑chain constraints, and single‑source vulnerabilities.

M&A and partnership screening: scoring tools to prioritize targets and structuring approaches to capture technology and capacity quickly.

The market is already concentrated at the top, with established biopharma and medtech players occupying strategic niches across cell, gene and tissue engineering. Leading pharmaceutical firms and specialized regenerative companies are taking differentiated routes to scale: some prioritize proprietary, high‑value autologous and gene therapies; others double down on off‑the‑shelf allogeneic platforms or tissue‑engineered products for high‑volume applications. Notable players under continuous watch include:

Novartis AG — a pioneer in autologous CAR‑T and gene therapy platforms; recent label expansions underscore a strategy of lifecycle extension and indication broadening.

Gilead Sciences — focused on commercializing CAR‑T franchises and optimizing manufacturing throughput for blood‑cancer indications.

Bristol‑Myers Squibb — leveraging cell and gene assets within oncology and specialty care to build integrated franchises.

Astellas Pharma — concentrating R&D on cardiovascular and orthopedic regenerative therapeutics where clinical pathways and reimbursement levers are evolving rapidly.

Smith+Nephew and Integra LifeSciences — incumbents in tissue‑engineered products and matrices, emphasizing hospital partnerships and procedural adoption.

Pfizer, Amgen — large biopharma leveraging balance sheets to enter gene and cell therapy spaces via internal programs and targeted acquisitions.

Specialists such as Organogenesis, Mesoblast, Vericel, and Cook Biotech — continuing to commercialize differentiated cellular and biologic matrices in wound care, musculoskeletal, and surgical applications.

Market structure matters: the top three firms account for a significant share of the market’s revenue base and top five concentration is higher still, creating both competitive barriers and potential consolidation opportunities for mid‑sized innovators.

Regulatory momentum: recent guidance and policy shifts from major regulators have lowered certain development frictions. Notably, draft and final guidances released in late 2025 and early 2026 expand expedited pathways and offer increased flexibility on CMC expectations for cell and gene therapies — a structural change that materially shortens clinic‑to‑market timelines for programs that meet evidentiary thresholds.

Reimbursement headwinds: high upfront costs and heterogeneous payer frameworks remain a gating factor. Adoption will hinge on value demonstration, innovative financing (outcomes‑based, annuity models), and early HTA wins in select markets.

Supply‑chain fragility: roughly one‑third of manufacturers rely on imported starting materials. Small‑batch, time‑sensitive workflows amplify exposure to shipments, customs delays and single‑supplier outages.

Labor and manufacturing cost intensity: cell therapy batch costs are markedly variable and driven by labor, cleanroom utilization and process automation; organizations should expect per‑batch labor costs to span wide ranges and plan accordingly when comparing autologous versus scalable allogeneic models.

Clinical and commercial milestones: 2025–2026 saw important approvals and regulatory milestones, including nonprofit and public‑sector dossiers that demonstrate alternative sponsorship models, reinforcing that diverse development pathways can reach approval when evidence and program design are aligned.

Rationalize your portfolio now. Use our scenario models to re‑score programs by time‑to‑market, capital intensity and real‑world outcome potential. Deprioritize long‑tail, low‑value projects and accelerate those with clear payer pathway and manufacturing scalability.

Invest selectively in capacity that offers optionality. Rather than blanket heavy CAPEX, favor modular, regional manufacturing nodes, strategic toll‑manufacturing partnerships, and convertible cleanrooms to manage utilization risk.

Lock down the supply base and logistics playbook. Dual sourcing, near‑shoring core inputs, and investing in cold‑chain redundancy materially reduce time‑to‑treatment risk for autologous workflows.

Engage regulators and payers early. Leverage expedited pathways where appropriate, and build payer evidence packages concurrently with late‑stage development to compress launch timelines.

Pursue acquisition and alliance pathways that fill capability gaps. For many firms, buying manufacturing capacity or partnering for commercialization will deliver faster returns than in‑house greenfield builds.

Tailored market and revenue models aligned to your pipeline and strategy scenario (multi‑scenario outputs for board‑level decision making).

CMC readiness assessments and regulatory playbooks mapped to current FDA/EU expectations and the latest guidance updates.

Manufacturing and cost optimization engagements, including unit‑cost modelling, CAPEX/opex tradeoffs, and supplier risk mitigation plans.

Commercial and reimbursement launch blueprints — payer evidence strategies, contracting templates, and HTA submission readiness.

M&A target screening and integration roadmaps designed to accelerate capability acquisition without overpaying for execution risk.

We designed this study to be a decision‑grade tool for leadership teams entering a pivotal year. It combines a transparent forecast (2026–2032), competitor mapping, regulatory and reimbursement intelligence, and operational playbooks — all calibrated to the real‑world constraints of manufacturing and market access.

If your 2026 strategy will be judged on speed, quality of evidence and scalability, this market study provides the frameworks and scenarios to act with conviction. For the granular segment‑level revenue breakdowns, company scorecards, and the full suite of model outputs that underpin our recommendations, please consult the full PW Consulting report and data pack on our website.

For detailed analysis of this topic, please visit the official page:Regenerative Medicine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com