Uninterruptible Power System (UPS) Market: Strategic Preview for 2026 Decisions

This executive preview sets the strategic frame for PW Consulting’s full market study on the Uninterruptible Power System (UPS) market. It distills the research’ most consequential insights for corporate strategy, capital allocation, product roadmaps, and competitive positioning through 2026 — while intentionally withholding proprietary segment-level detail reserved for the full report. Think of this as the trailer: enough depth to change how you think, not enough to replace the playbook you’ll need to act.

Uninterruptible Power System (UPS) Market

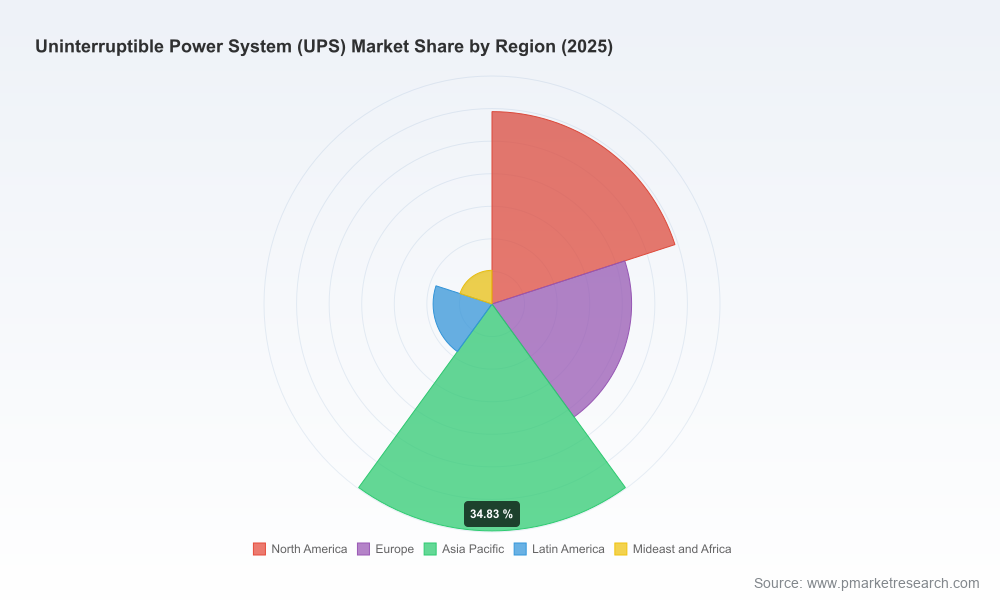

Market snapshot: scale, trajectory and concentration

The UPS market has moved from an estimated USD 130.45 Million in 2020 to USD 180.25 Million in the 2025 base year, reflecting structural demand across data centres, telecommunications, industrial and distributed IT ecosystems. Our consolidated forecast section models a steady compound annual growth rate (CAGR) of 5.85% for the 2026–2032 period, producing a market value approaching USD 266.0 Million by 2032 under the base-case scenario.

Uninterruptible Power System (UPS) Market

Competitive concentration is material but not prohibitive: the top three vendors account for a meaningful slice of market revenue, and the top five push total share beyond the mid‑50s percentile. That profile creates a landscape where scale matters for R&D and supply chain leverage, yet regional specialists and focused innovators can command niches and price premiums.

Uninterruptible Power System (UPS) Market

Why 2026 is a strategic inflection point

- Electrification and data gravity: The accelerating deployment of AI-optimized compute clusters is reshaping power requirements. New medium‑voltage architectures reduce conversion layers and change site-level balance sheets — creating winners among vendors able to deliver high-voltage, high-efficiency protection systems.

- Distributed intelligence and edge proliferation: Edge IT rooms and micro data centres are re‑wiring demand away from one-size-fits-all offerings toward modular, serviceable, and battery-optimized UPS systems.

- Safety and certification as market multipliers: Recent UL and IEC certifications for energy storage and medium‑voltage direct‑connect products are now differentiators. Regulatory endorsements shorten procurement cycles for certified solutions and raise the bar for incumbents without certified portfolios.

- Supply chain and materials pressure: Battery chemistry choices and components sourcing are increasingly strategic issues. Manufacturers moving earlier to validated lithium‑ion configurations demonstrate faster time-to-deploy at the edge and achieve lifecycle cost advantages.

What the full PW Consulting report delivers (practical outputs)

- Market sizing and forecast model (2020–2032) with deployable scenario toggles — base, upside, and downside assumptions tied to volume, price, and technology substitution. (Note: the preview omits segment share tables that are included in the full dataset.)

- Go‑to‑market playbooks for OEMs, channel partners, and system integrators — including pricing levers, service packaging, and contracting models aligned to buyer personas.

- Vendor scorecards and benchmarked financials — R&D intensity, gross margins, installed-base economics, and maintenance revenue streams (proprietary rankings are available only in the full report).

- Technology roadmaps — evaluating medium‑voltage UPS, compact three‑phase designs, and battery chemistries (lead acid vs. lithium‑ion variants), with transition timing guidance for each adoption cohort.

- Supply‑chain risk matrix and mitigation playbook — critical components, dual‑sourcing strategies, long‑lead inventory tactics, and nearshoring implications.

- Investment and M&A heat map — target archetypes, valuation priors, and integration risks for strategic acquirers, private equity, and industrial buyers.

- Policy and regulation tracker — certification timelines, safety standards impacts, and regional compliance implications for project rollout.

Competitive dynamics: what to watch among incumbent and emerging players

The competitive picture is a mix of global industrial conglomerates, specialized UPS manufacturers, and fast-moving Asian system houses. Key players profiled in our research include technical and go‑to‑market snapshots that illustrate the path each is taking to win in 2026 and beyond.

- Schneider Electric (Rueil‑Malmaison, France) — A strategy focused on densification and high‑density IT/industrial solutions. Recent introductions of compact three‑phase UPS systems reflect a product roadmapped to serve constrained footprints and high‑power-density racks. Expect continued emphasis on software and lifetime services to lock in installed‑base revenue.

- Eaton (Dublin, Ireland) — Leveraging strong power‑electronics heritage and industrial channel reach. Eaton’s competitive play emphasizes reliability, broad portfolio coverage and integrated power management software. Success will hinge on execution in medium‑voltage integration and lifecycle service offerings.

- Vertiv (Columbus, Ohio, United States) — Rapidly expanding both ends of the market with compact units for homes/workspaces and heavy industrial/commercial solutions. Multiple 2026 product launches underscore a two‑pronged strategy: capture distributed power needs at small scale while defending data centre and industrial accounts with higher‑capacity systems and services.

- ABB (Zurich, Switzerland) — Pushing the frontier in medium‑voltage UPS with products enabling direct grid connection at higher voltages. The HiPerGuard line, and associated UL 9540 certification for energy storage safety, materially alters deployment economics for large AI data centres and microgrid applications.

- Delta Electronics (New Taipei City, Taiwan) — Strong in modular systems and power electronics manufacturing. Delta’s proximity to Asian hyperscalers and edge deployments supports aggressive pricing and rapid iteration cycles; look for moves into battery‑integrated subsystems.

- Riello UPS (Legnago, Italy) — A specialist with a focus on tailored solutions and aftersales service. Riello’s competitive strength lies in localized engineering and vertical account management.

- Huawei (Shenzhen, China) — Applying systems integration skills and scale to offer complete power ecosystems, often bundling power protection with broader IT and network infrastructure propositions. Their speed of deployment and vertical customer relationships are differentiators, subject to regional regulatory dynamics.

- Toshiba (Tokyo, Japan) — A technology‑led competitor with deep electronics and industrial credentials; positioning emphasizes reliability and long lifecycle performance.

- Piller (Vienna, Austria) — Niche player focusing on very high‑availability solutions for specialised industrial and mission‑critical use cases.

- Shenzhen innovators (Kehua Data, INVT, etc.) — Chinese OEMs providing competitive pricing, modular offerings and aggressive route‑to‑market strategies in Asia and emerging markets. Expect them to contest price‑sensitive segments and increasingly move upmarket on service and certification.

- North American specialists (Falcon Electric, Active Power) — Focused on custom, high‑reliability systems for specific industrial and infrastructure customers; their value resides in engineering depth and bespoke service models.

Recent product and regulatory developments shaping 2026

- Vertiv’s 2026 launches span compact residential/office units and heavy industrial UPS lines, signalling deliberate segmentation of product portfolios to address both distributed digitalisation and traditional heavy industry.

- ABB’s HiPerGuard 34.5 kV family and its UL 9540 certification accelerate medium‑voltage direct‑grid strategies for large AI data centres and microgrids, reducing conversion losses and simplifying site infrastructure.

- Schneider Electric’s compact three‑phase release targets high‑density IT and industrial deployments where footprint and thermal constraints are the gatekeepers for adoption.

- Battery makers have been actively expanding lithium‑ion UPS configurations optimized for edge and distributed IT, shifting total cost of ownership calculations for many operators.

Actionable strategic plays for 2026 decision‑makers

- Scenario‑based portfolio planning — Use the base‑case CAGR of 5.85% as the planning anchor, but stress test plans against a faster medium‑voltage adoption curve and a slower, commodity‑price driven downside. Prioritize modular product designs that allow firms to migrate customers between architectures.

- Certify early or partner with certified vendors — Certifications like UL 9540 are now procurement accelerants. Vendors without certified, grid‑direct architectures face longer sales cycles in hyperscale and AI use cases.

- Capitalize on services — Service and maintenance revenues will increasingly differentiate margin profiles. Design service contracts tied to uptime SLAs that reflect the economics of modern compute loads.

- Hedge supply risk in batteries — Where possible secure multi‑chemistry options, develop long‑term supply agreements, and pilot battery swapping or leasing models to mitigate raw material volatility.

- Targeted M&A and partnerships — For incumbents seeking regional reach or capability infill, pursue tuck‑ins that deliver certification, software telemetry, or battery integration expertise rather than just raw manufacturing capacity.

- Channel reconfiguration — Align channel incentives toward lifecycle contracts and bundled solutions rather than one‑time hardware sales; this amplifies recurring revenue and customer stickiness.

How to use this preview — and next steps

This preview distills the directional insights that PW Consulting believes will matter most to executives making capital, product and M&A decisions in 2026. The full report contains the granular modelling, segmental breakdowns, vendor scorecards, and downloadable scenario tools that translate these insights into executable plans. If you are positioning product roadmaps, prioritising sales territories, evaluating acquisition targets, or re‑designing service economics, the full dataset and playbooks are built to be operationalized within 90 days.

Requesting the complete report will provide access to: interactive forecast models, vendor financial benchmarks, procurement decision matrices, and bespoke advisory sessions tailored to your firm’s role in the UPS value chain. Consider this preview your strategic cue to re-evaluate assumptions — the signal is clear: power protection is now a core business lever, not just an engineering requirement.

Closing note

As the UPS market transitions from commodity replacement cycles to an era defined by direct‑grid, battery‑integrated, and software‑driven power architectures, 2026 will reward firms that pair product engineering with commercial agility. PW Consulting’s full study provides the data and the decision frameworks to convert that reward into measurable outcomes. For those willing to act, the opportunity is both immediate and asymmetric.

For detailed analysis of this topic, please visit the official page:Uninterruptible Power System (UPS) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com