Micro‑Lens Arrays Market: Strategic Imperatives for 2026 Decision‑Makers

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present a high‑level orientation to our new Micro‑Lens Arrays (MLA) market study — a briefing designed to clarify the market dynamics that will shape procurement, R&D, and corporate strategy in 2026. The industry is at a practical inflection point: after recovering from pandemic-era disruption, the global MLA market expanded from roughly USD 160 million in 2020 to about USD 215 million by 2025, and is projected to continue growing at a mid‑single‑digit compound annual growth rate (CAGR ~6.5% through 2032), reaching well into the mid‑hundreds of millions by the end of the forecast period. What follows is a synthesis of the actionable insights we distilled — offering strategic direction while preserving the granular segment-level findings for subscribers to the full report.

Micro-Lens Arrays Market

Why Micro‑Lens Arrays Matter in 2026

- Systems integration and miniaturization: OEMs across telecom, automotive, consumer optics, and medical devices are embedding sophisticated micro‑optics to meet tighter form‑factor, efficiency and performance requirements.

- New optical system architectures: Photonic integrated circuits (PICs), LiDAR modules, microLED displays, advanced fiber coupling and AR/VR optics are driving demand for MLAs with tighter tolerances, varied materials and bespoke freeform geometries.

- Performance vs cost tradeoffs: As system volumes rise, customers are balancing high‑performance glass and fused‑silica solutions with lower‑cost polymer alternatives; manufacturability and repeatability have become procurement drivers.

- Regulatory and supply resilience: Tariff changes and raw material concentration are shifting sourcing strategies from global optimization to resilience‑focused configurations.

Market Trajectory: Growth with Pockets of Volatility

The headline growth numbers conceal an important nuance: while the market has re‑accelerated since 2022, growth is uneven across end‑use applications and technology routes. The market expanded meaningfully between 2020 and 2025, reflecting stronger demand in telecommunications, sensing and consumer optics. Our 2026–2032 forecast (CAGR ≈ 6.49%) models continued adoption but assumes periodic episodic shocks — from material shortages to tariff oscillations — that create windowed premium pricing and extended lead times for high‑precision glass MLAs.

Micro-Lens Arrays Market

Competitive concentration remains relatively low: top players account for well under a third of total market sales, which implies a fragmented supplier base and opportunities for consolidation or vertical integration by strategic players. That structural fragmentation, coupled with rising application complexity, creates clear entry points for specialized suppliers and service providers.

Micro-Lens Arrays Market

Supply‑Side Realities and Risk Signals

- Raw material constraints: Specialty optical glasses containing rare‑earth dopants and high‑grade fused silica are subject to supply concentration and periodic shortages. Companies dependent on these feedstocks face the dual pressure of cost inflation and extended lead times during demand surges.

- Trade and tariff dynamics: Recent measures (notably new duties imposed in 2025) materially changed the cost calculus for imported substrates and finished MLAs. The immediate reaction has been increased capitalization on localized production and diversification of supply sources.

- Labor and process complexity: High‑precision polishing, alignment and microfabrication require skilled labor and process controls that raise unit costs as volumes scale. Automation reduces per‑unit labor exposure but requires upfront capex and design for manufacturability investments.

- Geopolitical concentration: High‑precision glass MLA capacity is concentrated in a small set of advanced manufacturing hubs. This concentration elevates vulnerability to geopolitical friction, natural disasters and export controls.

Technology & Manufacturing Landscape: Choosing the Right Route

MLA production today spans a spectrum of approaches — each with distinct scaling, cost, and performance tradeoffs. Leading processes include high‑precision glass microfabrication and molding, wafer‑level imprint lithography, silicon‑based etch techniques, and additive manufacturing via two‑photon polymerization (2PP) for freeform optics. Material choices — fused silica, high‑index glass, PMMA and silicon — interface with process choices to determine optical performance, environmental robustness and price per unit.

Decision criteria we use with clients include: optical tolerance requirements; thermal and environmental exposure; volume and ramp profile; supplier geographic footprint; IP and patent exposure; and lifecycle cost (including repair and replacement cycles). In practice, a hybrid approach — combining high‑performance glass MLAs for mission‑critical nodes with polymer or wafer‑level solutions for high‑volume, lower‑spec subassemblies — is emerging as a dominant commercial pattern.

Competitive Landscape: Strategic Positions & Partnership Vectors

Our competitive analysis highlights a diverse set of players, each occupying specific niches across materials, technology and go‑to‑market models:

- AGC Inc. (Tokyo): Strength in high‑precision glass microfabrication and molding positions AGC to serve high‑reliability optical systems (e.g., camera modules, automotive lighting) where material integrity is paramount.

- Holographix LLC (Marlborough): Focused on custom, cost‑effective MLAs and recent expansion of design services (launch in early 2025) makes this firm attractive as a collaborative partner for rapid prototyping and design‑led solutions.

- Axetris AG (Kernen): Offers silicon and fused‑silica wafer MLAs with high pitch accuracy — a fit for telecom/datacom and coupling applications requiring wafer‑scale consistency.

- Nanoscribe GmbH (Jena): As a leader in 2PP additive microfabrication, Nanoscribe enables complex freeform and hybrid optics that are difficult or impossible with subtractive methods — a critical capability for next‑generation sensors and bespoke devices.

- SUSS MicroOptics SA (Hauterive): Wafer‑level imprint expertise and automotive quality certifications make SUSS a go‑to supplier for high‑volume, automotive‑grade lighting and PIC coupling applications.

- PowerPhotonic, Avantier, Thorlabs, Edmund Optics and others: These suppliers span fused‑silica specialty solutions, precision polishing for machine vision, and catalog PMMA MLAs for research and instrumentation — collectively providing a healthy supply ecosystem for OEMs of various scale.

Strategic implications: OEMs should map supplier capabilities to their product roadmaps (not every supplier is suited to high‑volume automotive vs. bespoke sensor modules). Investors and acquirers should prioritize firms with scalable manufacturing platforms, proprietary process control, and customer design service capabilities. For suppliers, investing in design partnerships, certification (e.g., automotive standards), and local presence in critical demand regions will be differentiators in 2026.

Actionable 2026 Playbook for Decision‑Makers

- Supply‑chain resilience: Implement dual‑sourcing strategies for critical materials, qualify regional alternate suppliers, and build staged inventory for critical long‑lead items to smooth production ramps.

- Technology selection framework: Use a standardized evaluation matrix that weighs optical performance, throughput, unit cost, TRL (technology readiness), and supplier risk to select solutions for each application tier.

- Partner early on design: Engage MLA suppliers in the concept phase to optimize for manufacturability and cost — design‑for‑optics pays back in yield and time‑to‑market.

- Investment and M&A posture: Target acquisitions that bring wafer‑level or freeform fabrication capabilities, or that consolidate fragmented supply in strategic regions. Consider contract manufacturing partnerships to de‑risk capex.

- Regulatory and sourcing intelligence: Monitor tariff developments and raw‑material market dynamics; scenario‑model pricing and sourcing outcomes to inform multi‑year procurement contracts.

- Operationalize quality: For safety‑critical applications (automotive, medical), prioritize suppliers with certified processes and traceability; factor qualification timelines into product roadmaps.

What PW Consulting’s MLA Report Delivers (Practical Components)

The full study is built to convert insight into executable plans. Key deliverables include:

- Market sizing and validated growth scenarios (historical and forward forecasts);

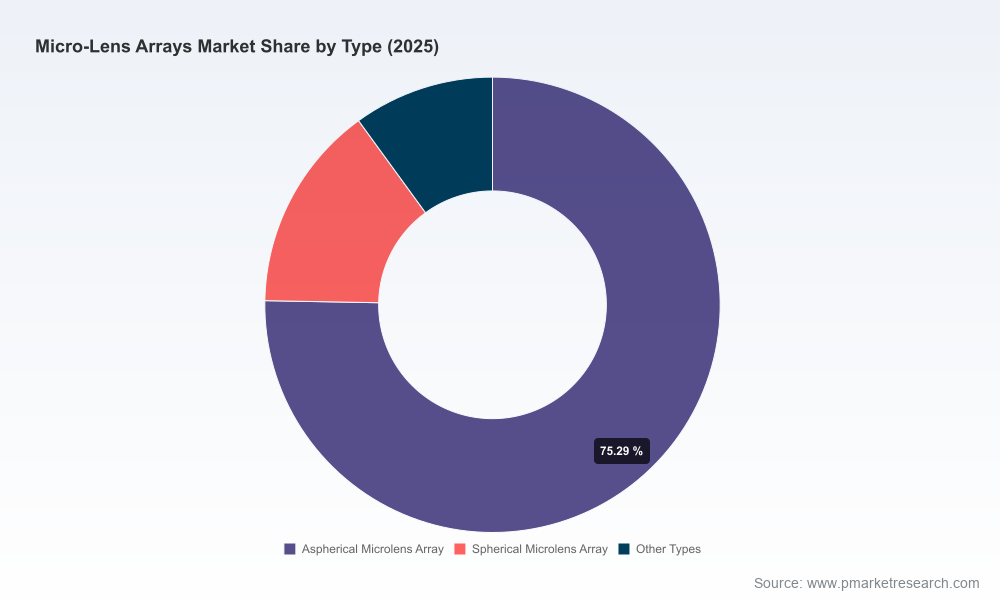

- End‑use and technology segmentation with adoption curve modelling (detailed segment data reserved for the full report);

- Supply‑chain maps and vulnerability heatmaps that quantify exposure to material, geographic and regulatory risks;

- Manufacturing cost models comparing glass, silicon, polymer and additive approaches under multiple volume and yield assumptions;

- Supplier capability matrices and a scored vendor short‑list for different application classes;

- Use‑case ROI calculators for MLA integration in telecom, sensing, display and medical platforms;

- M&A and partnership playbooks including an acquisition‑target heatmap and integration checklists;

- Policy and tariff scenario analysis with recommended mitigation steps for procurement and product teams.

Next Steps for Leaders

For executives preparing budgets, vendor strategies or M&A pipelines in 2026, the imperative is clear: treat MLA sourcing and technology choices as strategic levers, not commodity procurement. Decisions made now about material choices, supplier partnerships, and capacity commitments will materially affect product performance, cost curves and time‑to‑market through the end of the decade.

PW Consulting’s full Micro‑Lens Arrays Market report contains the granular segmentation, regional and application breakdowns, vendor‑level benchmarking and scenario data necessary to convert these strategic imperatives into operational plans. Contact PW Consulting’s industry practice or visit our report portal to access the full dataset, vendor scorecards and bespoke advisory services that turn the market’s complexity into a competitive advantage.

For detailed analysis of this topic, please visit the official page:Micro-Lens Arrays Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com