Spray Dryer Market — Strategic Imperatives for 2026 Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present an executive preview of our Spray Dryer Market research — a tactical briefing designed to shape decisive action in 2026. The market for spray drying equipment and integrated services is no longer a niche engineering conversation: it is a multisector strategic battleground where regulatory shifts, capital intensity, energy dynamics, and technology differentiation determine winners and losers. Our analysis synthesizes historical performance (2020–2025, base year 2025) and a forward-looking forecast (2026–2032) to arm corporate leaders with a practical, decision-ready frame for capital allocation, product strategy, and M&A prioritization.

Spray Dryer Market

Topline: Size, Trajectory, and Competitive Shape

The spray dryer market is at an inflection point. After steady recovery and an acceleration into 2024–2025, global market value stood at USD 6,590 million in 2025. Over the forecast window through 2032, we model a sustained expansion driven by end-market growth and technology-led retrofits, reaching a projected market size in excess of USD 10 billion by the end of the period. This trajectory corresponds to a compound annual growth rate (CAGR) of approximately 6.51% across the forecast horizon — a pace that justifies active investment while demanding careful portfolio prioritization given high capital intensity and long asset lifecycles.

Spray Dryer Market

Market concentration is meaningful: the leading three and five suppliers together account for a substantial share of industry revenue, reflecting high barriers to entry for full-scale systems integration, regulatory-compliant pharmaceutical-grade solutions, and extensive service networks (CR3 ~68.5%; CR5 ~78.2%). For strategic planners, that concentration matters: it shapes partner selection, pricing power, and M&A rationale.

Spray Dryer Market

Why this research matters for 2026 decisions

- CapEx Prioritization: With typical large-scale spray drying installations representing multi‑million-dollar projects, procurement teams must balance immediate capacity needs against multi-year productivity gains achievable via energy-efficiency or modular designs. Our study supplies the decision frameworks that convert market signals into prioritized investment roadmaps.

- Regulatory Readiness: New compliance imperatives — notably the FDA Quality Management System Regulation (QMSR) effective February 2, 2026, and validated expectations for Quality by Design (QbD) in pharmaceutical spray drying — elevate the cost of non-compliance and increase the value of vendors that bundle validation support and documentation services. The report outlines practical steps to map equipment selection to regulatory timelines.

- M&A and Partnership Sourcing: Given the concentrated supplier landscape, inorganic strategies (acquihires, bolt-on capabilities for pilot-to-production scale, service network expansion) are often more effective than greenfield builds. We provide a prioritized short list and rationale for targets based on capability gaps, geographic footprint, and technology synergies.

- Operational Cost Modeling: Energy and labor are persistent cost levers. The market remains energy‑intensive and operationally demanding; our TCO templates quantify the impact of energy-efficiency retrofits, automation, and service contracts on payback timelines.

Key drivers and headwinds shaping 2026 strategies

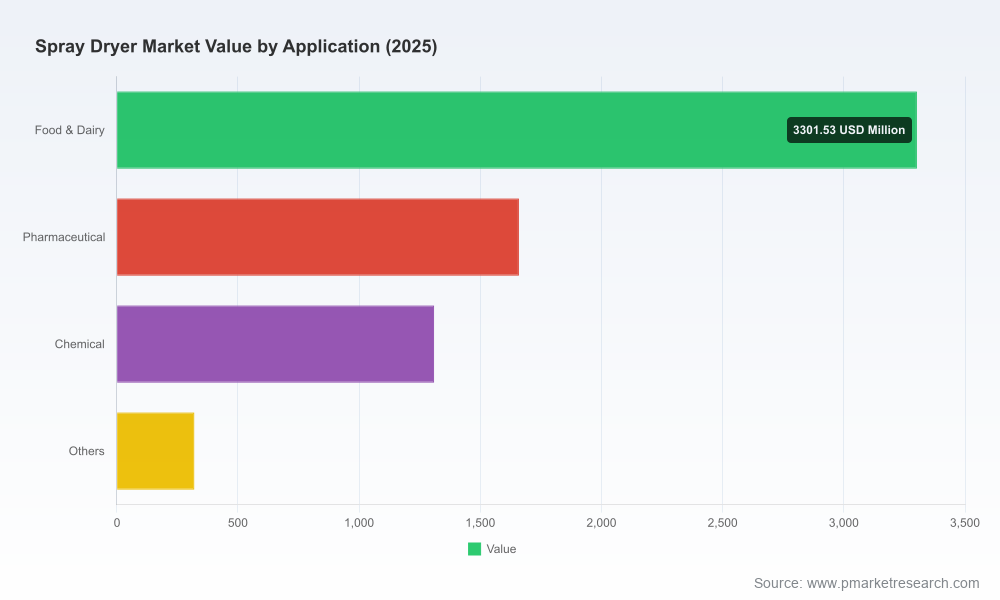

- Demand composition and sectoral pull: Growth is being pulled by sustained expansion in food & dairy, pharmaceuticals, and specialty chemicals — each with distinct technical and compliance requirements. Understanding these differences is central to product positioning.

- Regulatory tightening: The FDA QMSR adoption and reinforced expectations around process validation (QbD) make supplier validation capabilities a differentiator. Buyers seeking rapid time-to-market for regulated products will favor vendors that provide documented design spaces and integrated validation packages.

- Energy and CapEx pressure: Spray drying is inherently energy‑intensive; energy costs and decarbonization targets materially influence equipment selection and operating models. Capital deployment decisions must now incorporate energy price volatility and potential incentives for efficiency upgrades.

- Skills and operations: Skilled operators remain a constraint. Investments in automation, remote monitoring, and training programs materially reduce the risk profile of new installations and support better uptime and quality consistency.

What PW Consulting’s report delivers (practical, actionable contents)

- Robust topline market sizing and scenario projections (base year 2025; forecast 2026–2032), including high/low demand scenarios tied to end-market cyclical risks.

- Detailed supplier landscaping and capability scorecards — performance on regulatory support, service network depth, energy-efficiency options, and pilot-to-production pathways.

- Technology roadmap and competitive differentiation matrix — rotary vs. nozzle, closed-loop and pulse-combustion innovations, modular units, and lab/pilot systems strategies (note: segment-level numeric breakdowns are reserved for the full report to preserve commercial integrity and client value).

- TCO and payback models tailored to common deployment cases (food/dairy, pharma, chemical) that let procurement teams stress-test CapEx vs. Opex trade-offs under different energy-price and duty-cycle assumptions.

- Regulatory impact playbook mapping QMSR and QbD requirements to procurement checklists, validation milestones, and dossier-ready documentation expectations.

- Go-to-market and aftermarket service playbooks for OEMs and large end-users focused on service-as-revenue, digital retrofits, and outcome‑based supply agreements.

- Risk matrix and mitigation plans — supply chain continuity, training and workforce transition, retrofit sequencing, and environmental compliance pathways.

Competitive landscape — strategic moves to watch

The competitive field is heterogeneous: global integrators, regional engineering houses, lab-scale specialists, and niche technology providers each play distinct roles. Below is a strategic lens on several core players whose moves influence market calculus.

- GEA Group AG (Düsseldorf): A global systems integrator with deep expertise in dairy, food‑ingredient, and pharmaceutical plants. Their recent launch of an advanced pharmaceutical spray dryer in August 2025 underscores a deliberate push into compliance-rich, high-value projects. Strategically, GEA’s strength lies in end-to-end offerings and validation support — a high-barrier proposition for buyers prioritizing rapid regulatory approval and scale-up certainty.

- SPX FLOW, Inc. (Charlotte, NC): Known for the Anhydro brand, SPX is positioned around process innovation and advanced atomization. Their appeal to food and pharmaceutical clients centers on proven process controls and aftermarket service — a compelling choice for buyers balancing performance and lifecycle support.

- BÜCHI Labortechnik AG (Flawil, Switzerland): A dominant lab/pilot-scale supplier with a strong foothold in R&D and small-batch clinical manufacturing. Their value is in de-risking process development prior to capital commitment, making them a typical partner in the early stages of product pipelines.

- VetterTec GmbH and other specialized OEMs: These vendors compete on customization capability and vertical expertise (starch, specialty food). They win projects where tailored process design and close engineering partnership matter most.

- Pulse Combustion Systems & energy-focused innovators: Energy-efficiency and alternative drying technologies are an area of active differentiation. Companies that can demonstrate measurable energy and emissions reductions will command a premium in tender evaluations.

- Tetra Pak & large system suppliers: Their integrated solutions for dairy and plant-based powders emphasize automation and integration into broader processing lines. For large processors seeking turnkey solutions, these OEMs present a compelling consolidated risk profile.

- Regional OEMs (e.g., Changzhou Jinqiao, Dedert): Localized cost-competitive options, often coupled with deep regional service footprints. Ideal for customers prioritizing price and proximity, but buyers should assess validation and documentation support for regulated markets.

Recent industry signals — tactical implications

- Product launches and installations: GEA’s August 2025 pharmaceutical dryer launch, and recent lab installations in early 2026, signal two things: suppliers see growth in regulated pharmaceutical volumes, and they are investing to capture share across R&D-to‑manufacturing transitions. Buyers should use supplier roadmaps to benchmark their own scale-up timelines.

- Regulatory change: FDA QMSR’s adoption in February 2026 elevates compliance risk for firms using spray drying in medical device or pharma contexts. Procurement criteria must now include explicit QMS alignment and documented ISO-based practices.

- Energy and labor realities: High operating energy and skilled-labor requirements make automation and remote monitoring business-critical. Firms that accelerate digital retrofits will reduce operating variability and secure margin improvements.

Five priority actions for 2026 leaders

- Map CapEx to regulatory milestones: Time installations and upgrades to align with QMSR and product approval calendars to avoid costly rework or validation delays.

- Adopt TCO-first procurement: Shift selection criteria from upfront price to lifecycle cost and documented energy performance; require suppliers to provide scenario-based paybacks.

- Build a pilot-to-production pathway: Invest in lab/pilot partnerships early (or secure supplier pilot-time) to reduce scale-up risk and accelerate commercialization.

- Negotiate service-linked contracts: Use aftermarket and validation services as leverage in procurement negotiations — warranty extensions, performance SLAs, and training bundles are convertible into lower lifecycle risk.

- Targeted M&A or partnership plays: If scale or capability gaps exist, prioritize targets that plug validation, automation, or energy-efficiency deficits rather than generic revenue plays.

Conclusion — the strategic value of the full PW Consulting study

This preview is intended to crystallize why 2026 is a pivotal year for spray dryer market decisions. With a market expanding from a USD 6.59 billion base in 2025 toward an above‑USD‑10 billion outlook by 2032 at a ~6.51% CAGR, the commercial imperative is clear: act to secure compliant, efficient, and scalable capacity — or cede advantage to more prepared competitors. PW Consulting’s full report translates this macro trajectory into executable plans: validated supplier shortlists, TCO models, regulatory checklists, and M&A playbooks designed for board-level decision cycles.

For senior executives and procurement leaders preparing CapEx submissions or strategic roadmaps in 2026, the report is structured to be immediately operational — a bridge between market intelligence and executable investment decisions. Access to the complete dataset, segment-level modeling, and supplier scorecards is available through PW Consulting’s full Spray Dryer Market report.

For detailed analysis of this topic, please visit the official page:Spray Dryer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com