Electrochromic Window Market Analysis: Supply Chain, Pricing, and Forecast 2025 –2032

Home |

2026-06-03 08:46:25

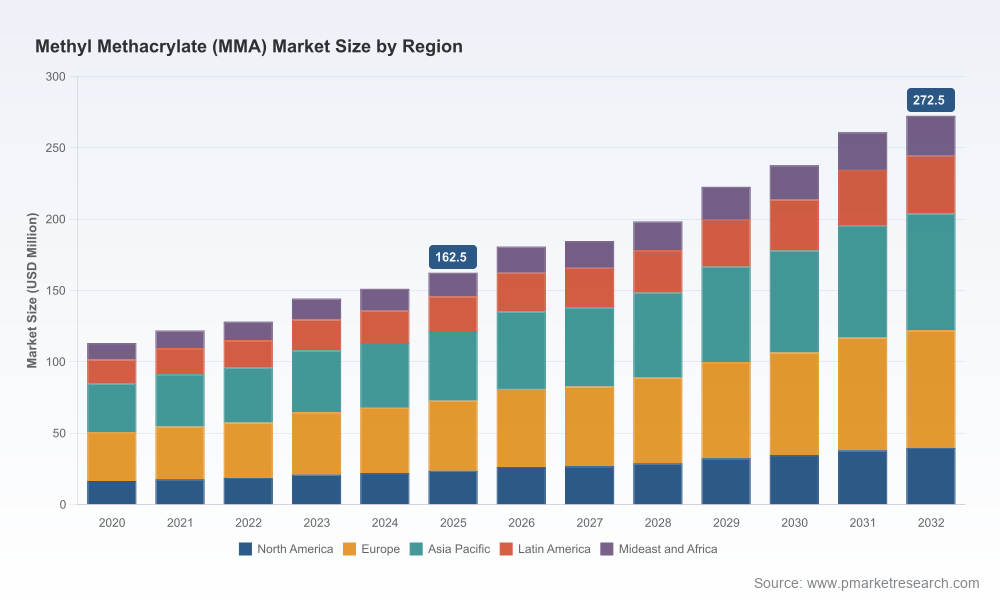

As PW Consulting releases its full Methyl Methacrylate (MMA) Market study, this preview outlines the strategic value of the analysis for executives planning capital allocation, sourcing, and product development in 2026. The MMA market is at a structural inflection point: after recovering steadily through 2020–2025 to reach a robust base year, our forecast period (2026–2032) projects continued expansion at a compound annual growth rate (CAGR) of 7.9%, with the market trajectory reflecting both demand-side resilience and supply-side realignment. This combination produces near-term volatility and medium-term opportunity for incumbents, challengers, and buyers alike.

Methyl Methacrylate (MMA) Market

Timing of investment decisions. With the market expanding at an aggregated CAGR of 7.9% over the forecast horizon, 2026 is the year to decide whether to fast‑track capacity, secure long‑lead feedstock arrangements, or pivot toward higher‑margin downstream applications. Small shifts in timing will materially affect utilization, cash flow and competitive position across the cycle.

Methyl Methacrylate (MMA) Market

Supply chain repositioning. Recent industrial moves and technology shifts have changed regional supply balances and the economics of feedstock choices. Executives must evaluate whether to rely on legacy suppliers, underwrite new technologies, or pursue backward integration for feedstock resilience.

Methyl Methacrylate (MMA) Market

Sustainability as value creation. Low‑carbon production routes and chemical recycling are no longer solely reputational imperatives; they are becoming sources of differentiation and cost advantage in procurement processes and large OEM specifications.

Our study calibrates the MMA market to a 2025 base year, quantifying historic flows and validating a forward outlook through 2032. The top‑line market value has expanded meaningfully over the 2020–2025 period, and under the scenarios modelled in the report the market reaches materially higher levels by 2032 consistent with the 7.9% CAGR noted above. We also quantify market concentration dynamics — the top three and top five producers control a substantial share of global capacity — providing an evidence base for competitive positioning and bargaining power analysis. These macro numbers underpin the scenario economics and sensitivity analyses that inform the recommendations below.

Executive dashboard — one‑page investor and procurement briefs that translate market drivers into decision options for 12–36 month horizons.

Top‑line and scenario forecasts — base, upside and downside cases with sensitivity to feedstock price, capacity additions/closures, and end‑market demand shocks.

Supply‑side map — plant‑level and technology overlays highlighting recent ramps, closures, and the diffusion of low‑carbon production routes.

Pricing and cost curve analysis — drivers of short‑ and long‑run price movements, break‑even curves for new capacity, and margin compression risk.

Competitive scorecards and M&A watchlist — forensic profiles of key producers, capability maps, and acquisition target assessment frameworks.

Go‑to‑market playbooks for downstream moves — prioritized initiatives for capturing value in coatings, adhesives, PMMA and specialty applications.

Procurement playbook — contract structures, hedging approaches, and supplier segmentation for 2026 negotiations.

Note: to preserve strategic signalling in this preview, we describe the types of segment analyses included in the full study without reproducing the core, proprietary subsegment tables. Access to the full dataset and model is available via the report landing page.

Röhm GmbH — strategic mover: Röhm has completed an industrial‑scale ramp of a C2‑based LiMA MMA plant in the U.S., strengthening supply resilience in North America and introducing a lower‑carbon production route. Recent commercial actions (including targeted price adjustments in parts of Asia) signal active commercial management as the company leverages new capacity.

Mitsubishi Chemical Corporation — scale with selectivity: historically the largest capacity holder, Mitsubishi has been selective about new greenfield investments and walked back a proposed large project in the U.S., reflecting heightened capital discipline and sensitivity to local regulatory and feedstock frameworks.

BASF, Dow, Arkema, Evonik, Sumitomo, Asahi Kasei, Chi Mei, Huntsman — differentiated positions: these incumbents collectively span integrated monomer‑to‑derivative value chains, regional strengths, and specialized downstream portfolios. Their strategic choices — from sustainability investments to portfolio optimization — will determine whether they compete on cost, service, or differentiated product features.

The report quantifies market concentration and competitive dynamics: the top three producers account for a meaningful majority of capacity, and the top five command an even larger share. This concentration creates both risk (single‑source exposure) and opportunity (attractive targets for bolt‑on acquisitions and strategic partnerships).

Capacity reconfiguration. A sequence of plant closures, re‑ramps and strategic optimizations has altered regional availability. Some legacy facilities were shuttered as new, more efficient plants came online; others were repositioned under portfolio programs — a dynamic that has tightened supply in certain windows during 2025–2026.

Feedstock and price pressures. Raw material and energy cost movements pushed MMA prices upward in early 2026. Where feedstock supply is constrained or logistics are strained, short‑term price spikes are possible; conversely, near‑term commissioning of new units can moderate those effects over a 12–24 month horizon.

Technology and sustainability inflection. Adoption of C2‑based LiMA routes and integration of chemical recycling are changing unit economics and the carbon intensity profile of production — factors increasingly valued by large end‑users and subject to regulatory scrutiny.

Re‑map your supply exposure by plant and technology: develop a forward cash‑flow view of incumbent suppliers that incorporates announced closures, ramps, and price intents through 2027.

Prioritize procurement contracts for flexibility: negotiate volume options, indexation clauses and short‑cycle renegotiation triggers to manage the current price‑and‑supply volatility.

Pursue selective vertical integration or JV arrangements where feedstock security is mission‑critical; model at least two time‑to‑value scenarios (rapid build vs. long‑term offtake).

Accelerate product differentiation downstream: invest in PMMA and high‑value methacrylate derivatives that can capture margin regardless of monomer price cycles.

Embed low‑carbon credentials into product strategy: customers are increasingly demanding lifecycle transparency — early movers on low‑carbon MMA will command price premiums in regulated procurement environments.

Scan for opportunistic M&A and bolt‑on acquisitions driven by portfolio optimization programs at incumbents — consolidation activity can create prime targets priced for strategic rather than financial buyers.

Run scenario exercises that combine demand shocks (e.g., slowed auto production) with supply disruptions to stress‑test unit economics and contract terms.

Beyond the market study, PW Consulting offers tailored services to translate insight into action: supplier due diligence, transaction support for acquisitions or JVs, procurement transformation programs, and carbon‑accounting integration for product portfolios. Our models can be adapted to client‑specific trading books, plant footprints, and contractual hedging frameworks.

The macro evidence points to a durable expansion of the MMA market through the decade, but the path is punctuated by supply reconfiguration, technology substitution and episodic price volatility. For corporate leaders, 2026 is not a year for passive observation — it is a window to lock in supply resilience, capture downstream value, and reframe sustainability investments as competitive levers. PW Consulting’s full MMA Market report supplies the analytics, scenarios, and playbooks necessary to convert that window into lasting advantage.

For access to the complete dataset, plant‑level maps, and executable playbooks referenced in this preview, please consult the full report landing page — the detailed subsegment tables and proprietary models are available there for decision teams and investors.

For detailed analysis of this topic, please visit the official page:Methyl Methacrylate (MMA) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com