Ultrafiltration Membrane Filtration Market — Strategic Imperatives for 2026

As water stress intensifies, industrial grade‑water requirements tighten, and treatment operators demand lower lifecycle costs, ultrafiltration (UF) has moved from niche utility to strategic infrastructure. PW Consulting’s latest Ultrafiltration Membrane Filtration Market study (base year 2025) equips executives, investors, and technology leaders with the market intelligence required to convert regulatory pressure and technology change into profitable growth. This introduction outlines the research’s strategic value for decisions you will make in 2026 — showcasing the analytical depth of the full study while intentionally preserving the granular splits and proprietary tables that drive transaction‑level decisions.

Ultrafiltration Membrane Filtration Market

Macro snapshot: scale, trajectory and what it means for 2026 choices

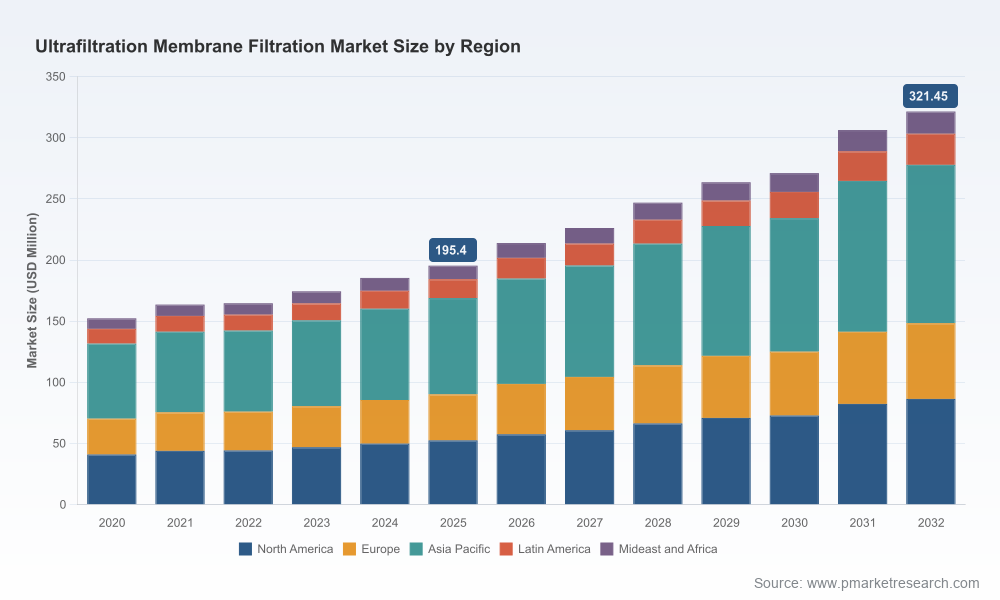

The UF market has demonstrated steady expansion through the first half of the decade and enters 2026 from a position of commercial maturity and accelerating demand. On a base‑year view, the market value in 2025 sits under USD 200 million (reporting units in Million USD). Our model projects a compound annual growth rate of approximately 7.45% across the 2026–2032 forecast window, reflecting a confluence of regulatory tightening, broader desalination pretreatment adoption, and rising process‑water needs in high‑value industries. By 2032 the market reaches a materially larger scale than today, reinforcing that strategic investments made in 2026 will compound through the decade.

Ultrafiltration Membrane Filtration Market

Two implications are immediate for corporate planners: (1) capital allocation decisions in 2026 should tilt to technologies and suppliers that demonstrate demonstrable total cost‑of‑ownership improvements ahead of unit price competition; and (2) go‑to‑market and supply‑chain choices must anticipate stronger demand volatility tied to project cycles in semiconductor, utilities, and large industrial clients.

Ultrafiltration Membrane Filtration Market

Why this research matters now: five drivers reshaping priorities

- Regulatory and quality delta: Stricter discharge standards and tighter reuse guidelines across municipal and industrial jurisdictions are elevating UF from a pretreatment option to a compliance cornerstone.

- Sectoral demand concentration: High‑value verticals — semiconductors, bioprocessing, and certain food/beverage segments — are accelerating adoption of advanced UF solutions that promise higher uptime and tighter particle control.

- Technology step‑changes: Material innovations and module design advances (e.g., lower‑biofouling surfaces, integrated pre‑filtration concepts, and SiC/ceramic options for extreme environments) are changing procurement criteria from simple cost to lifecycle performance.

- Capex optimization pressure: Customers increasingly evaluate UF solutions within integrated process stacks (UF+RO, MBR systems) and for compact footprints on constrained sites — favoring suppliers that can deliver system‑level OPEX/footprint advantages.

- Market fragmentation creates opportunity: Market concentration metrics show a principally fragmented supplier base, which accelerates potential for strategic partnerships, bolt‑on acquisitions, and channel consolidation.

Competitive landscape: capability map and strategic implications

Our vendor coverage blends global leaders, material innovators, and specialist suppliers — each occupying distinct strategic positions that matter for incumbent suppliers and new entrants alike:

- Toray Industries (Tokyo, Japan) — a leader in hollow‑fiber modules, now extending its value proposition with a next‑generation, lower‑biofouling module and an ultra‑fine nominal pore option (announced April 2026). This enhances Toray’s pitch where fouling risk and long runs between cleanings are critical.

- DuPont de Nemours (Wilmington, Delaware, USA) — advancing integrated module concepts with an April 2026 launch that combines pre‑filtration and UF into a single module, explicitly targeting footprint and capital reduction. If performance benchmarks hold, this is a disruptive go‑to‑market lever for desalination pretreatment and municipal projects.

- Veolia Water Technologies & Solutions (Paris, France) — an operator‑integrator with strong systems capabilities in UF/RO and MBR applications, evidenced by recent flagship contracts in high‑value water for semiconductor facilities and long‑term O&M arrangements.

- Cembrane A/S (Aarhus, Denmark) — positioning SiC membranes as the industrial, high‑throughput answer for utilities and heavy industry where chemical and thermal resilience command premiums.

- BASF SE (Ludwigshafen, Germany), Synder Filtration, Meissner Filtration, and regional specialists such as Theway Membranes — together they populate a market where material science, module design, and application specificity (e.g., bioprocess vs. municipal) define differentiation.

Strategic takeaway: with CR3 and CR5 measures indicating a low to moderate share concentration, incumbents should expect continued competition on innovation and service delivery rather than price alone. For buyers, this fragmentation increases negotiating leverage but also heightens evaluation complexity — reinforcing the need for structured vendor scorecards and performance validation protocols.

What the full PW Consulting report delivers (practical, transaction‑ready components)

The study is built to inform 2026 execution. Highlights include:

- Transparent market sizing and forecast model (base 2025), with scenario layers that stress test adoption under regulatory, capex, and supply‑disruption shocks.

- Technology deep dives: membrane materials, module architectures, and lifecycle fouling/cleaning regimes with lab‑scale performance mapping.

- Vendor benchmark scorecards: operational KPIs, product roadmaps, reliability records, and commercial terms synthesized into actionable shortlists for RFPs.

- Commercial playbooks for utilities, industrial users, and system integrators — including TCO calculators, contract structures, and O&M optimization templates.

- M&A and partnership decision frameworks that map capabilities to inorganic growth targets, valuation sensitivities, and integration playbooks.

- Regulatory and standards tracker to align product development and certification roadmaps with near‑term compliance deadlines in major markets.

Note: while this introduction references the types of segmentation analyzed, the full document contains the granular regional, type, and application splits, plus underlying datasets and model granularity — these are intentionally retained for licensed report users.

Strategic playbook for decision‑makers in 2026

Based on our integrated analysis, PW Consulting recommends a three‑track approach for market participants:

- Defend and deepen core offerings: Prioritize materials and module configurations that demonstrably lower lifecycle fouling and cleaning downtime. For suppliers, this means reallocating R&D budgets toward surface chemistry and integrated module concepts that reduce footprint and OPEX.

- Target smarter partnerships not just customers: System integrators and membrane specialists should form productized alliances (joint warranties, shared performance guarantees) to win large, integrated projects — particularly in sectors where water quality is mission critical.

- Use selective M&A to fill capability gaps: Given the fragmented supplier base, bolt‑on acquisitions focused on high‑value materials (SiC, PVDF/PES specialty grades) or regional manufacturing footprints can accelerate scale and reduce delivery lead times.

90/180/360 day execution checklist

- 0–90 days: Run a vendor scorecard for current suppliers with an emphasis on validated fouling metrics, lead times, and retrofit capability; initiate pilot agreements with at least one supplier offering integrated modules.

- 90–180 days: Execute an internal TCO analysis comparing retrofit vs. greenfield choices across priority accounts; prepare an RFP template and shortlist vendors using the PW Consulting benchmark methodology.

- 180–360 days: Finalize supply agreements with performance SLAs, lock in strategic partnership/MOU terms where necessary, and align 2027 capex to capture projected demand spikes while maintaining cash discipline.

Closing — how PW Consulting’s insight accelerates confident action

2026 presents a narrow window where technical differentiation, regulatory alignment, and commercial structuring will compound into multi‑year competitive advantage. PW Consulting’s Ultrafiltration Membrane Filtration Market study converts market momentum and vendor dynamics into specific, executable investments and commercial plays. The full report includes the proprietary segmentation tables, downloadable model files, vendor scorecards, and RFP templates that underpin the recommendations outlined here — content we withhold in this executive preview to preserve the actionable intelligence available to licensed subscribers.

For teams planning 2026 capital allocations, product roadmaps, or M&A outreach, the report functions as both a market map and an operational playbook. Contact PW Consulting or access the full study to unlock the datasets and proprietary analyses required to convert the 7.45% CAGR trajectory and expanding market scale into measurable competitive advantage.

For detailed analysis of this topic, please visit the official page:Ultrafiltration Membrane Filtration Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com