Metallocene Catalyst Market: Strategic Preview for 2026 Decision-Making

Executive Synopsis

As PW Consulting’s lead industry analyst, I present a distilled strategic preview of our full Metallocene Catalyst Market study. The global metallocene catalyst market has demonstrated steady expansion across the 2020–2025 historical window and is projected to continue on a mid-single-digit CAGR over the 2026–2032 forecast horizon. Using a 2025 base year, our topline modeling places total market revenue in the low‑hundreds of USD Million in 2025, progressing to a substantially larger opportunity by 2032 under a 6.85% compound annual growth rate. This preview identifies the value levers that will matter to C-suite and investment committees in 2026 — without disclosing the proprietary segment-level datapoints that are contained in the full report.

Metallocene Catalyst Market

Why This Study Matters for 2026 Decisions

- Timing capital allocation: Technology- and feedstock-sensitive investments in polyolefin capacity require high-resolution views of catalyst-driven margins. Our study translates catalyst dynamics into actionable investment timing signals for both producers and technology licensors.

- Product portfolio prioritization: Metallocene chemistry unlocks performance attributes (clarity, toughness, process window) that can justify higher downstream value capture. We show where to prioritize R&D and commercialization resources to maximize return on incremental capex.

- Supply‑chain risk mitigation: With feedstock pricing volatility and regional regulatory shifts, understanding where metallocene economics decouple from commodity catalysts is essential to contracting, hedging, and sourcing strategies.

- M&A and partnership playbooks: The study offers an evidence-based framework to size bolt-on acquisitions, JV targets, and licensing opportunities against commercial traction scenarios that boards will debate in 2026.

Market Trajectory — The Macro View

From a consolidated vantage, the market has grown from a modest base in 2020 to a materially larger market by 2025, reflecting broader polyolefin demand and accelerating adoption of single-site catalyst technology. Our forecasts extend to 2032 and reflect an assumed compound growth pathway (CAGR 6.85%) that incorporates expected product upgrades, regulatory-driven material substitution, and measured penetration into specialty polyolefin niches. The topline model is stress‑tested across multiple feedstock and regulation scenarios to help executives understand upside, base, and downside cases for the next investment cycle.

Metallocene Catalyst Market

Dynamics Shaping the Market

- Feedstock price movements: Recent market observations show downstream polyethylene grades responding to upstream ethylene variations — for example, Northeast Asia mLLDPE pricing moved to roughly 1.19 USD/kg in March 2026 with a modest downward adjustment, driven by easing upstream costs and catalyst feedstock flows. Our report quantifies how such movements impact catalyst economics across manufacturing routes.

- Regulatory tailwinds and constraints: Policy measures such as the EU’s Packaging and Packaging Waste Regulation (mandating recyclable, mono-material packaging by 2030) create clear demand pull for metallocene-enabled resins that support monomaterial structures and film downgauging. Conversely, stricter waste and chemicals rules alter lifecycle cost calculations for certain catalyst systems — we map these regulatory vectors to commercial outcomes.

- Relative unit economics: Metallocene catalyst systems remain a premium technology relative to conventional heterogeneous catalysts — industry measures indicate metallocene systems can cost approximately 30–40% more than Ziegler‑Natta equivalents in some LLDPE applications. Our scenario analysis demonstrates when the performance delta (yield, quality, processing efficiency) overrides the upfront catalyst premium to produce net margin improvement.

Competitive Landscape — Who Moves the Needle

The market exhibits moderate concentration: the leading three suppliers control a significant portion of the global market (CR3 around the high‑fifties percent), while the top five raise concentration further into the high‑sixties. This structure creates a market with a mix of technology incumbents, diversified chemical majors, and regional specialist suppliers. Key players profiled in the full study include established licensors and catalyst houses as well as vertically integrated resin producers and specialized chemical manufacturers.

Metallocene Catalyst Market

- Technology licensors and process integrators: Global licensors with proven single‑site processes continue to secure world‑scale project selections, illustrating the strategic value of pairing catalyst and process know‑how.

- Catalyst specialists and chemical intermediates suppliers: Firms offering ligand synthesis, custom metallocenes, and activator systems are competing on formulation capability and supply reliability.

- Regional and industrial players: Several vertically integrated petrochemical firms and local manufacturers are leveraging proximity to feedstock and converters to win market share in targeted geographies.

Recent market events — such as a major technology selection for a world‑scale polyethylene line in 2024 and the launch of novel metallocene‑based grades optimized for film applications — validate the continued strategic importance of metallocene chemistries to resin producers and converters. The full report contains a competitive matrix that maps each named player against technology depth, commercial footprint, customer segments, and strategic intent.

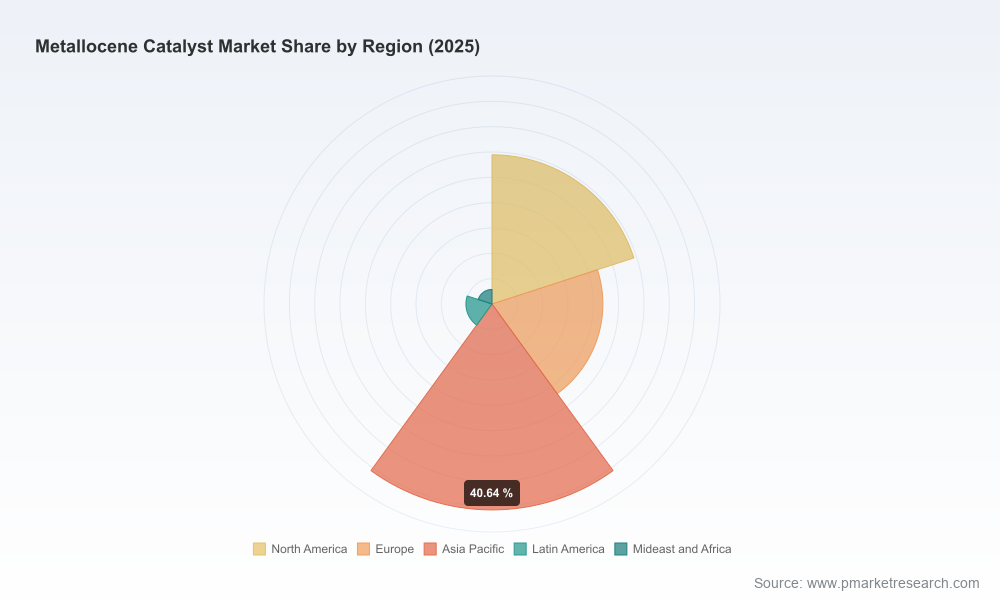

Segmentation & Product Strategy (what we analyze — not disclosed here)

Our segmentation approach layers by catalyst architecture (single‑site variants), application end‑markets (film, injection, extrusion, specialty polyolefins), and regional demand drivers. Rather than publish proprietary split values in this preview, we highlight the analytical outputs executives need:

- Elasticity profiles that show how different downstream products respond to catalyst price and performance changes.

- Adoption curves for innovative catalyst formulations across incremental film and molded applications.

- Value capture ladders that quantify margin uplift from product upgrades and process efficiency gains.

These deliverables enable portfolio prioritization without exposing the granular segment tables reserved for the full study.

Practical, Actionable Contents of the Full Report

- Methodology appendix: transparent modeling assumptions, base‑case build‑up, and sensitivity levers for feedstock, catalyst pricing, and regulatory scenarios.

- Detailed demand forecast to 2032 with scenario bands and policy overlays for recycling and single‑material mandates.

- Supply‑chain map and supplier risk matrix highlighting concentration points, raw‑material dependencies, and alternative sourcing strategies.

- Competitive benchmarking: capabilities matrix, technology readiness levels, and inferred strategic intent for the dozen core vendors profiled.

- Price and margin modeling: per‑tonne economics mapped to catalyst choice, process technology, and film/grade outcomes.

- M&A & partnership heatmap: prioritized acquisition targets and licensing opportunities by value‑creation potential.

- Implementation playbooks: go‑to‑market and procurement strategies tailored to producers, converters, and catalyst suppliers.

Strategic Imperatives for 2026

- Operate with optionality: structure capex and licensing deals to allow downgrades or upgrades in catalyst choice as feedstock and regulatory signals crystallize.

- Lock performance, not just price: negotiate contracts that align catalyst cost to realized polymer performance (e.g., downgauging, throughput gains), reducing the risk of paying a premium without capture.

- Invest in downstream partnerships: converters facing recycling and mono‑material mandates will reward resin suppliers that co‑engineer formulations built on metallocene platforms.

- Targeted in‑licensing: for companies without in‑house metallocene expertise, prioritized licensing or JV structures can accelerate market entry with controlled downside.

- Hedge raw material and catalyst feedstocks: implement hedges and supply agreements that reflect the non‑linear relationship between ethylene pricing and metallocene economics.

What We Withhold Here (and why)

This preview adheres to a “trailer” principle: enough technical depth to build confidence in our methods and recommendations, but not the proprietary segment tables, price decks, or region/application split values that clients use to make transactional decisions. The full dataset — including granular regional and application breakdowns, supplier share tables, and project‑level financials — is available through the report portal and is essential for executing M&A, procurement negotiations, or detailed capex case work.

How PW Consulting Can Engage

We offer three pragmatic engagement paths to convert the intelligence into action over the 2026 decision cycle:

- Rapid Decision Pack (2 weeks): tailored briefings and a focused economic model to support an imminent investment or procurement decision.

- Deal‑Support Sprints (4–8 weeks): due diligence, vendor screening, and term‑sheet development for M&A or JV agreements.

- Strategic Partnership Program (3–6 months): co‑developed go‑to‑market playbooks, licensing strategies, and pilot deployments with KPI‑linked outcomes.

Closing — The Strategic Tradeoffs

Metallocene catalysts present a classic strategic tradeoff in 2026: higher upfront catalyst and formulation costs versus differentiated resin performance and regulatory alignment that can command price premia or unlock new markets. Through transparent modeling, scenario stress tests, and competitive mapping, our full study arms executives with the evidence required to choose where to compete and how quickly to commit capital. For teams prioritizing precision in 2026 — whether on capital allocation, procurement, or product strategy — the full PW Consulting report is the operational instrument to convert market intelligence into measurable value.

To access the complete dataset, company profiles, and executable playbooks referenced in this preview, please visit the report page or contact our sales team for a confidential briefing.

For detailed analysis of this topic, please visit the official page:Metallocene Catalyst Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com