Data Center Power Market Trends in Intelligent Power Systems

Other |

2026-04-06 07:11:20

As companies plan capital allocation, supply-chain restructuring, and product roadmaps in 2026, understanding where the nanocrystalline soft magnetic materials market is headed is no longer optional — it is foundational. This preview synthesizes PW Consulting’s latest industry-level findings and strategic translations to help executives prioritize choices this year. We show the market trajectory, the structural forces reshaping supplier economics, and the tactical playbook leaders must consider — while reserving the granular segment-by-segment tables and detailed scenario appendices for the full report.

Nanocrystalline Soft Magnetic Material Market

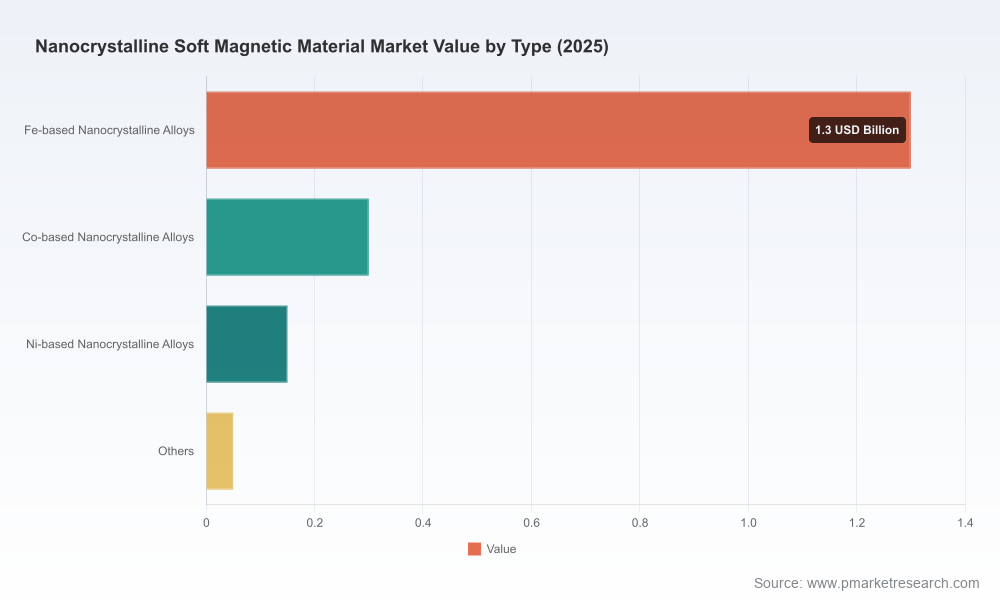

The nanocrystalline soft magnetic materials market has moved from niche to growth engine over the past half-decade. From a base around the early-2020s, industry revenues increased steadily through 2025, reaching approximately USD 1.8 Billion in the base year. Looking ahead under our central-case assumptions, the market is forecast to grow at a compound annual growth rate of roughly 9.2% across the 2026–2032 forecast window, reaching an estimated USD 3.34 Billion by 2032.

Nanocrystalline Soft Magnetic Material Market

Two framing observations matter for 2026 planning. First, the market is large enough to justify dedicated sourcing and R&D strategies for medium and large manufacturers, yet still exhibits pockets of supplier-led advantage where technology, process quality, and upstream access to specialty inputs create defensible positions. Second, the growth profile is robust and front-loaded: the market is transitioning from steady adoption in power-electronics and transformer segments into a broader set of industrial and mobility use-cases, which creates both immediate demand pressure and optionality for product-line extensions.

Nanocrystalline Soft Magnetic Material Market

Capital allocation decisions — The growth rate and mid-term market size justify selective capacity investments now, but those investments must be granularly staged. Firms that overcommit to commodity ribbon production risk margin erosion; those that invest in high-purity processing, tailored core assemblies, and converter-grade laminates stand to capture value.

Supply-chain positioning — Critical upstream inputs continue to be a constraining factor. Heightened raw-material costs and supply concentration for certain specialty oxides and alloying agents have been persistent industry dynamics. Securing long-term supply arrangements, qualifying alternate chemistries, or vertically integrating into key inputs are strategic levers worth evaluating in 2026.

Customer segmentation and route-to-market — As demand broadens across power-electronics, utility-scale conversion, and industrial automation, the winners will be those that align product form-factors (ribbons, tape-wound cores, assemblies) with targeted OEM procurement cycles and total-cost-of-ownership narratives.

Our Dynamics chapter synthesizes supply, demand, regulatory, and input-cost drivers that will dominate boardroom agendas in 2026:

Input-cost pressure — High raw material and processing costs continue to restrain margins. Firms will need to model sensitivity to alloy input volatility and evaluate hedging, index-linked contracts, or design changes that maintain performance while reducing rare input intensity.

Supply security moves — Leading material producers are pursuing strategic alliances and MoUs with upstream suppliers of critical oxide chemistries. These arrangements are emerging as a competitive moat: controlling high-purity input flows materially shortens lead times for advanced nanocrystalline alloys.

Consolidation and concentration — The market displays moderate concentration among primary producers, with a clear top-tier group capturing a significant share of advanced material output. This creates both opportunities for partnerships and risks for smaller players facing procurement pressure from OEMs seeking scale and reliability.

Regulatory and environmental considerations — Processing steps for some nanocrystalline materials have energy- and emissions-intensive phases. Increasing scrutiny on manufacturing footprint and recyclability is making environmental performance a procurement filter for large buyers.

Our competitor profiles go beyond public claims to analyze capability stacks, go-to-market reach, and recent strategic moves. The market’s leading players can be grouped by their strategic orientation — primary material innovators, specialized processors, and contract fabricators — each with different implications for partners and acquirers.

Primary innovators — A small set of companies has historically driven materials science innovation and maintains strong IP and product recognition in high-frequency and power-electronics applications. These firms remain pivotal because their material grades set performance baselines for OEM designs.

Regional manufacturers and processors — Several manufacturers focus on regional supply, customized cores, or ring assemblies and have gained traction through customer intimacy and rapid customization. Their agility is an asset for OEMs seeking faster design cycles.

Fabricators and assemblers — Companies that convert ribbon into tape-wound cores, or that integrate cores into assemblies, occupy an essential role in the value chain. They offer the scale and configuration know-how that many OEMs need without investing upstream.

Notable strategic moves underline these dynamics. In late 2025, a leading European producer signed a memorandum of understanding to secure high-purity oxide supplies — a defensive and offensive step to protect alloy processing pipelines. In 2025–26, a capacity expansion and subsequent facility commissioning by a major regional manufacturer demonstrates how the mid-tier is professionalizing and scaling to serve large OEM contracts. Together, these developments emphasize that securing upstream inputs and expanding reliable capacity are active strategic levers — and not hypothetical scenarios.

PW Consulting’s full market study is built as an operational toolkit for executives rather than an academic exercise. Key deliverables include (high-level descriptions):

Demand-supply model with scenario analysis — A dynamic model that maps demand by end-use classes under multiple macroeconomic and technology-adoption scenarios, showing stress points and surplus windows through 2032.

Supplier and input-risk heatmap — A prioritized list of critical upstream inputs, supplier concentration metrics, and mitigation options (dual-sourcing, strategic stockpiles, backward integration playbooks).

Go-to-market and product prioritization matrix — Decision frameworks for selecting which product forms and grades to scale first, aligned to customer procurement cycles and margin pools.

M&A and partnership playbook — A transaction-ready map showing which capabilities to buy vs. partner for, valuation benchmarks, and integration risk checklists.

Procurement negotiation briefs — Template contracts, negotiation levers specific to rare-oxide supply, and clauses to protect against price and availability shocks.

Regulatory and sustainability action plan — Guidelines to reduce processing emissions, improve end-of-life recyclability of cores, and prepare for buyer-side ESG screening.

These components are designed to be implementable: worked examples, executive checklists, and templated board-ready slides are included in the full deliverable to accelerate decision execution in 2026.

Prioritize upstream security — Immediately assess exposure to specialty oxide supply and pursue at least one medium-term securing action (e.g., forward contract, strategic alliance, or co-investment) within the fiscal year.

Stage capacity investments — De-risk capital deployment by phasing investments with technology gating milestones (e.g., pilot throughput, loss-performance validation) and supplier qualification gates.

Lean into customization for high-value OEMs — Target early engagements where nanocrystalline performance enables system-level advantages (power density, efficiency), using co-development incentives to lock design wins.

Assess M&A selectively — Use M&A to fill capability gaps (processing, assembly, specialty alloy access) rather than to chase volume. Prioritize targets that immediately improve margin profile or input control.

Operationalize sustainability — Embed energy efficiency and material recycling requirements into new facility designs; this both reduces operating risk and meets buyer-side ESG thresholds increasingly seen in procurement RFQs.

We help clients convert the market-level view into executable 12–36 month plans: from rapid due diligence on a target plant to designing contractual terms for long-term oxide supply. Our engagement options include scenario-driven strategy sprints, full commercial due diligence, and procurement playbooks tailored to the client’s position in the value chain.

Note: This preview highlights the macro trajectory, competitive themes, and recommended strategic moves, but intentionally omits granular segment-level revenue breakdowns and proprietary scenario tables. Those inputs — including granular regional and application splits, detailed CR-by-segment, and downloadable financial models — are available in the full PW Consulting report and data package.

Download the full market study to access the segment-level models, supplier scorecards, and executable templates referenced above.

Schedule a 60-minute strategy briefing with our nanocrystalline practice to translate findings into a bespoke 90-day action plan for your organization.

In a market growing at roughly a mid-single-digit-to-double-digit mid-term pace and reshaped by supply security initiatives and capacity moves, 2026 will be a year of choices that have multi-year consequences. Companies that combine measured capacity plays, upstream security, and focused product differentiation will convert current growth into durable, higher-margin positions. PW Consulting’s full study provides the instruments and the diagnostics to do precisely that — the preview above points to the why and the what; the full report supplies the how.

For detailed analysis of this topic, please visit the official page:Nanocrystalline Soft Magnetic Material Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com